A net balance of +35% of RICS surveyors in the North West reported rising sales expectations at the start of 2026 — while their London counterparts recorded deeply negative sentiment. That single data point captures the most dramatic regional divergence in UK residential property since the post-pandemic rebalancing began. For building surveyors, valuers, and property professionals, understanding these Regional Housing Recovery Trends: Valuation Adjustments for North West Surge vs London Slump in RICS Q1 2026 Surveys is no longer optional — it is a core competency that directly shapes valuation accuracy, client advice, and professional risk management.

Key Takeaways 📌

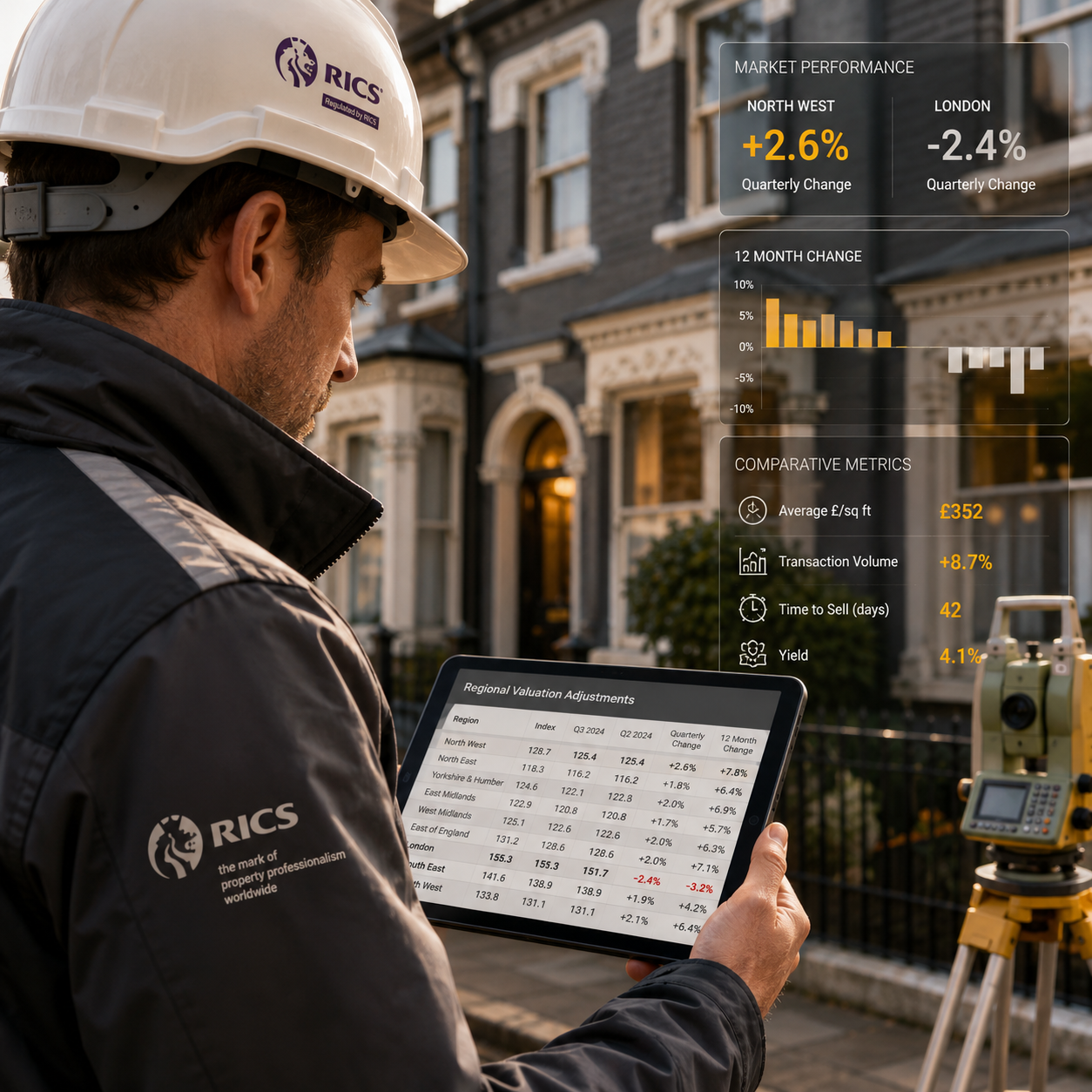

- The North West is the UK's standout growth region in Q1 2026, with annual house price growth of 2.6% and strongly positive RICS sales expectations.

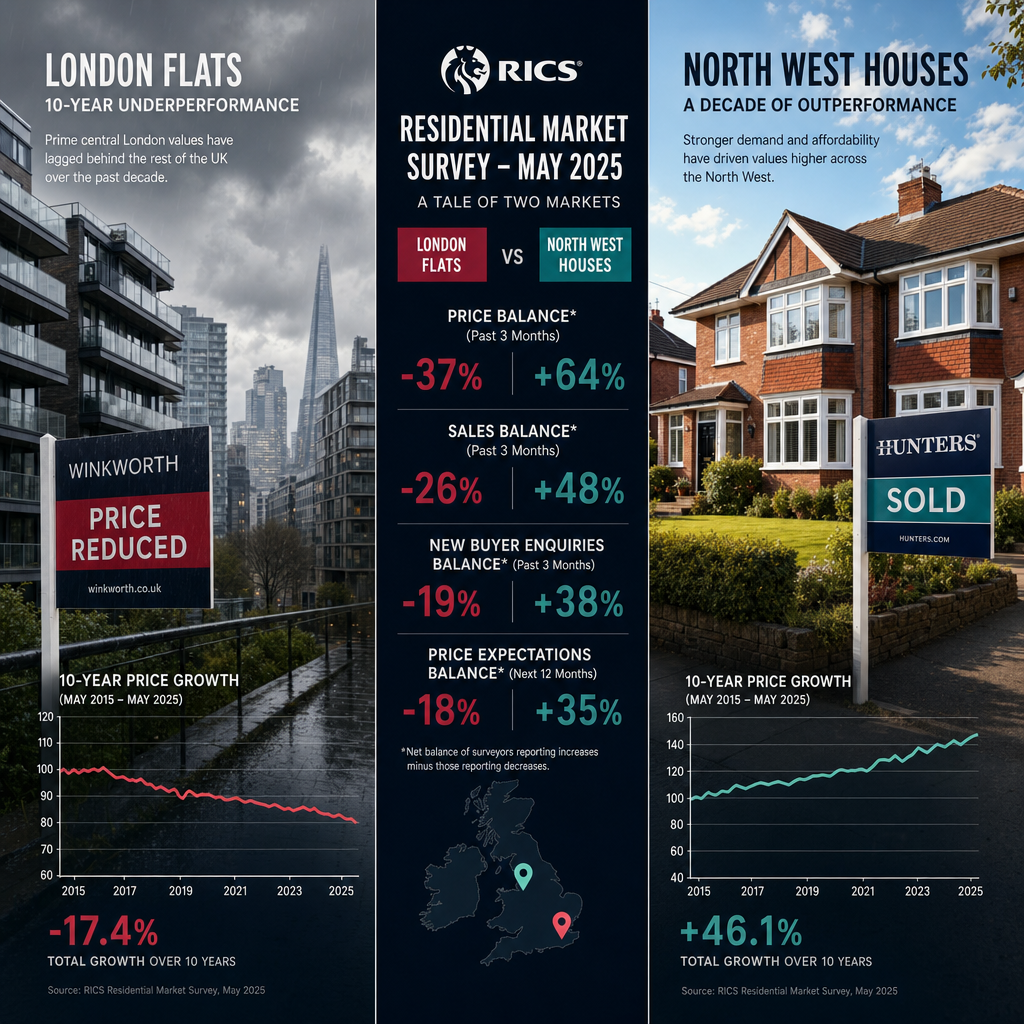

- London is underperforming significantly, recording a 2.4% annual price decline and a decade of only 10% cumulative growth versus 41% nationally.

- Rising mortgage rates (averaging 5.75% on two-year fixes by May 2026) are suppressing national buyer demand, with RICS reporting a -34% net balance on new enquiries.

- Valuation professionals must apply region-specific adjustments, particularly when instructed on properties in diverging markets where comparable evidence is rapidly shifting.

- 46.7% of homes listed in April 2026 were withdrawn unsold, largely due to overvaluation — making accurate, evidence-based appraisals more critical than ever.

Understanding the RICS Q1 2026 Landscape: A Market Divided

The RICS Residential Market Survey for early 2026 paints a picture of a UK housing market that is not one story but many. Nationally, the headline figures tell of caution: new buyer enquiries registered a net balance of -34% in April 2026, and agreed sales sat at a similarly subdued -36% [2]. These numbers suggest a market treading water. Yet beneath that national surface, regional dynamics are pulling in sharply opposite directions.

National Headwinds: Mortgage Rates and Buyer Caution

The primary brake on activity is the cost of borrowing. The average two-year fixed mortgage rate climbed to 5.75% by mid-May 2026, up from 4.83% in March — a jump driven by geopolitical tensions and persistent inflation concerns [3]. This rapid repricing has squeezed affordability, particularly in higher-value markets where loan sizes are largest.

Despite this, the market has shown resilience. Sales agreed are running only 4% below the same period last year, when rates were materially lower [1]. The number of homes available for sale is at its highest level since 2015, giving buyers greater choice but simultaneously placing downward pressure on asking prices in oversupplied areas [1]. Approximately 32% of existing listings have seen price reductions, a clear signal that seller expectations in many areas remain misaligned with buyer capacity [1].

💬 "The divergence between northern optimism and London caution in 2026 is not a temporary blip — it reflects a decade-long structural shift in where value is being created in UK residential property."

Regional Housing Recovery Trends: The North West Surge Explained

The North West's outperformance is not accidental. It reflects a confluence of affordability, economic investment, and demographic shifts that have been building for several years — and that RICS Q1 2026 data confirms are now firmly embedded.

Price Growth and Demand Drivers

Annual house price growth in the North West reached 2.6% in the year to May 2026, making it one of the strongest-performing regions in the country [1]. Cities like Manchester, Liverpool, and Salford have attracted sustained inward investment, benefiting from infrastructure improvements, growing graduate retention, and a tech and creative sector that has diversified the economic base beyond traditional industries.

Affordability remains a key structural advantage. With average property prices significantly below the national median, the North West offers buyers — particularly first-time purchasers and those relocating from more expensive regions — genuine value even at current mortgage rates. This relative affordability cushions demand against rate rises in a way that London simply cannot replicate.

Zoopla's 2026 outlook identifies Scotland and Northern England as having the best prospects for growth among UK regions, citing exactly these affordability and demand dynamics [6]. For valuers operating in the North West, this means:

- Comparable evidence is moving upward — recent sales must be weighted carefully against older comparables that may understate current market value.

- New-build premiums are holding firm in regeneration zones, requiring careful analysis when instructing RICS building surveys on properties in these areas.

- Demand from investor buyers remains active, particularly in the private rented sector, which can support valuations in certain property types.

Valuation Adjustment Tactics for Resilient Northern Markets

For registered RICS valuers working in the North West, the practical implication of these regional housing recovery trends is that a conservative, nationally-anchored approach to comparables risks systematic undervaluation. Key adjustments to consider include:

| Factor | Adjustment Approach |

|---|---|

| Time adjustment on comparables | Apply upward adjustments for sales older than 3 months |

| New-build vs second-hand | Maintain distinct comparable pools; avoid cross-contamination |

| Investor yield analysis | Cross-check capital value against rental yields in active BTL zones |

| Regeneration area premiums | Document planning context and infrastructure investment in report |

| Mortgage rate sensitivity | Note affordability stress in commentary even where value is supported |

Understanding the methods of valuation available — from the comparable method to the investment approach — is particularly important in a market where different buyer profiles (owner-occupiers vs. investors) may produce different value conclusions for the same asset.

Regional Housing Recovery Trends: Valuation Adjustments for the London Slump

London's story in 2026 is one of prolonged underperformance that has now tipped into outright decline in many segments. Annual house prices in the capital fell by 2.4% in the year to May 2026 [1] — a figure that, while not catastrophic in isolation, sits within a deeply troubling longer-term context.

A Decade of Underperformance

Between February 2016 and February 2026, London property prices grew by just 10% — compared to 41% nationally [4]. Flats and maisonettes, which dominate London's housing stock, increased by a mere 0.5% over the same decade [4]. For anyone who purchased a London flat in 2016 expecting capital growth in line with broader UK trends, the outcome has been deeply disappointing in real terms.

The reasons are structural and well-documented:

- Affordability exhaustion: London prices reached a ceiling relative to local incomes during the 2010s bull run and have struggled to find a new equilibrium.

- Leasehold complexity and service charge inflation: Escalating service charges and ground rent uncertainty have suppressed flat values in particular.

- Stamp duty drag: Higher transaction costs at London price levels deter discretionary moves, reducing liquidity.

- Remote working: The pandemic-era shift toward larger homes outside city centres has permanently altered some demand patterns.

In April 2026, 46.7% of homes listed were withdrawn unsold, primarily because asking prices were set too high relative to what buyers could or would pay [5]. This overvaluation problem is especially acute in London, where sellers anchored to peak 2014–2016 values are encountering a fundamentally different market.

Practical Valuation Guidance for London Professionals

For surveyors and valuers operating in the capital — whether instructed through chartered surveyors in North London or across other London boroughs — the current environment demands a disciplined, evidence-first approach:

🔴 Key risks to manage:

- Seller-led overvaluation pressure: Clients may challenge downward valuations based on outdated expectations. Robust comparable evidence and clear written justification are essential.

- Leasehold-specific adjustments: Properties with short leases, high service charges, or ground rent escalation clauses require specific downward adjustments. A lease extension valuation may be necessary to properly advise clients on the true cost of ownership.

- Flat market segmentation: The 0.5% decade growth in flats means comparable selection must be hyper-local and property-type specific.

- Tax-related valuation instructions: With prices under pressure, instructions for capital gains tax valuation and ATED valuation purposes require particular care in a declining market, as historic base values and current market values may diverge significantly.

💬 "In a declining market, the temptation to anchor on historic highs is the single greatest source of valuation error. London in 2026 demands that professionals treat each instruction on current evidence alone."

London's Outlook: Flatline Now, Modest Recovery Later

London's property prices are expected to flatline throughout 2026, with modest growth forecast to return from 2027 onward. Cumulative growth of 13.6% by 2030 is projected [4] — meaning the capital is not in terminal decline, but recovery will be gradual. For clients considering investment decisions, this timeline matters enormously for advice on holding periods and financing structures.

Navigating the Divergence: Strategic Considerations for Property Professionals

The contrast captured in these Regional Housing Recovery Trends: Valuation Adjustments for North West Surge vs London Slump in RICS Q1 2026 Surveys creates both risk and opportunity for property professionals across the UK.

Instructed Surveys in a Two-Speed Market

When conducting RICS building surveys in either market, the regional context should inform how condition findings are framed in terms of their market impact. A structural defect in a rising North West market may have a different negotiation dynamic than the same defect in a stagnant London flat market. Understanding the difference between Level 2 and Level 3 surveys helps clients select the right level of scrutiny for their specific property and market context.

Shared Ownership and Affordable Housing Valuations

The regional divergence has particular implications for valuing shared ownership properties. In the North West, rising open market values may increase the cost of staircasing for shared owners. In London, declining values could create situations where shared owners have negative equity on their equity share — a complex scenario requiring careful, compliant valuation advice.

Commercial Property Spillover Effects

The residential divergence is beginning to influence commercial markets too. Retail and leisure investment in North West city centres is being supported by population growth and rising residential confidence. Commercial property surveyors working across both regions will need to account for these macro-residential trends when advising on commercial asset valuations, particularly mixed-use schemes.

What the Data Means for 2026 and Beyond

The RICS Q1 2026 survey data, combined with Rightmove's May 2026 house price index and Zoopla's regional forecasts, points to several durable conclusions:

✅ The North West will continue to outperform as long as affordability advantages persist and economic investment continues. Valuers should expect upward pressure on comparables to continue through 2026.

⚠️ London requires a cautious, evidence-led approach with no assumption of mean reversion in the short term. The structural issues suppressing London values — particularly in the flat sector — will not resolve quickly.

📊 National averages are misleading in 2026. The UK average asking price rose by 1.2% (£4,333) to £378,304 in May 2026, surpassing the ten-year seasonal average [1]. But this national figure masks the North West's outperformance and London's decline — using it as a benchmark for regional valuations would be a material error.

🏦 Mortgage rate sensitivity remains the wildcard. A return of rates toward 4.5% or below would likely unlock suppressed demand nationally. Until that happens, the -34% net balance on buyer enquiries [2] suggests transaction volumes will remain constrained, keeping negotiating power with buyers in most markets.

Conclusion: Actionable Next Steps for Property Professionals

The regional housing recovery trends captured in RICS Q1 2026 surveys demand a fundamental shift in how valuers and surveyors approach their work in 2026. A one-size-fits-all national methodology is no longer fit for purpose when the gap between the North West and London is this pronounced.

Here are the key actions professionals should take now:

-

Recalibrate your comparable databases — ensure your comparable evidence pools are refreshed with 2026 transaction data, particularly in fast-moving North West markets where older data will understate current values.

-

Document regional context in all valuation reports — RICS Red Book compliance requires that market conditions are clearly described. The divergence between regions in 2026 is material and must be reflected in your commentary.

-

Advise clients on realistic timescales — in London, sellers need honest guidance that the 2026 market will not reward optimistic pricing. The 46.7% withdrawal rate [5] is a stark reminder of what overvaluation costs in time and stress.

-

Invest in specialist instruction types — in a complex market, clients increasingly need specialist valuations: capital gains tax valuations, lease extension valuations, and ATED valuations are all areas where accurate, market-aware advice adds significant client value.

-

Stay current with RICS survey releases — the quarterly RICS Residential Market Survey is the most authoritative barometer of regional sentiment. Building it into your professional development routine is non-negotiable.

The divergence of 2026 is not a crisis — it is a market communicating clearly about where value is being created and where it is being eroded. The professionals who listen carefully to that signal, and adjust their practice accordingly, will deliver the most accurate and defensible advice to their clients.

References

[1] May 2026 – https://www.rightmove.co.uk/news/house-price-index/may-2026/?utm_source=openai

[2] Higher Mortgage Rates Hit Buyer Demand – https://mortgagesoup.co.uk/higher-mortgage-rates-hit-buyer-demand/?utm_source=openai

[3] House Prices – https://moneyweek.com/investments/house-prices/house-prices?utm_source=openai

[4] London House Prices – https://moneyweek.com/investments/property/london-house-prices?utm_source=openai

[5] UK House Prices May 2026 South West London Buyer Guide – https://wimbledonsurveyors.com/uk-house-prices-may-2026-south-west-london-buyer-guide/?utm_source=openai

[6] Great Scot Zoopla Identifies Housing Markets With The Best Prospects For – https://www.zoopla.co.uk/press/releases/great-scot-zoopla-identifies-housing-markets-with-the-best-prospects-for/?utm_source=openai