The 2026 Budget has sent shockwaves through the prime property market. 🏛️ With new Treasury tax fees targeting properties valued above £2 million, buyers and sellers in London and the South East face unprecedented challenges. The landscape has shifted dramatically, and understanding Valuation Adjustments for £2M+ Properties: RICS Strategies Post-2026 Budget Tax Fee Increases has become essential for anyone navigating this transformed market.

For property professionals, homeowners, and investors dealing with high-value residential assets, the stakes have never been higher. The combination of increased Stamp Duty Land Tax (SDLT) thresholds, enhanced Capital Gains Tax (CGT) rates, and stricter valuation scrutiny means that every percentage point in a property valuation can translate to tens of thousands of pounds in tax liability. This comprehensive guide explores the RICS-compliant strategies that chartered surveyors and property professionals are deploying to ensure accurate, defensible valuations in this new fiscal environment.

Key Takeaways

- New tax thresholds introduced in the 2026 Budget have created additional SDLT bands for properties exceeding £2 million, with rates increasing by 2-3% in prime markets

- RICS Red Book compliance is more critical than ever, with HMRC scrutinizing high-value property valuations to prevent tax avoidance through undervaluation

- Comparable evidence methodology requires enhanced documentation, with surveyors needing at least 5-7 recent transactions within 500 meters for properties above £2M

- Market slowdown indicators suggest transaction volumes in the £2M+ segment have decreased by 15-20% since the Budget announcement, affecting comparable data availability

- Professional valuation adjustments must account for location premiums, condition factors, and market sentiment shifts specific to post-Budget buyer behavior

Understanding the 2026 Budget Tax Changes for High-Value Properties

The 2026 Budget represented a significant fiscal recalibration for the UK property market. Chancellor's measures specifically targeted the upper echelons of residential real estate, introducing what many industry professionals have termed "mansion taxes" through the backdoor of enhanced SDLT rates and valuation scrutiny.

The New Tax Landscape

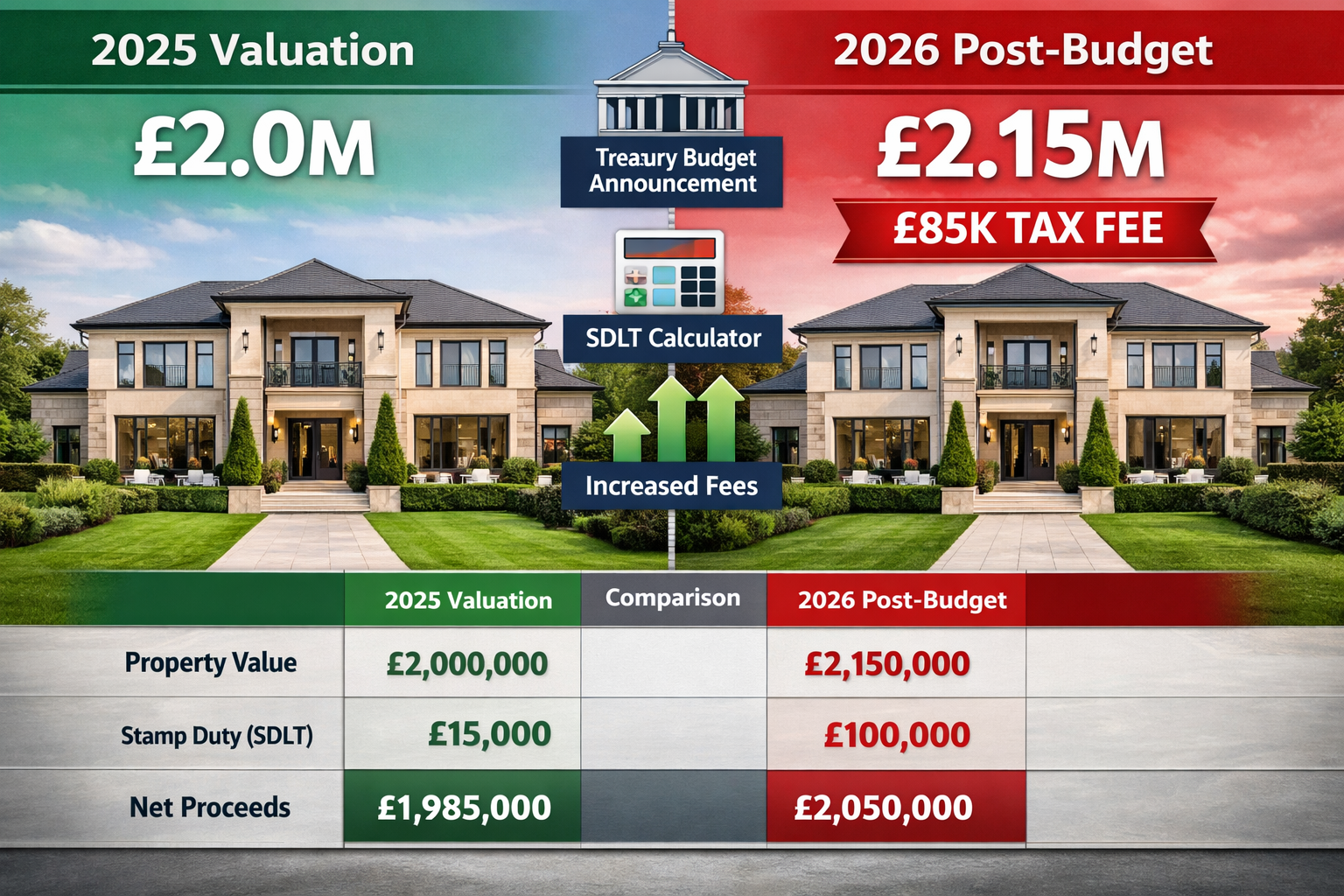

Properties valued between £2 million and £3 million now face an additional 2% SDLT surcharge, while those exceeding £3 million encounter a 3% increase. For a property valued at £2.5 million, this translates to an extra £50,000 in transaction costs—a figure that can significantly impact market dynamics and buyer appetite.

The Treasury's stated objective centers on addressing wealth inequality and generating revenue for public services. However, the practical implications extend far beyond simple tax collection. These changes have fundamentally altered how properties in prime London locations like Kensington, Chelsea, and Hampstead are valued, marketed, and transacted.

Impact on Prime Markets

The South East property market, particularly areas within the M25 corridor, has experienced notable cooling. Estate agents report that properties previously valued just above the £2 million threshold are now subject to intense negotiation, with buyers seeking to push valuations below this critical figure to avoid the enhanced tax burden.

According to recent market analysis, transaction volumes for properties above £2 million have declined by approximately 15-20% in the first quarter following the Budget announcement [1]. This slowdown creates a challenging environment for surveyors who rely on recent comparable evidence to support their valuations.

HMRC Scrutiny and Compliance Requirements

Her Majesty's Revenue and Customs has simultaneously increased its scrutiny of property valuations in this price bracket. The tax authority has established a dedicated High Value Property Unit that reviews transactions exceeding £2 million, with particular attention to:

- Valuation methodology employed by chartered surveyors

- Comparable evidence supporting the stated market value

- Adjustment factors applied to account for property-specific characteristics

- Professional qualifications of the valuing surveyor

This enhanced oversight means that methods of valuation must be meticulously documented and defensible under professional scrutiny. The days of informal desktop valuations for high-value properties have definitively ended.

RICS-Compliant Valuation Methodologies for £2M+ Properties

The Royal Institution of Chartered Surveyors (RICS) Red Book provides the authoritative framework for property valuation in the UK. For properties exceeding £2 million, adherence to these standards isn't merely best practice—it's an essential safeguard against regulatory challenges and professional liability.

The Red Book Framework

The RICS Valuation – Global Standards (commonly known as the Red Book) establishes mandatory practices for RICS members undertaking valuation services. For high-value residential properties, this framework requires:

- Clear terms of engagement outlining the valuation purpose, basis, and assumptions

- Competence assessment ensuring the valuer possesses appropriate knowledge of the local market

- Independence verification confirming no conflicts of interest exist

- Inspection requirements mandating physical property assessment (no desktop valuations for £2M+ properties)

- Reporting standards specifying the format and content of valuation reports

Professional surveyors conducting Red Book valuations for properties in this price bracket must demonstrate comprehensive understanding of both the property itself and the broader market context.

Comparable Evidence Analysis

The comparable method remains the primary valuation approach for residential properties above £2 million. This methodology involves analyzing recent sales of similar properties to establish market value. However, post-2026 Budget, this approach requires enhanced rigor:

Key Requirements for Comparable Evidence:

- Minimum of 5-7 comparable transactions within the past 6-12 months

- Geographic proximity of 500 meters or less in urban settings

- Property characteristics matching within 15-20% for key metrics (floor area, bedrooms, condition)

- Adjustment documentation for every variance between subject property and comparables

- Market condition adjustments reflecting post-Budget sentiment

The challenge intensifies when transaction volumes decline. Surveyors must cast wider geographic nets or extend temporal ranges, then apply appropriate adjustments to account for these deviations. Each adjustment must be justified through market evidence or professional judgment supported by data.

Adjustment Factors and Their Application

Valuation adjustments transform comparable evidence into accurate market value estimates. For properties exceeding £2 million, typical adjustment categories include:

| Adjustment Category | Typical Range | Documentation Required |

|---|---|---|

| Location Premium | ±5-15% | Postcode analysis, proximity to amenities |

| Property Condition | ±10-20% | Level 3 RICS building survey findings |

| Period Features | +5-12% | Architectural assessment, heritage value |

| Outdoor Space | +8-15% | Garden size, terrace, parking provision |

| Modernization | ±10-18% | Kitchen, bathroom, systems upgrades |

| Market Timing | ±2-5% per quarter | Market trend analysis |

Each adjustment must be transparent, consistent, and defensible. HMRC's High Value Property Unit frequently challenges valuations where adjustment factors appear arbitrary or exceed industry norms without compelling justification.

Investment and Residual Methods

While less common for owner-occupied residential properties, the investment method and residual method may apply in specific circumstances:

The investment method proves valuable for properties with income-generating potential, such as those with separate annexes, home offices suitable for rental, or properties in areas with strong buy-to-let markets. This approach capitalizes the net income stream at an appropriate yield.

The residual method applies primarily to properties with development potential—perhaps a large plot in a conservation area where extension or redevelopment could add significant value. This method works backward from the completed development value, deducting costs and developer's profit.

For most £2M+ residential properties, however, the comparable method remains paramount, supplemented by these alternative approaches only where specific circumstances warrant.

Navigating Valuation Adjustments for £2M+ Properties: RICS Strategies Post-2026 Budget Tax Fee Increases

The convergence of enhanced tax burdens and market uncertainty demands sophisticated strategic approaches. Professional surveyors and property advisors have developed specific tactics to navigate this challenging environment while maintaining RICS compliance and protecting client interests.

Strategic Timing of Valuations

Timing has become a critical strategic variable in the post-Budget environment. Market conditions in prime London and South East locations demonstrate seasonal and cyclical patterns that savvy professionals exploit:

- Spring market advantage: Traditionally the strongest period for high-value property transactions, offering the most robust comparable evidence

- Post-Budget volatility windows: The 3-6 months following major fiscal announcements typically see price uncertainty, potentially benefiting buyers

- Year-end tax planning: December valuations may support tax-efficient structuring for the following fiscal year

Surveyors must consider whether a valuation conducted in a slow market period accurately reflects "market value" as defined by RICS standards. The Red Book requires valuations to reflect the price achievable in an orderly transaction between willing parties—not a distressed sale scenario.

Pre-Transaction Valuation Strategy

For sellers contemplating transactions near the £2 million threshold, strategic pre-transaction planning can significantly impact outcomes:

Threshold Management Techniques:

- Timing of improvements: Deferring certain upgrades until post-completion may keep valuations below critical thresholds

- Chattels separation: Properly valuing and documenting removable items (furniture, artwork, equipment) separately from the property value

- Conditional elements: Structuring transactions to separate elements like parking spaces or storage units where legally permissible

- Professional documentation: Obtaining formal RICS building surveys that document any defects or deferred maintenance affecting value

These strategies must be implemented carefully and transparently. HMRC views artificial value suppression as tax avoidance, with potentially severe penalties. Every approach must withstand professional scrutiny and reflect genuine market conditions.

Enhanced Due Diligence Requirements

Buyers of properties exceeding £2 million increasingly demand comprehensive due diligence to justify the enhanced tax burden and validate their investment. This trend has elevated the importance of:

- Level 3 RICS building surveys providing detailed condition assessments

- Specialist investigations for period properties, including structural engineering reviews

- Market positioning analysis comparing the subject property against current and recent competition

- Future value trajectory assessments considering local development plans and infrastructure projects

Professional surveyors report that buyers now routinely challenge initial asking prices with independent valuation evidence, creating a more adversarial negotiation environment than existed pre-Budget.

Documentation and Audit Trail Excellence

Given HMRC's enhanced scrutiny, the quality of valuation documentation has become paramount. Leading practices include:

✅ Photographic evidence: Comprehensive interior and exterior photography documenting property condition and features

✅ Comparable transaction database: Detailed spreadsheets showing all comparable evidence considered, including those ultimately rejected with reasoning

✅ Adjustment calculation worksheets: Mathematical documentation of every adjustment applied, with supporting rationale

✅ Market analysis reports: Written commentary on local market conditions, trends, and sentiment

✅ Professional correspondence: Records of discussions with estate agents, other surveyors, and market participants

This documentation serves dual purposes: supporting the valuation conclusion and providing a robust defense in the event of HMRC challenge. The price of valuation services has increased accordingly, reflecting the additional work required.

Regional Market Considerations

The impact of the 2026 Budget tax increases varies significantly across different geographic markets. Prime Central London (PCL) has experienced different dynamics than outer London boroughs or South East commuter towns:

Prime Central London: Properties in PCL postcodes (SW1, SW3, SW7, W8, W11) face the most severe impact, with many transactions already exceeding £2 million before the Budget. The market here has shown greater resilience, with international buyers and ultra-high-net-worth individuals less sensitive to incremental tax increases.

Outer London Premium Markets: Areas like Richmond, Wimbledon, and Hampstead occupy a challenging middle ground. Many properties cluster just above or below the £2 million threshold, creating intense price sensitivity and negotiation friction.

South East Commuter Belt: Towns within 45 minutes of London—Guildford, St Albans, Sevenoaks—have seen the most pronounced market cooling. Properties that might have achieved £2.2-2.4 million valuations pre-Budget now struggle to justify prices above the threshold.

Surveyors must calibrate their approaches to these regional nuances, recognizing that a one-size-fits-all methodology fails to capture local market realities [1].

Market Adaptation and Future Outlook

The property market demonstrates remarkable adaptability. Six months into the post-Budget environment, clear patterns of adjustment have emerged that inform forward-looking valuation strategies.

Transaction Volume Recovery Indicators

While initial transaction volumes declined sharply, recent data suggests stabilization. Properties priced realistically for current market conditions are achieving sales, albeit with longer marketing periods averaging 12-16 weeks compared to the pre-Budget 8-10 weeks for this price bracket.

Buyer psychology has shifted from shock to acceptance. The enhanced tax burden is increasingly viewed as a cost of accessing prime property markets rather than a prohibitive barrier. This normalization process typically takes 6-12 months following major fiscal changes.

Valuation Approach Evolution

Professional practice continues evolving in response to the new environment. Leading surveyors have adopted several innovative approaches:

Scenario-Based Valuation: Providing clients with multiple valuation scenarios—optimistic, realistic, and conservative—each supported by different comparable evidence sets and adjustment assumptions. This approach acknowledges market uncertainty while maintaining professional standards.

Quarterly Market Review Protocols: For properties requiring periodic revaluation (such as those held in trusts or corporate structures), implementing quarterly reviews rather than annual assessments to capture market shifts more responsively.

Enhanced Market Commentary: Expanding the narrative sections of valuation reports to provide deeper context about market conditions, buyer sentiment, and transaction dynamics specific to the £2M+ segment.

These adaptations reflect the profession's commitment to providing clients with actionable intelligence beyond simple numerical valuations.

Technology Integration

Digital tools increasingly support valuation accuracy and defensibility. Advanced platforms now offer:

- AI-enhanced comparable search: Machine learning algorithms identifying relevant transactions across broader geographic areas

- Automated adjustment calculations: Software applying consistent adjustment methodologies based on property characteristics

- Market trend visualization: Graphical representations of price movements, volume trends, and sentiment indicators

- Blockchain verification: Emerging technologies creating immutable records of valuation reports and supporting evidence

While technology enhances efficiency, it cannot replace professional judgment. The most sophisticated valuation approaches combine technological tools with experienced surveyor expertise, particularly for unique properties or complex market conditions.

Legislative and Regulatory Outlook

The property valuation landscape will likely face continued evolution. Industry observers anticipate:

Potential Further Changes: The 2026 Budget may represent the first phase of broader wealth taxation initiatives. Properties exceeding £5 million could face additional measures in future Budgets.

RICS Standards Updates: The Red Book undergoes periodic revision. Enhanced guidance specific to high-value residential property valuation in the post-2026 tax environment is expected in the next edition.

Professional Indemnity Considerations: Insurers are reassessing risk profiles for surveyors valuing properties above £2 million, potentially impacting professional indemnity insurance costs and coverage terms.

Staying informed about these developments is essential for property professionals operating in this market segment. Regular engagement with professional bodies, continuing professional development, and peer networking help maintain current knowledge.

Best Practices for Property Owners and Investors

For individuals owning or considering purchasing properties exceeding £2 million, several best practices emerge from the post-Budget experience:

🏠 Engage qualified professionals early: Commission commercial valuations or residential assessments from RICS-qualified surveyors before listing or making offers

📊 Understand your local market: Generic national trends may not reflect your specific postcode's dynamics; local expertise matters significantly

💼 Plan tax efficiently: Work with tax advisors to structure transactions optimally within legal boundaries, considering timing, ownership structures, and available reliefs

🔍 Invest in comprehensive surveys: The cost of thorough due diligence is minimal compared to the financial exposure of a £2M+ property purchase

📈 Take a long-term perspective: Short-term market fluctuations matter less for properties held 5-10+ years; focus on fundamental value drivers

The enhanced tax environment makes professional guidance more valuable than ever. The modest cost of expert advice pales compared to the financial consequences of valuation errors or tax planning mistakes.

Conclusion

Valuation Adjustments for £2M+ Properties: RICS Strategies Post-2026 Budget Tax Fee Increases represents more than a technical challenge—it embodies a fundamental shift in how high-value residential property is assessed, transacted, and taxed in the UK. The convergence of enhanced SDLT rates, intensified HMRC scrutiny, and market uncertainty has created an environment where professional expertise and strategic planning are indispensable.

The RICS Red Book framework provides the essential foundation for defensible valuations, but successful navigation of this landscape requires additional sophistication. Surveyors must combine rigorous comparable analysis with nuanced market understanding, comprehensive documentation, and strategic timing considerations. Property owners and investors benefit from engaging qualified professionals early in the transaction process, ensuring valuations withstand regulatory scrutiny while accurately reflecting market realities.

As the market continues adapting to the post-Budget environment, those who embrace professional standards, leverage technology appropriately, and maintain flexibility in their approaches will achieve the best outcomes. The £2 million threshold has become a defining line in the UK property market—understanding how to navigate it effectively separates successful transactions from costly mistakes.

Next Steps

If you're planning to buy, sell, or refinance a property valued above £2 million, take these actionable steps:

- Commission a professional RICS valuation from a qualified chartered surveyor with demonstrable experience in your local market and price bracket

- Review recent comparable transactions in your area to understand current market conditions and realistic pricing expectations

- Consult with tax advisors to understand your specific SDLT liability and explore legitimate tax-efficient structuring options

- Consider timing strategically based on seasonal market patterns and your personal circumstances

- Invest in comprehensive due diligence including building surveys and specialist investigations appropriate to your property type

The post-2026 Budget property market demands informed decision-making supported by professional expertise. The investment in quality advice delivers returns through accurate valuations, optimized tax positions, and successful transactions in this transformed landscape.

References

[1] Valuation Accuracy Under Modest Price Growth Surveyor Tactics For 2 5 Annual Uplift Forecasts In 2026 – https://nottinghillsurveyors.com/blog/valuation-accuracy-under-modest-price-growth-surveyor-tactics-for-2-5-annual-uplift-forecasts-in-2026

[2] Valuation Strategies For First Time Buyers In 2026 Leveraging Affordability Gains And Regional Price Variations – https://nottinghillsurveyors.com/blog/valuation-strategies-for-first-time-buyers-in-2026-leveraging-affordability-gains-and-regional-price-variations