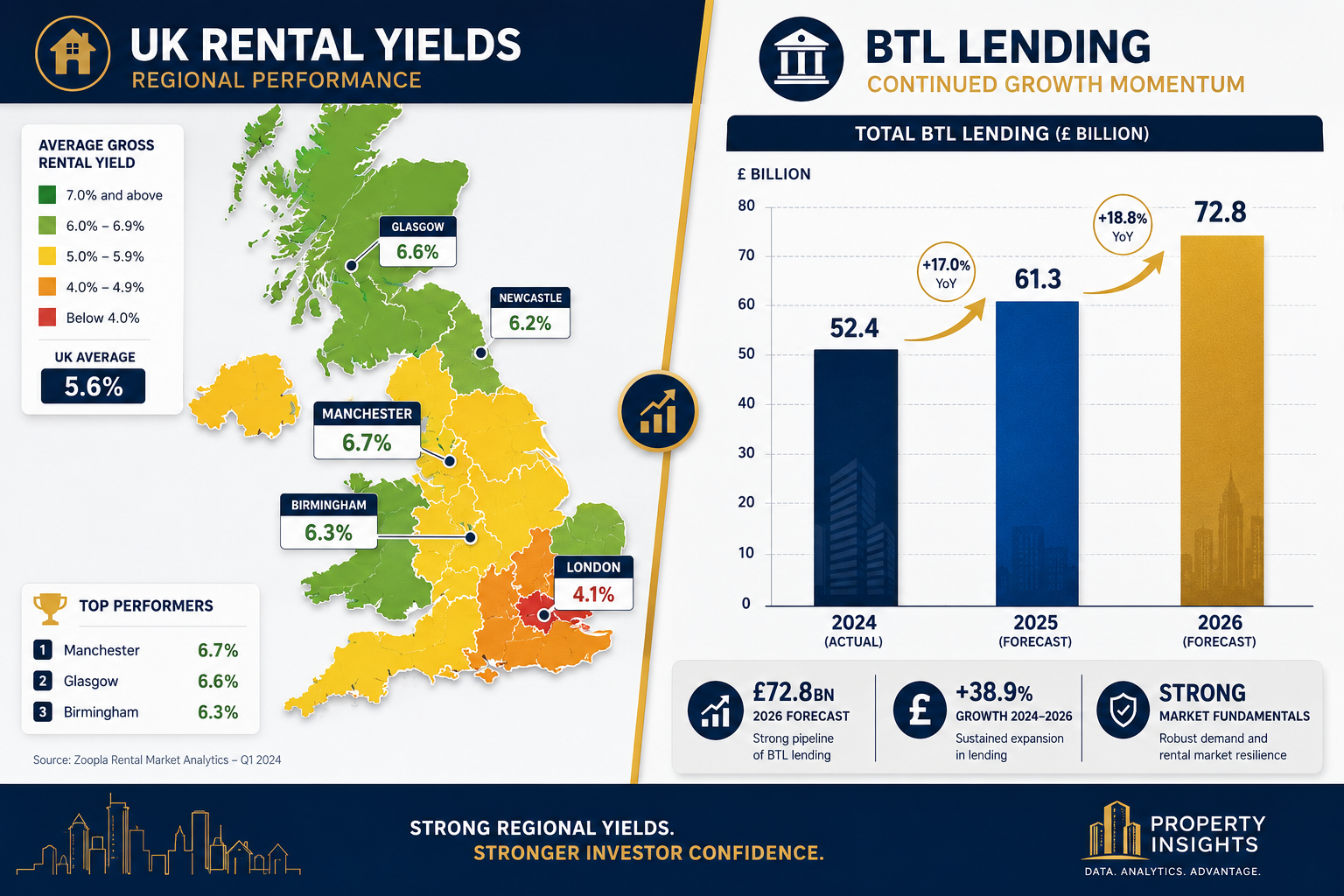

By Q3 2025, buy-to-let lending had climbed to £6.6 billion — a 7% quarterly increase that signalled a decisive shift in who controls the UK rental market [1]. The exit of individual landlords, accelerated by a 47% income tax rate on rental income, has handed institutional investors a structural advantage they are moving quickly to exploit [2]. For professional investors acquiring or managing large residential portfolios, the challenge is no longer simply finding properties. It is valuing them accurately, at scale, with full visibility of risk.

Valuing Institutional Buy-to-Let Portfolios in 2026: Risk-Adjusted Surveys for Professional Investors is therefore not a theoretical exercise. It is a practical discipline that determines whether a portfolio generates sustainable returns or quietly accumulates hidden liabilities.

Key Takeaways

- Institutional investors now dominate UK BTL acquisition, requiring survey methodologies that go far beyond standard residential checks.

- Risk-adjusted valuations must incorporate yield sustainability, regulatory compliance, structural condition, and regional demand data simultaneously.

- The Renters' Rights Act 2026 and enhanced EPC requirements have introduced new risk profiles that directly affect capitalisation rates.

- RICS survey data from early 2026 shows strong rental price expectations (+20% net balance) alongside near-term capital value caution (-18% net balance).

- Professional investors benefit most from structured, repeatable survey frameworks that can be applied consistently across large multi-property portfolios.

Why Institutional Investors Now Drive BTL Valuation Standards

The composition of the UK buy-to-let market has changed fundamentally. Where individual landlords once dominated, institutional investors — pension funds, real estate investment trusts, and dedicated build-to-rent operators — now set the pace [1]. This shift carries direct implications for how properties are surveyed and valued.

Individual landlords typically relied on basic mortgage valuations or Level 2 homebuyer reports. Institutional buyers cannot afford that approach. A single acquisition may involve dozens or hundreds of units across multiple regions, each carrying its own structural profile, tenancy arrangement, and compliance status. Errors at the survey stage compound across the portfolio, turning manageable risks into material losses.

Three forces are reshaping valuation standards in 2026:

-

Tax-driven market consolidation — The 47% income tax rate on rental income has prompted a wave of individual landlord exits, creating acquisition pipelines that institutions are well-positioned to absorb [2]. These portfolios often arrive with mixed quality standards, making thorough due diligence essential.

-

Renewed investor confidence — CBRE's Q4 2025 Multifamily Underwriting Survey found that 76% of respondents reported positive sentiment toward core multifamily acquisitions, up sharply from 44% the prior year [3]. That confidence must be grounded in reliable data.

-

Private market allocation growth — Nuveen's 2026 Global Institutional Investor Survey found that 81% of institutional investors plan to increase private market allocations over the next five years [5]. Residential real estate sits at the heart of those strategies.

For surveyors and investors alike, these trends make stock condition surveys and structured portfolio assessments the baseline expectation, not an optional extra.

The Core Components of Risk-Adjusted Survey Methodology

Valuing institutional buy-to-let portfolios in 2026 through a risk-adjusted lens means treating the survey as a multi-layered financial instrument, not just a physical inspection. A credible methodology integrates at least four distinct assessment layers.

Structural and Physical Condition Assessment

The physical fabric of each property underpins every other metric. Structural defects, damp ingress, roof deterioration, and non-standard construction all affect both reinstatement costs and long-term yield reliability. For large portfolios, a tiered inspection approach is standard: desktop screening first, followed by targeted physical surveys on higher-risk units.

Surveyors should apply consistent grading criteria across all units, enabling portfolio-level aggregation of condition risk. A single property with severe damp may be manageable; ten properties with the same issue across a 50-unit portfolio represents a material capital expenditure liability. Understanding the true cost of damp surveys and structural checks is essential when budgeting due diligence for large acquisitions.

For properties where physical access is difficult — rooftop plant, large commercial roofs, or multi-storey blocks — drone survey technology now provides cost-effective visual inspection data that can be integrated into portfolio condition reports.

Yield Sustainability and Rental Income Modelling

Physical condition alone does not determine value. Rental income is projected to grow by 12% through 2031, but that headline figure masks significant regional variation [4]. Institutional valuations must model yield sustainability under multiple scenarios, including:

- Base case: Current passing rent maintained, vacancy rate at market average

- Stress case: Regulatory-driven rent caps or increased void periods

- Upside case: Rental growth in line with RICS projections

The February 2026 RICS Residential Market Survey reported a strong +20% net balance for rental price expectations over the next three months, alongside near-term capital value expectations of -18% [4]. This divergence — rising rents against cautious capital values — is precisely the kind of nuance that risk-adjusted modelling must capture.

Understanding methods of valuation appropriate to income-producing assets, including the investment method and discounted cash flow analysis, is fundamental to this layer of the survey process.

Regulatory Compliance and ESG Risk

Regulatory risk has become one of the most significant value drivers in institutional BTL portfolios. The Renters' Rights Act 2026 has introduced new tenancy protections that alter the risk profile of possession proceedings and rental adjustment mechanisms, requiring direct adjustments to capitalisation rates [7].

ESG compliance adds a further layer. Enhanced EPC requirements mean that properties below the minimum energy efficiency standard face either significant retrofit costs or removal from the lettable pool. Selective licensing schemes in multiple local authority areas add operational cost and administrative complexity.

Key compliance checks in a 2026 institutional survey:

| Compliance Area | Risk Level | Valuation Impact |

|---|---|---|

| EPC rating (minimum Band C target) | High | Retrofit cost deducted from gross yield |

| Renters' Rights Act 2026 tenancy terms | High | Capitalisation rate adjustment |

| HMO licensing (where applicable) | Medium | Licensing fee and compliance cost provision |

| Selective licensing schemes | Medium | Operational cost uplift |

| Fire safety (multi-storey blocks) | High | Potential major works liability |

| Asbestos management plans | Medium | Remediation cost provision |

Institutional investors are increasingly prioritising ESG factors in property valuations, with EPC compliance costs and licensing fees becoming significant line items in yield calculations [4]. Surveyors who cannot quantify these costs with precision are not providing institutional-grade advice.

Tenant Demand and Location Analysis

A property's value is ultimately anchored to demand. Regional performance data from RICS and other sources must be integrated into portfolio valuations to ensure that yield assumptions reflect local market conditions rather than national averages.

Investors are actively reassessing regional exposures to manage concentration risk, with diversification strategies increasingly informed by granular demand metrics [5]. A portfolio heavily weighted toward a single local authority or employment catchment carries concentration risk that a well-structured survey framework will flag explicitly.

Applying Risk-Adjusted Surveys Across Large Portfolios

The practical challenge of valuing institutional buy-to-let portfolios in 2026 with risk-adjusted surveys for professional investors is one of consistency and scalability. A methodology that works for a single property must be adapted to function reliably across 50, 100, or 500 units without losing analytical rigour.

Tiered Survey Frameworks

Most institutional investors adopt a tiered approach to portfolio surveys:

Tier 1 — Desktop and data review: EPC registers, planning history, title documentation, tenancy schedules, and local authority licensing records are reviewed before any physical inspection. This layer identifies obvious red flags at low cost.

Tier 2 — Condition sampling: A statistically representative sample of units undergoes physical inspection. Sample size is determined by portfolio homogeneity; a portfolio of identical purpose-built flats requires a smaller sample than a mixed portfolio of Victorian terraces and 1970s semi-detached properties.

Tier 3 — Full individual surveys: Units flagged by Tier 1 or Tier 2 as higher risk receive comprehensive individual surveys. For leasehold properties, this includes review of service charge accounts, major works schedules, and lease terms. Understanding the implications of freehold valuation versus leasehold structures is particularly important for blocks of flats.

Integrating Survey Findings into Valuation Models

Survey findings must feed directly into the valuation model, not sit in a separate report that the investment team never reads. The most effective frameworks assign a financial value to each risk identified:

- Structural defects: Estimated remediation cost, discounted to present value

- EPC compliance gap: Retrofit cost estimate, phased over projected ownership period

- Regulatory risk: Capitalisation rate adjustment, expressed in basis points

- Void risk: Sensitivity analysis on occupancy assumptions

This integration ensures that the final portfolio valuation reflects actual risk exposure rather than an optimistic projection based on passing rent alone.

For portfolios containing commercial elements — ground-floor retail, mixed-use blocks, or purpose-built student accommodation — commercial valuation principles apply alongside residential methodology, adding a further layer of complexity that requires specialist input.

The Role of Monitoring Surveys

Institutional portfolio management does not end at acquisition. Ongoing monitoring surveys provide the performance data needed to manage assets actively, identify deteriorating units before they become expensive liabilities, and demonstrate compliance to lenders and regulators.

A well-structured monitoring programme also generates the longitudinal condition data that improves future acquisition surveys, creating a feedback loop that sharpens valuation accuracy over time.

Regional Performance Data and Portfolio Diversification

Valuing institutional buy-to-let portfolios in 2026 requires regional granularity that national averages cannot provide. The RICS February 2026 data showing a +33% twelve-month price expectation alongside a -18% near-term expectation illustrates how short-term and long-term signals can point in opposite directions [4]. Regional markets diverge even more sharply.

Key regional considerations for 2026 portfolio valuations:

- Northern England and the Midlands: Stronger gross yields but higher void risk in some sub-markets; infrastructure investment pipelines support long-term demand forecasts.

- London and the South East: Lower gross yields but greater liquidity and deeper tenant demand pools; EPC compliance costs are proportionally higher given older stock.

- University cities: Consistent demand but regulatory exposure through HMO licensing and potential Article 4 Direction restrictions.

- Coastal and rural markets: Higher yield potential but thinner liquidity; concentration risk is elevated.

J.P. Morgan Asset Management's Q1 2026 Alternatives Relative Value Outlook notes that commercial real estate valuations are recovering broadly, with improving fundamentals and lower debt costs strengthening the overall outlook [6]. For residential BTL portfolios, the parallel improvement in rental fundamentals supports a cautiously optimistic valuation stance — provided that regional risk is properly disaggregated.

Investors diversifying geographically should ensure that survey methodologies are calibrated to local market conditions. A structural survey standard appropriate for London mansion blocks is not automatically appropriate for northern terraced housing stock. Working with local chartered surveyors who understand regional construction types, planning environments, and tenant demand patterns adds material value to the due diligence process.

Common Valuation Errors and How to Avoid Them

Even experienced institutional investors make systematic errors in portfolio valuation. The most costly include:

Over-reliance on passing rent: Passing rent reflects the current tenancy, not the sustainable market rent. Valuations based on above-market passing rents will overstate yield and understate void risk when those tenancies end.

Ignoring lease structure in leasehold portfolios: Short leases, onerous ground rent clauses, and pending major works can each materially reduce value. The cost implications of lease extensions must be factored into any leasehold portfolio valuation.

Treating ESG compliance as a future problem: Retrofit costs that are deferred do not disappear. They accumulate interest and regulatory urgency. Valuations that exclude EPC compliance costs are systematically overstating net asset value.

Applying uniform capitalisation rates across heterogeneous portfolios: A single cap rate applied to a mixed portfolio of HMOs, standard ASTs, and purpose-built flats will produce a misleading aggregate value. Each asset class carries a distinct risk profile that warrants a distinct rate.

Underestimating dilapidations exposure: For portfolios with significant tenant turnover history, schedule of dilapidations analysis should inform both the condition assessment and the financial model.

Conclusion

The professionalisation of the UK buy-to-let market has made rigorous, risk-adjusted survey methodology a commercial necessity for institutional investors. Valuing institutional buy-to-let portfolios in 2026 through the lens of risk-adjusted surveys for professional investors means combining physical condition assessment, yield modelling, regulatory compliance analysis, and regional demand data into a single, integrated framework.

Actionable next steps for professional investors and their advisers:

- Commission tiered portfolio surveys before any significant acquisition, ensuring that sample sizes and inspection depths reflect the heterogeneity of the portfolio.

- Quantify regulatory risk in financial terms — EPC compliance costs, licensing fees, and Renters' Rights Act implications should appear as line items in the valuation model, not footnotes.

- Disaggregate regional performance data rather than relying on national yield averages; local demand metrics and planning environments materially affect sustainable yield assumptions.

- Establish a monitoring survey programme post-acquisition to track condition changes, maintain lender compliance, and generate the longitudinal data that improves future valuations.

- Engage RICS-registered valuers with demonstrable experience in institutional residential portfolios; the complexity of 2026's regulatory and market environment demands specialist expertise.

The investors who will generate the strongest risk-adjusted returns from UK residential portfolios in 2026 and beyond are those who treat the survey not as a cost to be minimised, but as the analytical foundation on which every other investment decision rests.

References

[1] Building Surveys For Institutional Buy To Let Portfolios Assessing Quality Standards When Professional Landlords Dominate 2026 Market – https://www.canterburysurveyors.com/blog/building-surveys-for-institutional-buy-to-let-portfolios-assessing-quality-standards-when-professional-landlords-dominate-2026-market/?utm_source=openai

[2] Valuation Adjustments For 2026 Buy To Let Institutional Surge Surveyor Checklists For Professional Landlord Investments – https://wimbledonsurveyors.com/valuation-adjustments-for-2026-buy-to-let-institutional-surge-surveyor-checklists-for-professional-landlord-investments/?utm_source=openai

[3] Valuing Buy To Let Properties In 2026 Surveys For Institutional Investors Amid Market Rebound – https://nottinghillsurveyors.com/blog/valuing-buy-to-let-properties-in-2026-surveys-for-institutional-investors-amid-market-rebound?utm_source=openai

[4] Valuation Surveys For Professional Buy To Let Investments Assessing Yields In 2026s Bullish Landlord Market – https://nottinghillsurveyors.com/blog/valuation-surveys-for-professional-buy-to-let-investments-assessing-yields-in-2026s-bullish-landlord-market?utm_source=openai

[5] Equilibrium – https://www.nuveen.com/global/insights/equilibrium?utm_source=openai

[6] Aiss Outlook – https://am.jpmorgan.com/se/en/asset-management/institutional/insights/portfolio-insights/alternatives/aiss-outlook/?utm_source=openai

[7] Valuing Buy To Let Properties In 2026 Lettings Surge Surveyor Strategies For Tenant Demand 2 – https://kingstonsurveyors.com/valuing-buy-to-let-properties-in-2026-lettings-surge-surveyor-strategies-for-tenant-demand-2/?utm_source=openai