When UK house price growth settles into the 4-5% annual range, the margin for error in property valuation narrows sharply. Subdued transaction volumes, compressed price differentials between comparable properties, and cautious buyer sentiment combine to create a deceptively complex environment. Evergreen RICS valuation techniques for flat markets: surveyor tools when national growth hits 4-5% are not simply fallback strategies — they are the professional bedrock that separates defensible, court-ready valuations from guesswork dressed up in formal reports. This article examines those techniques in depth, explains the adjustment frameworks that matter most in stable conditions, and identifies the red flags that can distort even the most carefully constructed opinion of value.

Key Takeaways

- In flat 4-5% growth markets, comparable evidence must be scrutinised more carefully because price gaps between properties are narrower and errors compound faster.

- All five core RICS valuation methods remain relevant in subdued markets, but the comparable and investment methods carry the heaviest evidential burden.

- Conservative yield assumptions and realistic profit margins are essential when using the investment and residual methods respectively.

- Red flags including thin transaction volumes, distressed sales contaminating comparable pools, and lease length issues require explicit adjustment frameworks.

- RICS Red Book compliance is non-negotiable regardless of market conditions, and professional indemnity risk rises when valuers cut corners during low-growth periods.

Why Flat Markets Demand Greater Valuation Rigour

A property market growing at 4-5% annually can appear straightforward. Prices are not collapsing, transactions are still occurring, and lenders remain broadly active. However, this apparent stability conceals several hazards that make accurate valuation harder, not easier.

In a rising market, modest errors in comparable selection tend to be absorbed by subsequent price growth. In a flat market, those same errors persist. A comparable that is six months old in a 10% annual growth environment might require a 5% upward time adjustment. In a 4-5% market, the same comparable requires only a 2-2.5% adjustment — but the precision demanded to justify even that figure is significantly greater, because the adjustment itself is smaller relative to any margin of error in the comparable's condition or specification.

Transaction volumes also thin out during flat periods. Buyers and sellers often sit on their hands when they perceive little urgency, which means the pool of usable comparables shrinks. Surveyors working in areas such as North London or Surrey will recognise this dynamic: micro-markets within those regions can see transaction volumes drop by 20-30% during nationally flat periods, leaving valuers with stale or unrepresentative evidence.

The broader economic context reinforces the need for rigour. The U.S. Bureau of Economic Analysis reported that the American economy expanded at an annualised rate of just 1.6% in Q1 2026 [1], while the IMF projects U.S. GDP growth of 2.4% for the full year [2]. Although these are US figures, they reflect a global pattern of moderating growth that feeds directly into investor confidence, cross-border capital flows, and ultimately UK commercial and residential property demand. Surveyors cannot afford to treat macroeconomic data as background noise.

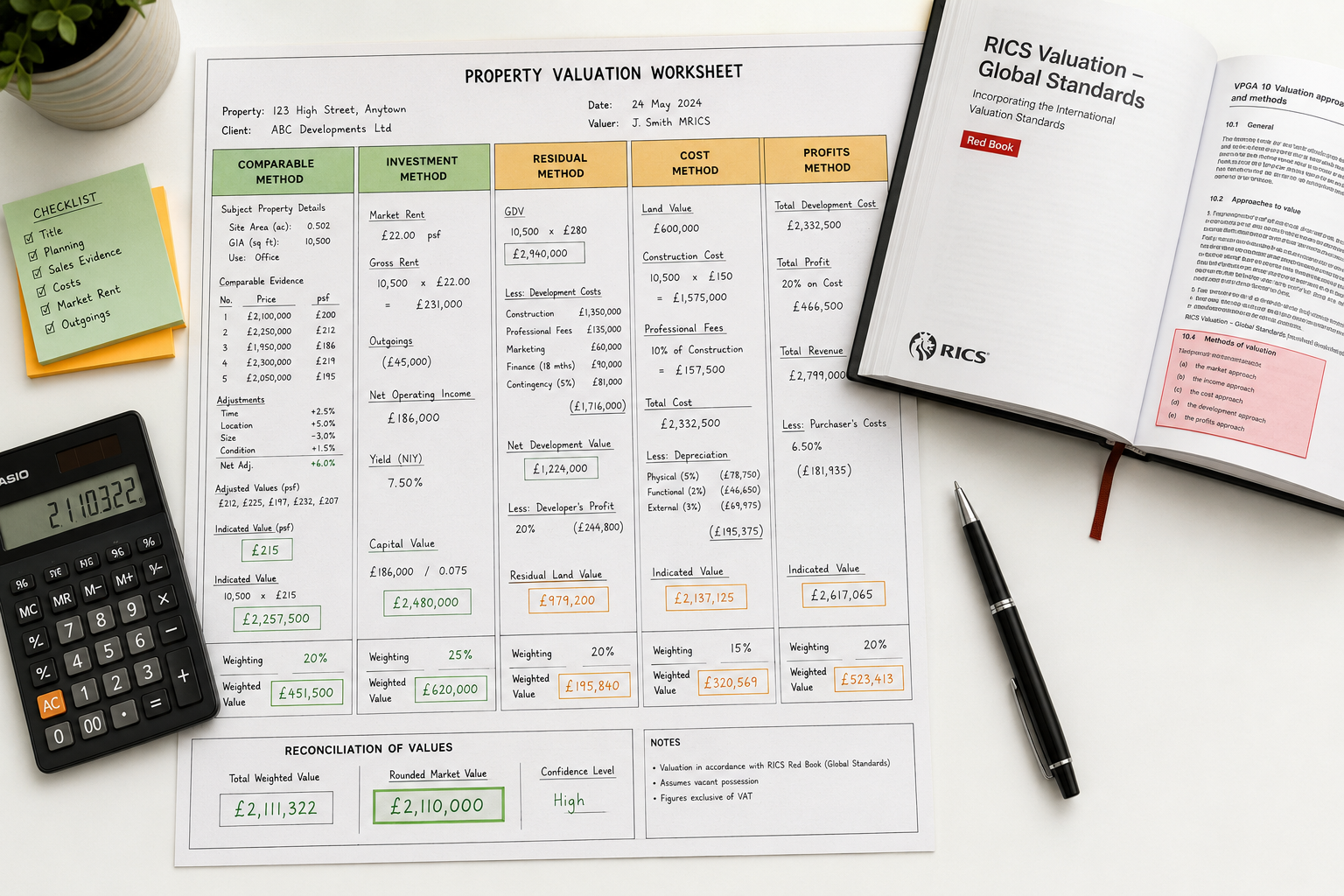

The Five Core RICS Methods and How They Perform in Flat Conditions

The RICS Valuation — Global Standards (the Red Book) recognises five principal methods of valuation. Each behaves differently when national growth is constrained to the 4-5% band.

The Comparable Method

The comparable method is the most widely used approach for residential property and many commercial assets. It involves identifying recent sales of similar properties and adjusting for differences in size, condition, location, and specification.

In flat markets, the comparable method is both the most reliable and the most demanding tool available. Because price differences between properties are compressed, the quality of adjustment reasoning must be exceptionally robust. Key considerations include:

- Recency: Comparables older than three months should be treated with caution and explicitly time-adjusted, even if the adjustment is modest.

- Contamination risk: Distressed sales (repossessions, probate disposals, or sales under time pressure) can drag comparable evidence downward. These must be identified and either excluded or adjusted. For guidance on how valuation factors interact with comparable selection, professional advice is essential.

- Leasehold complications: Short leases create significant value discounts that can corrupt a comparable pool if not identified. A flat with 75 years remaining is not comparable to one with 125 years, and the adjustment is non-trivial. Surveyors handling lease extension valuation work will be familiar with the scale of these adjustments.

The Investment Method

Used primarily for income-generating properties — commercial units, buy-to-let residential, and mixed-use assets — the investment method capitalises net rental income at an appropriate yield to produce a capital value.

In flat markets, two pressures operate simultaneously. First, rental growth may itself be subdued, meaning the income figure is conservative. Second, investors seeking yield in a low-growth environment may compress yields (driving values up) or widen them (driving values down) depending on their risk appetite. Surveyors must resist the temptation to adopt the most recent transactional yield without interrogating whether that yield reflects a sustainable market position or a one-off anomaly.

"In a flat market, the yield assumption carries more weight than in any other condition. A 25 basis point error in yield on a commercial asset worth £2 million can move the valuation by £100,000 or more."

For commercial assets, a RICS commercial building survey conducted alongside the valuation can identify physical defects that justify yield adjustments — a step that is easily overlooked when market conditions appear stable.

The Residual Method

The residual method is used for development land and properties with development potential. It works by estimating the gross development value (GDV) of the completed scheme, then deducting all development costs and a developer's profit margin to arrive at the residual land value.

Flat market conditions make the residual method particularly sensitive to input assumptions. If GDV growth is only 4-5%, a developer's profit margin that was viable at 7% annual growth may be unachievable. Surveyors must stress-test their GDV assumptions against realistic absorption rates and ensure that build cost estimates reflect current tender prices rather than historical benchmarks.

The Cost Method (Depreciated Replacement Cost)

The cost method estimates the current cost of constructing an equivalent building, then applies depreciation to reflect age, condition, and obsolescence. It is most appropriate for specialised properties — schools, hospitals, utilities infrastructure — where market comparables are scarce.

In flat markets, the cost method becomes more relevant for a wider range of properties simply because comparable evidence thins out. Surveyors should ensure that depreciation allowances are not mechanically applied but are instead grounded in physical inspection findings. A RICS Level 3 building survey provides the granular condition data needed to support defensible depreciation calculations.

The Profits Method

The profits method values a property by reference to the trading performance of the business it houses — hotels, pubs, petrol stations, and cinemas are typical examples. It requires the valuer to assess maintainable annual turnover, apply appropriate expense ratios, and capitalise the resulting fair maintainable operating profit.

In flat market conditions, the profits method demands particular conservatism. Businesses in discretionary spending sectors are often the first to feel consumer caution. Surveyors should use three-year average trading figures rather than peak-year data, and should apply sensitivity analysis to occupancy rates and average spend assumptions.

Applying Evergreen RICS Valuation Techniques for Flat Markets: Adjustment Frameworks and Red Flags

The practical application of evergreen RICS valuation techniques for flat markets — surveyor tools when national growth hits 4-5% — requires more than method selection. It requires a structured approach to adjustments and a disciplined eye for red flags that can undermine an otherwise sound analysis.

Adjustment Frameworks for Flat Market Conditions

Time adjustments in a 4-5% growth environment should be calculated on a monthly basis rather than rounded to quarterly periods. At 4% annual growth, the monthly increment is approximately 0.33%. Applying a 1% time adjustment to a comparable that is actually three months old, rather than the correct 1%, introduces a small but compounding error.

Condition adjustments carry greater relative weight in flat markets. When overall price growth is modest, a property in poor condition may trade at a 10-15% discount to an equivalent well-maintained property — a gap that is proportionally larger than in a rising market. Surveyors should obtain detailed condition evidence, and where a homebuyer survey has been carried out on a comparable property, that information (where available) can inform adjustment reasoning.

Specification adjustments — for features such as parking, garden size, energy performance certificates, and kitchen quality — should be benchmarked against local buyer preference data rather than national averages. In a flat market, buyer selectivity increases, meaning specification premiums and discounts are more pronounced and more stable.

The table below summarises the key adjustment categories and their relative importance by market condition:

| Adjustment Type | Rising Market (7%+) | Flat Market (4-5%) | Falling Market |

|---|---|---|---|

| Time adjustment | High importance | Moderate importance | Critical importance |

| Condition adjustment | Moderate | High | Very high |

| Specification adjustment | Low-moderate | High | High |

| Lease length (leasehold) | Moderate | Very high | Very high |

| Location micro-adjustment | Low | High | High |

Red Flags That Distort Flat Market Valuations

Several red flags appear with greater frequency — or greater impact — during flat market conditions:

Thin comparable pools. When fewer than three genuinely comparable sales are available within a 12-month window, the valuer must either widen the search area, extend the time window with appropriate adjustments, or explicitly acknowledge the limitations of the evidence base in the report. Attempting to present a thin pool as robust evidence is a professional indemnity risk.

Distressed sale contamination. Probate sales, repossessions, and matrimonial settlement disposals can all generate below-market evidence. A probate valuation or divorce valuation conducted by a RICS-registered valuer will include explicit commentary on whether the disposal price reflects market value — but when such properties appear as comparables in a third-party valuation, that context is often lost.

Lease length drift. In a flat market with subdued transaction activity, leaseholders are less likely to extend leases proactively. This means the average unexpired lease term across a comparable pool can drift downward over time, gradually eroding the validity of comparisons. Surveyors should check lease lengths on every comparable, not just the subject property.

Overreliance on automated valuation models (AVMs). AVMs perform reasonably well in active, homogeneous markets. In flat markets with thin transaction volumes, their error rates increase significantly. A desktop house valuation can serve as a useful cross-check, but it should never substitute for a full RICS inspection-based valuation in complex or high-value cases.

Ignoring physical defects. In a rising market, buyers often overlook defects because they expect value growth to outpace repair costs. In a flat market, defects become genuine value detractors. Issues such as damp, structural movement, or drainage problems can suppress value by amounts that exceed the cost of remediation. A damp survey or drainage survey can quantify these risks and provide the evidence base for defensible downward adjustments.

Evergreen RICS Valuation Techniques for Flat Markets: Professional Standards and Practical Workflow

Maintaining compliance with RICS professional standards is not merely a regulatory obligation — it is the practical foundation that makes valuations defensible under challenge. The Red Book valuation framework sets out the requirements for inspection, research, analysis, and reporting that apply regardless of market conditions.

In flat markets, the workflow implications of these standards become more demanding in several respects.

Documentation and Evidence Trails

Every adjustment made in a flat market valuation should be documented with explicit reasoning. The narrower the price differentials between comparables and the subject property, the more important it becomes to show that each adjustment was grounded in evidence rather than judgement alone. Surveyors should retain:

- Printed or downloaded evidence of comparable transactions from Land Registry and EPC registers

- Notes from any conversations with local agents about market conditions

- Photographs of the subject property and, where possible, comparables

- Records of any comparable evidence that was considered but rejected, with reasons

Sensitivity Analysis

In flat market conditions, sensitivity analysis is a valuable addition to any valuation report, particularly for investment or development properties. Presenting a base-case valuation alongside a modest downside scenario (for example, a 50 basis point yield widening or a 5% reduction in GDV) demonstrates professional rigour and helps clients understand the range of outcomes they face.

Fee Transparency

Clients in flat markets are often more cost-conscious, which can create pressure on surveyor fees. However, reducing the scope of a valuation to compete on price introduces professional risk. Surveyors should be transparent about what a given fee level covers and direct clients to resources such as surveyor pricing guides so that fee expectations are set appropriately from the outset.

The Macroeconomic Context for 2026 and Its Valuation Implications

The 4-5% growth scenario does not exist in isolation. In 2026, the broader economic backdrop includes moderating growth in major economies, with the IMF projecting U.S. GDP growth of 2.4% for the year [2] and Q1 2026 U.S. GDP expanding at just 1.6% annualised [1]. AI sector investment has provided some upside momentum [3], but this has not translated uniformly into property market confidence.

For UK surveyors, the practical implications include:

- Commercial property valuations face headwinds from occupier caution, particularly in retail and secondary office sectors where hybrid working patterns continue to suppress demand.

- Residential valuations in commuter belt locations may be more sensitive to employment data than in previous cycles, as remote working flexibility fluctuates with employer policy changes.

- Development land valuations require careful scrutiny of planning consent timelines and infrastructure delivery commitments, both of which can extend in a low-growth environment as public sector budgets tighten.

Surveyors operating across regions — from West London to Essex — will observe that even within a nationally flat market, micro-market conditions vary considerably. A 4-5% national average can mask 8% growth in one postcode and 1% in another. The evergreen principle here is that national data informs context but never substitutes for local evidence.

Conclusion

Flat markets are not easy markets. The evergreen RICS valuation techniques for flat markets — surveyor tools when national growth hits 4-5% — demand greater precision, more rigorous documentation, and a sharper eye for the red flags that can corrupt comparable evidence or distort method outputs. The five core RICS methods remain valid and valuable, but their application in subdued conditions requires conservative assumptions, explicit sensitivity analysis, and a disciplined approach to adjustment frameworks.

Actionable next steps for practising surveyors in 2026:

- Audit your comparable selection process to ensure distressed sales are identified and either excluded or explicitly adjusted.

- Review lease length data across your comparable pools, particularly in leasehold-heavy markets.

- Adopt a formal sensitivity analysis template for investment and development valuations to demonstrate the range of outcomes to clients.

- Ensure physical defect evidence — from damp, drainage, or structural surveys — is integrated into your adjustment reasoning rather than treated as a separate report.

- Stay current with RICS Red Book updates and ensure your documentation trails meet the evidential standard required for professional indemnity defence.

The surveyors who maintain rigorous standards during flat market conditions are precisely those who build the reputations that sustain practices through every phase of the cycle.

References

[1] Gross Domestic Product – https://www.bea.gov/data/gdp/gross-domestic-product?utm_source=openai

[2] Pr 26102 Usa Imf Executive Board Concludes 2026 Article Iv Consult – https://www.imf.org/en/news/articles/2026/04/01/pr-26102-usa-imf-executive-board-concludes-2026-article-iv-consult?utm_source=openai

[3] Gdp Q1 Economy Trump – https://www.axios.com/2026/04/30/gdp-q1-economy-trump?utm_source=openai