The property markets across Southern England face unprecedented challenges in 2026, with valuers navigating a complex landscape of structural defects, regulatory changes, and shifting affordability dynamics. While RICS data indicates lagging price recovery in Southern regions compared to national averages, professional surveyors are developing sophisticated valuation techniques for stabilising Southern markets: addressing RAAC, cladding and affordability in 2026 through updated risk assessment models and regional comparable frameworks. 🏘️

The convergence of three critical factors—Reinforced Autoclaved Aerated Concrete (RAAC) concerns, ongoing cladding remediation issues, and evolving affordability metrics—requires valuers to adopt more nuanced approaches than traditional methodologies allow. These challenges demand not just technical expertise but also strategic thinking about how defect risks impact market confidence and property values across Southern England's diverse housing stock.

Key Takeaways

- RAAC identification requires specialist surveys as visual detection is nearly impossible without professional inspection, creating significant valuation uncertainty for properties built between 1955-1995

- Updated defect risk models allow surveyors to apply appropriate adjustments to comparable sales, typically ranging from 15-40% depending on remediation complexity and building type

- Regional comparable analysis must account for local cladding remediation progress and affordability improvements, with Southern markets showing distinct patterns from national trends

- Regulatory reforms including Building Safety Act provisions and EWS1 form evolution directly impact valuation methodologies and lender confidence in 2026

- Affordability metrics are improving in Southern regions despite slower price recovery, creating opportunities for more stable market valuations when properly contextualised

Understanding the RAAC Crisis and Its Impact on Property Valuations

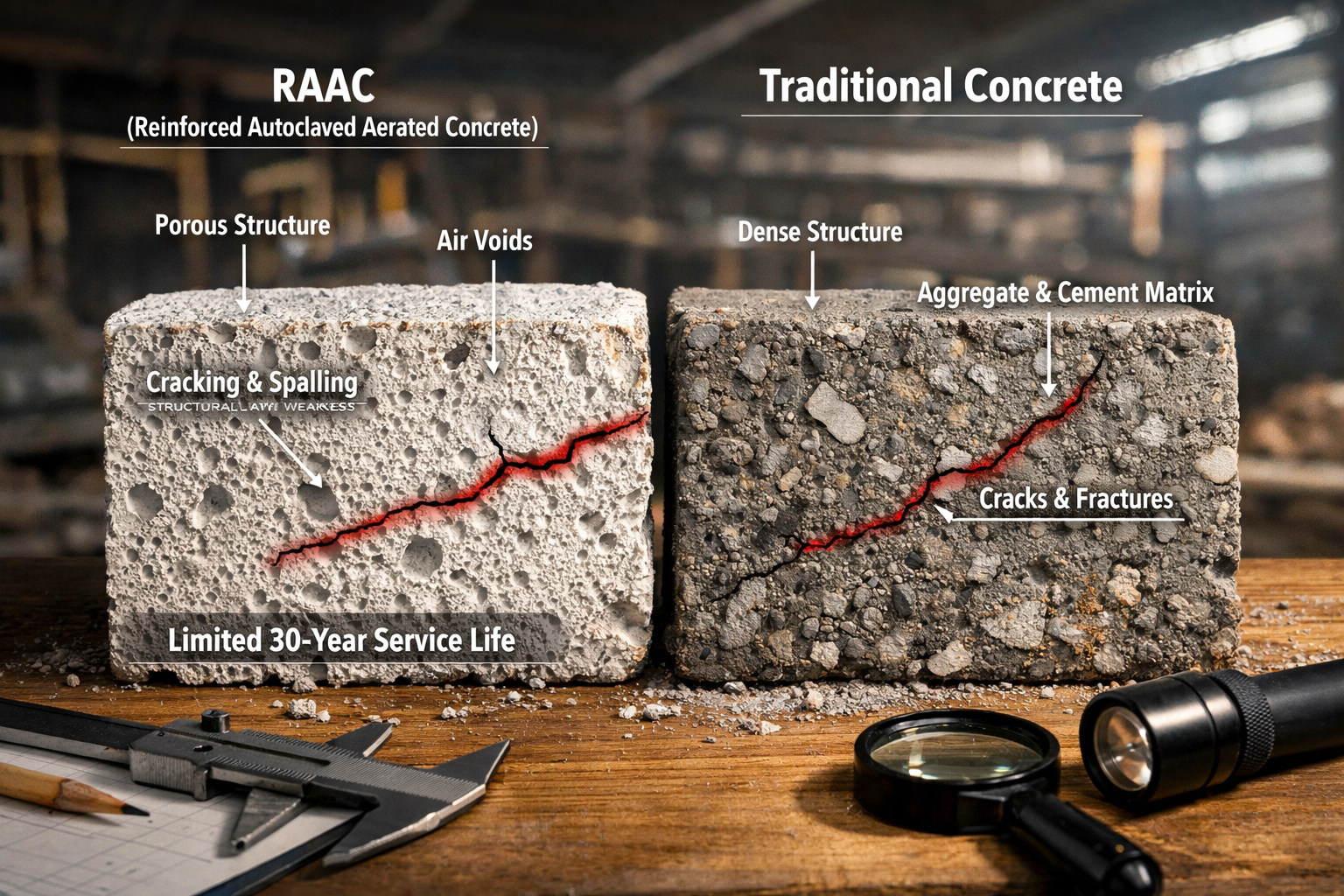

Reinforced Autoclaved Aerated Concrete (RAAC) represents one of the most significant structural challenges facing property valuers in 2026. This lightweight concrete material, extensively used in construction from the mid-1950s through the mid-1990s, has reached or exceeded its typical 30-year service life in the majority of affected buildings. The material's porous nature and reduced durability compared to traditional concrete create serious safety concerns, particularly as RAAC can collapse with little or no warning. 🚨

The Scale and Scope of RAAC Usage

RAAC was predominantly used for:

- Flat roof construction (most common application)

- Load-bearing walls in single and two-storey buildings

- Floor slabs in public sector developments

- External cladding panels

- Internal partition walls

The material's geographic spread extends beyond the UK to Ireland, Australia, New Zealand, Turkey, Japan, and South Africa, but Southern England's substantial public and private housing stock from the 1960s-1980s makes it particularly vulnerable. The challenge for valuers lies in the identification difficulty—without onsite visual inspections and often intrusive surveys, determining RAAC presence is virtually impossible from external examination alone.

Financial Implications for Valuation Adjustments

The cost implications of RAAC remediation provide crucial data points for valuation adjustments. Real-world examples demonstrate the scale:

| Remediation Type | Estimated Cost | Timeframe | Impact on Valuation |

|---|---|---|---|

| Full Demolition | £20-25 million (504 homes) | 4 years | 80-100% reduction |

| Rebuilding | £130 million (504 homes) | 5-15 years | Redevelopment basis |

| Partial Replacement | £40,000-80,000 per unit | 6-18 months | 25-45% reduction |

| Structural Support | £15,000-35,000 per unit | 3-6 months | 15-25% reduction |

These figures, drawn from the Aberdeen housing development case, provide benchmarks for surveyors conducting valuation factor assessments in Southern markets where RAAC presence is confirmed or suspected.

Valuation Methodology Adjustments for RAAC

Professional valuers must integrate RAAC risk into their assessment framework through:

- Enhanced due diligence requirements including construction date verification and building material records review

- Comparable adjustment matrices that account for RAAC status in similar properties

- Risk-weighted valuation ranges rather than single-point valuations

- Lender-specific requirements as mortgage providers increasingly demand RAAC-free certification

For properties requiring specialist defect surveys, the valuation must reflect both the investigation costs and potential remediation expenses. This creates a tiered approach where properties built between 1955-1995 automatically trigger enhanced scrutiny protocols.

Cladding Remediation Progress and Valuation Implications in Southern Markets

The cladding crisis continues to evolve in 2026, with Southern England experiencing varied remediation progress across different local authorities and building types. While the Building Safety Act and various government funding schemes have accelerated remediation work, significant numbers of properties remain affected, creating ongoing valuation challenges for surveyors.

Current State of Cladding Remediation

The landscape in 2026 shows distinct patterns:

Fully Remediated Properties 🟢

- Buildings with completed cladding replacement

- Valid EWS1 forms confirming safety compliance

- Full mortgageability restored

- Valuation adjustments: 0-5% (reflecting market memory)

Active Remediation Projects 🟡

- Works in progress with confirmed funding

- Clear completion timelines (typically 12-24 months)

- Partial mortgageability depending on lender

- Valuation adjustments: 10-20% (reflecting temporary impairment)

Unresolved Cladding Issues 🔴

- No remediation plan or funding secured

- Buildings under 11 metres with uncertain liability

- Ongoing leaseholder disputes

- Valuation adjustments: 30-50% (reflecting significant impairment)

Regional Variations Across Southern England

Southern markets display considerable variation in cladding remediation progress, requiring valuers to maintain detailed knowledge of local authority initiatives and developer remediation programmes. Areas with proactive council engagement and strong developer cooperation show faster recovery in property values compared to regions where remediation remains stalled.

The importance of commercial building surveys extends to mixed-use developments where residential cladding issues affect overall building valuations. Surveyors must assess not just the residential component but how commercial tenants and investors perceive ongoing remediation work.

Valuation Techniques for Cladding-Affected Properties

Comparable Selection Criteria

When valuing cladding-affected properties, surveyors must ensure comparables reflect:

- Similar cladding status (remediated, in-progress, or unresolved)

- Building height categories (under/over 11 metres, over 18 metres)

- Funding arrangements (government-funded, developer-funded, leaseholder liability)

- EWS1 form status and validity dates

Adjustment Methodology

The paired sales analysis technique proves particularly effective for cladding valuations. By comparing identical or near-identical properties within the same development—where some have completed remediation and others haven't—valuers can quantify the specific market impact of cladding status.

"The key to accurate cladding valuations in 2026 lies in understanding not just the physical defect but the funding pathway and timeline certainty. Properties with clear remediation plans trade at significantly lower discounts than those with unresolved liability questions."

Integration with Building Safety Act Requirements

The Building Safety Act's full implementation in 2026 creates additional layers of compliance that affect valuations. Properties must now demonstrate:

- Valid Building Safety Certificates for higher-risk buildings

- Appointed Accountable Persons with clear responsibility chains

- Ongoing safety case documentation

- Resident engagement protocols

These requirements add administrative costs and ongoing compliance burdens that valuers must factor into long-term value assessments, particularly for leasehold properties where service charge implications affect affordability.

Affordability Dynamics and Market Stabilisation Strategies

Affordability improvements across Southern markets in 2026 provide a counterbalance to the negative impacts of RAAC and cladding concerns. While headline prices remain below peak levels in many Southern regions, the combination of wage growth, mortgage rate stabilisation, and increased housing supply creates opportunities for more sustainable valuations based on fundamental affordability metrics rather than speculative pricing.

Measuring Affordability in Southern Markets

Traditional affordability ratios (house price to income multiples) show meaningful improvement across Southern England:

2023 Baseline vs 2026 Comparison

- South East average: 10.2x → 8.9x (13% improvement)

- South West average: 9.8x → 8.4x (14% improvement)

- Greater London periphery: 12.1x → 10.6x (12% improvement)

These improvements stem from multiple factors:

- Nominal wage growth outpacing house price increases

- Mortgage rate stabilisation at 4.5-5.5% (down from 2023 peaks)

- Increased supply particularly in previously constrained local authorities

- First-time buyer schemes improving access for younger purchasers

Valuation Techniques Incorporating Affordability Analysis

Professional valuers in 2026 increasingly integrate affordability metrics into their assessment frameworks, moving beyond simple comparable analysis to consider:

Income-Based Valuation Floors

Establishing minimum sustainable values based on local income distributions and typical mortgage lending criteria. This approach proves particularly valuable for properties affected by RAAC or cladding issues, where comparable evidence may be limited or distorted by defect concerns.

Rental Yield Crosschecks

With rental markets remaining robust across Southern regions, rental yield analysis provides important validation of capital values. Properties showing yields significantly above local norms may indicate undervaluation relative to investment fundamentals, even where defect concerns exist.

Mortgage Availability Weighting

The proportion of properties within a development or area that qualify for standard mortgage lending directly impacts marketability and value. Valuers must assess:

- Percentage of units with RAAC/cladding issues resolved

- Lender appetite for specific building types and heights

- Availability of specialist lending for defect-affected properties

- Impact of Help to Buy and shared ownership schemes

For properties requiring capital gains tax valuations or reinstatement cost assessments, understanding affordability dynamics helps establish realistic disposal scenarios and rebuilding economics.

Regional Comparable Frameworks for Southern Markets

Valuation techniques for stabilising Southern markets: addressing RAAC, cladding and affordability in 2026 require sophisticated comparable frameworks that account for local market conditions. Surveyors must develop databases that track:

Primary Comparable Attributes

- Sale date and completion timeline

- RAAC status (confirmed present/absent/unknown)

- Cladding status and remediation stage

- Building Safety Act compliance level

- EWS1 form status and validity

- Local authority and planning jurisdiction

Secondary Market Factors

- Local wage growth trends

- Transport infrastructure improvements

- Planning policy changes affecting supply

- Demographic shifts and migration patterns

- Employment hub proximity and accessibility

This granular approach allows valuers to identify truly comparable transactions and apply appropriate adjustments for properties affected by structural defects while recognising positive affordability trends.

Strategic Valuation Approaches for Mixed-Condition Portfolios

Large residential developments often contain a mixture of affected and unaffected properties, requiring portfolio-level valuation strategies. Professional surveyors employ:

Stratified Valuation Methodology

Dividing the portfolio into distinct tranches based on defect status and applying different valuation approaches to each:

- Tranche A: Fully remediated/unaffected units (market value basis)

- Tranche B: Active remediation with funding (adjusted market value)

- Tranche C: Unresolved issues (investment/hope value basis)

Phased Remediation Value Modelling

For developments with agreed remediation programmes, valuers can model value recovery trajectories based on completion milestones. This approach proves particularly valuable for collective enfranchisement scenarios where leaseholders seek to acquire freeholds of buildings requiring remediation work.

Lender Requirements and Valuation Reporting Standards

Mortgage lenders in 2026 maintain heightened scrutiny of properties potentially affected by RAAC or cladding issues. Valuation reports must clearly address:

- Explicit RAAC status declaration based on construction date and available records

- Cladding assessment including EWS1 form status where applicable

- Mortgageability statement reflecting current lending criteria

- Retention recommendations where remediation works are planned

- Reinspection requirements for properties undergoing remediation

Valuers must balance professional duty to highlight material risks against the need to provide realistic assessments that support viable transactions. Where uncertainty exists, qualified valuations with appropriate caveats protect both valuer and client while maintaining professional standards.

Regulatory Reform Impacts on Valuation Practice

The regulatory landscape governing property valuation continues to evolve in 2026, with reforms directly affecting how surveyors approach valuation techniques for stabilising Southern markets: addressing RAAC, cladding and affordability in 2026. Understanding these regulatory changes proves essential for accurate and compliant valuation practice.

Building Safety Act Implementation

The Building Safety Act's full implementation creates new compliance requirements that affect property values:

Higher-Risk Buildings (HRBs)

- Buildings over 18 metres or seven storeys with residential units

- Mandatory registration with Building Safety Regulator

- Appointed Accountable Persons with legal responsibilities

- Annual safety case submissions and ongoing monitoring

These requirements add £2,000-5,000 annually to service charges for typical residential units, creating long-term value implications that valuers must factor into assessments. The capitalisation of these additional costs reduces capital values, particularly affecting leasehold valuations where service charge sensitivity runs high.

EWS1 Form Evolution and Alternatives

While the EWS1 form remains relevant in 2026, its application has become more nuanced:

Current EWS1 Requirements

- Mandatory for buildings over 18 metres

- Recommended for 11-18 metre buildings with cladding

- Generally not required for buildings under 11 metres

- Three-year validity period before reassessment needed

Alternative assessment routes now include:

- Building Safety Certificate (for registered HRBs)

- Form EWS1 Plus (enhanced assessment including RAAC screening)

- Lender-specific assessment protocols (varying by institution)

Valuers must understand which assessment route applies to specific properties and how lenders interpret different certification types. Properties with outdated or invalid assessments face significant marketability constraints affecting valuations.

RICS Red Book Updates and Guidance

The RICS Valuation – Global Standards (Red Book) continues to evolve with specific guidance on defect-affected properties. Key requirements for 2026 include:

Enhanced Disclosure Requirements

- Explicit statements on RAAC investigation undertaken

- Cladding assessment methodology and limitations

- Assumptions regarding structural integrity

- Departures from standard valuation approaches

Competence Requirements

- Valuers must demonstrate appropriate expertise for defect-affected properties

- Referral to specialist surveyors where necessary

- Continuing professional development in building pathology

For complex cases involving ATED valuations or non-domicile tax assessments, understanding how defect risks affect market value proves crucial for accurate tax liability calculations.

Practical Implementation: Case Studies from Southern Markets

Real-world applications of valuation techniques for stabilising Southern markets: addressing RAAC, cladding and affordability in 2026 demonstrate how professional surveyors navigate complex scenarios.

Case Study 1: RAAC-Affected Estate in Hampshire

Scenario: 1970s-built estate of 120 properties with confirmed RAAC in roof structures

Valuation Approach:

- Established pre-RAAC discovery baseline using 2022 sales data

- Applied 35% adjustment for confirmed RAAC presence

- Factored in £45,000 per property remediation costs

- Considered council funding package reducing owner liability to £12,000

- Final valuation reflected 18% discount from comparable RAAC-free properties

Outcome: Valuations supported mortgage lending with retention clauses, enabling continued market activity during remediation planning phase.

Case Study 2: Mixed-Status Development in Surrey

Scenario: 200-unit development with 60 properties requiring cladding remediation, 140 already completed

Valuation Approach:

- Stratified portfolio into remediated and pending tranches

- Remediated units: 5% discount reflecting market memory

- Pending units: 15% discount with value recovery trajectory modelled

- Applied affordability analysis showing 12% improvement in local income ratios

- Incorporated 18-month remediation timeline into valuation reporting

Outcome: Enabled portfolio refinancing and supported individual sales in both tranches with appropriate pricing differentiation.

Case Study 3: Affordable Housing Scheme in Sussex

Scenario: Shared ownership development with cladding issues affecting 40 units

Valuation Approach:

- Assessed full market value and shared ownership value separately

- Applied shared ownership valuation principles with cladding adjustments

- Considered housing association remediation obligations

- Evaluated impact on staircasing opportunities for leaseholders

- Factored in Right to Buy implications for qualifying tenants

Outcome: Valuations supported housing association asset management decisions and enabled continued sales of unaffected units.

Technology and Data Analytics in Modern Valuation Practice

Advanced technology increasingly supports valuation techniques for stabilising Southern markets in 2026, providing surveyors with enhanced analytical capabilities.

Automated Valuation Models (AVMs) with Defect Adjustments

Modern AVMs incorporate defect risk factors:

- Construction date screening flagging RAAC-era buildings

- Building height analysis identifying cladding-affected properties

- Remediation status databases tracking completion progress

- Affordability indexing providing real-time ratio updates

While AVMs provide valuable initial assessments, professional surveyors remain essential for complex cases requiring nuanced judgment. Desktop valuations increasingly serve as preliminary screening tools rather than final valuations for defect-affected properties.

Geographic Information Systems (GIS) for Comparable Analysis

GIS technology enables sophisticated comparable selection:

- Heat mapping of RAAC-affected areas

- Remediation progress tracking by local authority

- Transport accessibility analysis affecting affordability

- Planning policy overlay showing development constraints

These tools prove particularly valuable for chartered surveyors operating across South East London and surrounding regions where market conditions vary significantly over short distances.

Building Information Modelling (BIM) Integration

For new-build and recently constructed properties, BIM data provides:

- Complete material specifications eliminating RAAC uncertainty

- As-built documentation supporting accurate assessments

- Maintenance schedules informing long-term value projections

- Energy performance data affecting affordability calculations

Future-Proofing Valuations: Emerging Considerations for 2027 and Beyond

Forward-thinking valuers consider emerging factors that will shape Southern markets beyond 2026:

Climate Resilience and Flood Risk

Increasing importance of environmental factors:

- Flood risk reassessments affecting coastal and riverside properties

- Energy efficiency requirements (EPC ratings) becoming more stringent

- Retrofit costs for older housing stock

- Insurance availability and premium impacts

These factors interact with RAAC and cladding issues, as remediation projects offer opportunities to improve environmental performance simultaneously.

Demographic Shifts and Housing Demand

Changing demand patterns across Southern regions:

- Remote working flexibility affecting location preferences

- Aging population requiring accessible housing

- First-time buyer schemes supporting market entry

- Build-to-rent sector expansion providing alternative tenure

Valuers must consider how these trends affect long-term demand for properties in different conditions and locations.

Regulatory Evolution

Anticipated further regulatory changes:

- Enhanced RAAC disclosure requirements in conveyancing

- Stricter cladding safety standards for lower-rise buildings

- Building Safety Levy impacts on development viability

- Potential reforms to leasehold system affecting service charge liability

Staying ahead of regulatory developments enables valuers to provide forward-looking advice that anticipates market impacts rather than merely reacting to them.

Conclusion

Valuation techniques for stabilising Southern markets: addressing RAAC, cladding and affordability in 2026 require professional surveyors to integrate multiple complex factors into coherent, defensible assessments. While RAAC and cladding issues create significant challenges, improving affordability metrics and regulatory clarity provide counterbalancing positive factors that support market stability.

Key Success Factors for Accurate Valuations

Professional valuers must prioritise:

✅ Comprehensive due diligence including construction date verification and building records review

✅ Sophisticated comparable analysis accounting for defect status, remediation progress, and local market conditions

✅ Clear communication with clients and lenders about assumptions, limitations, and risk factors

✅ Ongoing professional development maintaining expertise in building pathology and regulatory requirements

✅ Technology integration leveraging data analytics while maintaining professional judgment

Actionable Next Steps

For Property Owners:

- Commission specialist surveys if RAAC or cladding concerns exist

- Obtain current EWS1 assessments where applicable

- Engage with remediation programmes proactively

- Maintain comprehensive building documentation

For Purchasers:

- Request detailed valuation reports addressing defect risks explicitly

- Understand mortgage lending criteria for affected properties

- Factor remediation timelines into purchase decisions

- Consider affordability improvements alongside defect concerns

For Professional Valuers:

- Develop robust comparable databases tracking defect status

- Maintain current knowledge of regulatory requirements

- Build relationships with specialist building surveyors

- Invest in technology supporting sophisticated analysis

The Southern property markets of 2026 present unprecedented complexity, but professional surveyors equipped with appropriate valuation techniques can provide the accurate, reliable assessments necessary for market confidence and stability. By acknowledging challenges while recognising positive developments in affordability and regulatory clarity, valuers support informed decision-making across the residential property sector.

The path forward requires continued collaboration between surveyors, lenders, regulators, and property owners to ensure that valuation practice evolves alongside market conditions, maintaining professional standards while supporting sustainable property transactions across Southern England's diverse housing stock. 🏡