Two identical 1930s semi-detached houses sit side by side on the same street in South London. One sells for £625,000. The other — with a clear loft conversion opportunity and room for a rear extension — achieves £672,000. That £47,000 gap is not luck. It is the result of a chartered surveyor systematically quantifying development potential, and in 2026, that process has become more rigorous, more transparent, and more consequential than ever.

Valuing Development Potential: How Surveyors Assess Loft, Extension and Conversion Upside in 2026 UK Appraisals is now a defined discipline within RICS-aligned residential appraisal practice. Surveyors are expected to identify whether loft, side-return, rear extension or garage conversion opportunities exist, assess planning risk, model build costs, and — where the uplift is material — present a separate figure alongside the standard existing use value (EUV). This article explains exactly how that process works, with practical case-style examples for typical UK homes.

Key Takeaways 🏠

- Residual valuation is the primary method surveyors use to quantify loft and extension uplift — GDV minus build costs, fees, finance and profit equals the "development element" of value.

- Permitted development rights (PDR) dramatically affect how much uplift a surveyor will formally reflect in the current market value versus treating it as speculative "hope value."

- A 2–5% change in expected £/sq ft sales rates can materially alter the residual figure — making comparable selection the most critical step in the appraisal.

- Planning risk (conservation areas, Article 4 directions, neighbouring precedent) is stress-tested before any uplift is hard-wired into a valuation report.

- RICS-style development potential sections are now standard in many 2026 residential reports for houses with obvious conversion or extension upside. [5]

The Residual Method: How Surveyors Calculate Loft and Extension Uplift

What Is the Residual Valuation Approach?

At its core, the residual method works backwards from what a finished, improved property would sell for. The formula is straightforward:

Residual Value (Development Uplift) = GDV − Build Costs − Professional Fees − Finance Costs − Developer's Profit

The Gross Development Value (GDV) is derived from recent comparable sales of similar properties that already have the improvement in place — for example, a four-bedroom house with a loft conversion on the same street, sold within the last six to twelve months via HM Land Registry data. [1]

From that GDV, the surveyor deducts:

- 🔨 Build costs — typically benchmarked against BCIS (Building Cost Information Service) rates for the relevant project type

- 📐 Professional fees — architect, structural engineer, planning consultant (usually 8–12% of build cost)

- 💷 Finance costs — relevant where a buyer would need to borrow to fund works

- 📊 Developer's profit — conventionally set at 20% of GDV for residential projects in 2026 [1]

The figure that remains is what can be attributed to the development potential itself — the "uplift" over and above the existing use value.

For a fuller explanation of the methods surveyors use to derive value in different scenarios, see this guide to methods of valuation used in UK appraisals.

Case Example: Loft Conversion Uplift in a South East Suburb

| Item | Figure |

|---|---|

| GDV (comparable 4-bed with loft, same street) | £720,000 |

| Less: Build cost (35m² loft @ £1,800/m²) | −£63,000 |

| Less: Professional fees (10%) | −£6,300 |

| Less: Finance/holding costs | −£4,500 |

| Less: Developer's profit (20% of GDV) | −£144,000 |

| Residual uplift (development element) | £42,200 |

| Existing use value (3-bed, no loft) | £625,000 |

| Indicated value with development potential | £667,200 |

This is not a simple "add the cost of works" calculation. The profit deduction is the element most often misunderstood by homeowners — it reflects the return a rational buyer demands for taking on construction risk and capital outlay. [1]

Why Comparable Selection Is the Most Sensitive Variable

Development value is acutely sensitive to GDV assumptions. A 3% shift in the expected £/sq ft sales rate — easily within the range of normal market variation — can move the residual figure by tens of thousands of pounds on a typical London or South East property. [1]

Surveyors therefore "normalise" comparables carefully, adjusting for:

- Specification (high-spec finishes vs. standard)

- Garden size and orientation

- Parking provision

- Sale date (applying a time adjustment in a 2.4% growth market) [7]

- Exact floor area of the completed improvement

This is why two surveyors looking at the same house can legitimately arrive at different uplift figures — the comparable selection process involves professional judgement, not just data retrieval.

Planning Risk, Permitted Development and Hope Value: The 2026 Framework

The Critical Distinction: Current Market Value vs. Hope Value

One of the most important concepts in valuing development potential in 2026 UK appraisals is the distinction between:

- Current Market Value (CMV) — what the property is worth today, potentially including a modest premium for obvious, low-risk development potential

- Hope Value — the speculative additional value attributable to development potential that has not yet been confirmed by planning permission or permitted development compliance

RICS guidance requires surveyors to be explicit about which basis they are using and why. [5] Where development is clearly achievable under permitted development rights (PDR) — no planning application needed, no Article 4 direction in force — surveyors are more willing to reflect some uplift directly in the CMV. Where planning consent is uncertain, the uplift may appear only as a narrative comment or a separate "subject to planning" scenario. [5]

How Permitted Development Rights Shape Uplift Assessments

The 2025–2026 permitted development framework in England allows a range of enlargements without full planning consent, including:

- Rear extensions up to 6m (semi-detached/terraced) or 8m (detached) under the prior approval neighbour consultation scheme

- Roof enlargements including hip-to-gable conversions and rear dormers on many house types

- Garage conversions to habitable use in most circumstances

Where a proposed loft conversion or rear extension clearly falls within PDR parameters, surveyors treat the planning risk as low and are more confident reflecting uplift in the current market value. [5]

Conversely, in the following scenarios, uplift is treated as more speculative:

| Scenario | Surveyor Treatment |

|---|---|

| Conservation area (no PDR for roof alterations) | Narrative only / discounted hope value |

| Article 4 direction removing PDR | Speculative — planning risk premium applied |

| Listed building | Minimal or no uplift reflected |

| Flood zone / restricted plot | Viability stress-tested heavily |

| Clear PDR compliance, no Article 4 | Uplift reflected in CMV |

Surveyors cross-check local authority planning portals for recent approvals and refusals on comparable schemes in the same street or conservation area before finalising their position. [5] A cluster of recent approvals for rear dormers on the same road is powerful evidence supporting a higher uplift figure.

The Role of the Government's Development Appraisal Framework

The UK Government's Development Appraisal Tool — most recently revised in 2024 and still the reference standard in 2026 — models increased floorspace as a marginal uplift in GDV against marginal costs. [6] Surveyors apply the same logic at micro-scale: a loft adding 25–40 m² or a rear extension adding 15–25 m² is treated as a marginal GDV increment, with the associated marginal build cost and profit deducted to derive the residual. [6]

This framework also informs how surveyors handle Section 106 and Community Infrastructure Levy (CIL) exposure on larger projects — relevant where a garage conversion creates a new dwelling unit rather than simply extending an existing one, triggering planning obligations that must be deducted from the residual. [6]

For properties where development potential intersects with leasehold complications — for example, a maisonette where the freeholder's consent is needed before any structural alteration — the valuation becomes considerably more complex. A lease extension valuation may need to be considered alongside the development appraisal.

Practical Application: How Surveyors Structure 2026 Valuation Reports With Development Upside

What a 2026 RICS-Aligned Development Potential Section Looks Like

RICS-style development potential sections are now standard in many 2026 residential valuation reports where loft, extension or conversion upside is material. [5] A well-structured report will typically contain:

- Existing Use Value (EUV) — the property valued as it stands, with no development assumed

- Development Scenario Description — what the surveyor believes is achievable (e.g., "rear dormer loft conversion providing one additional bedroom and en-suite bathroom, estimated 32m² net additional floor area")

- Residual Appraisal Summary — GDV, cost deductions, profit assumption and residual uplift figure

- Planning Risk Assessment — PDR compliance check, Article 4 status, conservation area designation, recent local precedent

- Value Conclusion — either an uplifted CMV (where risk is low) or a separate "with development" scenario figure (where risk is higher)

The surveyor's professional judgement determines whether the uplift is "hard-wired" into the headline value or presented as a conditional scenario. [5]

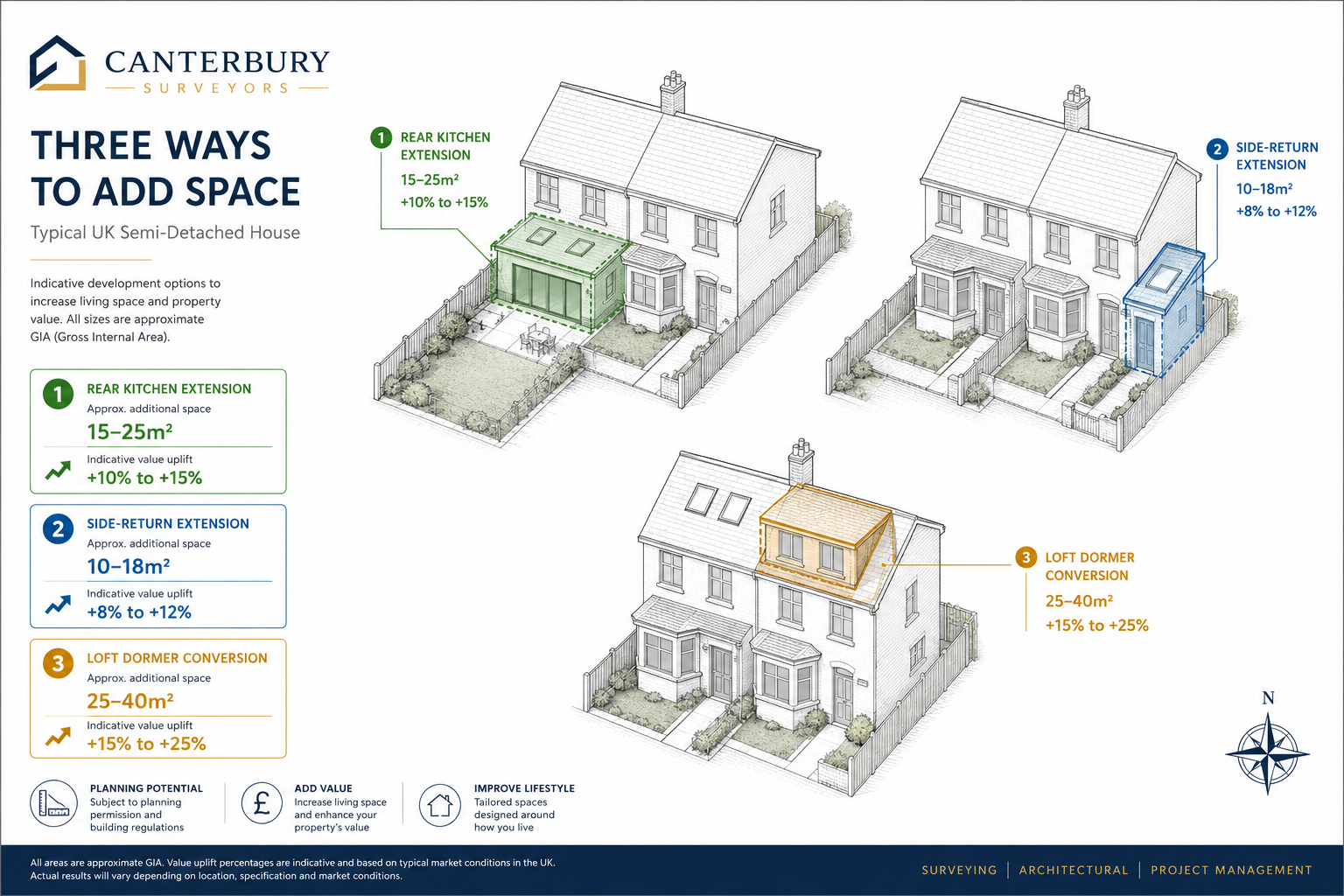

Three Case-Style Examples for Typical UK Houses

🏠 Case 1: 1930s Semi in Outer London (PDR-Compliant Loft)

A three-bedroom semi in Harrow has a hip roof suitable for hip-to-gable conversion with rear dormer. The scheme falls within PDR parameters. Comparable four-bedroom conversions nearby have sold at £680,000–£695,000. Residual analysis produces an uplift of approximately £38,000–£44,000. The surveyor reflects a mid-point uplift of £41,000 in the current market value, noting low planning risk. Chartered surveyors in Harrow regularly encounter this scenario.

🏠 Case 2: Victorian Terrace in a Conservation Area (Hope Value Only)

A two-bedroom Victorian terrace in Islington sits within a conservation area where Article 4 removes PDR for roof alterations. A rear extension is feasible under a planning application, but the loft conversion requires full consent with uncertain outcome. The surveyor values the property at EUV and adds a narrative comment noting "material hope value subject to securing planning consent, estimated at £30,000–£55,000 if consent obtained." No uplift is reflected in the headline figure. For properties in areas like this, working with chartered surveyors in Islington who know the local planning environment is essential.

🏠 Case 3: Detached House in Surrey with Rear Extension and Garage Conversion Potential

A four-bedroom detached house in Surrey has a large rear garden and an integral garage. A rear extension of 22m² and garage conversion to home office are both PDR-compliant. Comparable improved properties indicate a combined GDV uplift of £85,000. After deducting build costs (£52,000), fees (£5,200), finance (£3,800) and profit (£17,000), the residual development element is approximately £7,000 — a modest figure that reflects the high build costs relative to the marginal GDV gain. The surveyor reflects a conservative £5,000–£8,000 uplift in CMV.

💡 Pull Quote: "The profit deduction is the element most often misunderstood by homeowners. It is not the surveyor being conservative — it is the market pricing in the risk and capital cost of actually doing the work."

Choosing the Right Survey Type to Capture Development Value

Not every survey type will address development potential in the same depth. A Level 2 HomeBuyer Report will note obvious opportunities but is unlikely to include a full residual appraisal. A RICS Building Survey (Level 3) or a bespoke valuation report is the appropriate vehicle for a detailed development potential assessment.

For buyers specifically interested in quantifying loft or extension upside before making an offer, commissioning a standalone valuation report with a development potential section is often the most cost-effective approach.

It is also worth noting that any planned structural works — particularly loft conversions involving removal of purlins or chimney breasts — will require a structural survey to confirm feasibility and identify any hidden costs that could erode the residual uplift figure.

Party Wall Considerations and Their Effect on Residual Value

One cost item frequently underestimated in amateur residual calculations is the party wall process. Rear extensions and loft conversions on terraced or semi-detached properties almost always trigger the Party Wall etc. Act 1996. Surveyor fees, potential awards and neighbour compensation can add £2,000–£8,000+ to project costs — directly reducing the residual uplift. Understanding party wall obligations before finalising a development potential figure is therefore an essential step, not an afterthought.

Conclusion: Actionable Steps for Buyers, Sellers and Investors in 2026

Valuing Development Potential: How Surveyors Assess Loft, Extension and Conversion Upside in 2026 UK Appraisals is no longer a niche speciality — it is a mainstream component of residential property appraisal in the UK, particularly in London and the South East where space is scarce and marginal floorspace commands a premium.

Actionable Next Steps ✅

-

Commission the right survey. If development potential is a key part of a purchase decision, request a Level 3 Building Survey or a bespoke valuation report with an explicit development potential section — not a basic mortgage valuation.

-

Check PDR status before assuming uplift. Verify whether the property sits in a conservation area or Article 4 direction zone. This single factor determines whether uplift is hard-wired into value or treated as speculative hope value.

-

Build a realistic residual model. Use BCIS build cost benchmarks, local HM Land Registry comparables from the last six months, and a 20% profit on GDV assumption. Do not rely on estate agent "after-improvement value" estimates without normalising for specification and sale date.

-

Factor in the full cost stack. Party wall fees, structural engineer costs, planning fees and CIL/S106 obligations must all be deducted before arriving at a credible residual figure.

-

Engage a local chartered surveyor. Development potential is highly location-specific. A surveyor with deep knowledge of local planning history, comparable sales and design guidance will produce a more reliable uplift figure than a national generalist.

The difference between a property that achieves full development value and one that leaves money on the table often comes down to the quality of the appraisal — and in 2026, the tools, data and RICS frameworks to get that right have never been more accessible.

References

[1] How To Value Land – https://www.domusgroups.com/blog/how-to-value-land

[2] Overcoming The Challenges Of Development Appraisals – https://ajasurveyors.co.uk/overcoming-the-challenges-of-development-appraisals/

[3] Development Appraisal And Viability – https://www.carterjonas.co.uk/services/development-appraisal-and-viability

[5] Valuation Surveys For Properties With Development Potential RICS Appraisals Maximising Uplift In 2026 Planning Reforms – https://www.canterburysurveyors.com/blog/valuation-surveys-for-properties-with-development-potential-rics-appraisals-maximising-uplift-in-2026-planning-reforms/

[6] Development Appraisal Tool User Manual Accessible Version – https://www.gov.uk/government/publications/development-appraisal-tool/development-appraisal-tool-user-manual-accessible-version

[7] Valuation Precision For 2026 House Price Adjustments Tools For Surveyors In A 2.4% Growth Market – https://wimbledonsurveyors.com/valuation-precision-for-2026-house-price-adjustments-tools-for-surveyors-in-a-2-4-growth-market/

[8] Development Valuation – https://www.fishergerman.co.uk/insights/publications/development-valuation