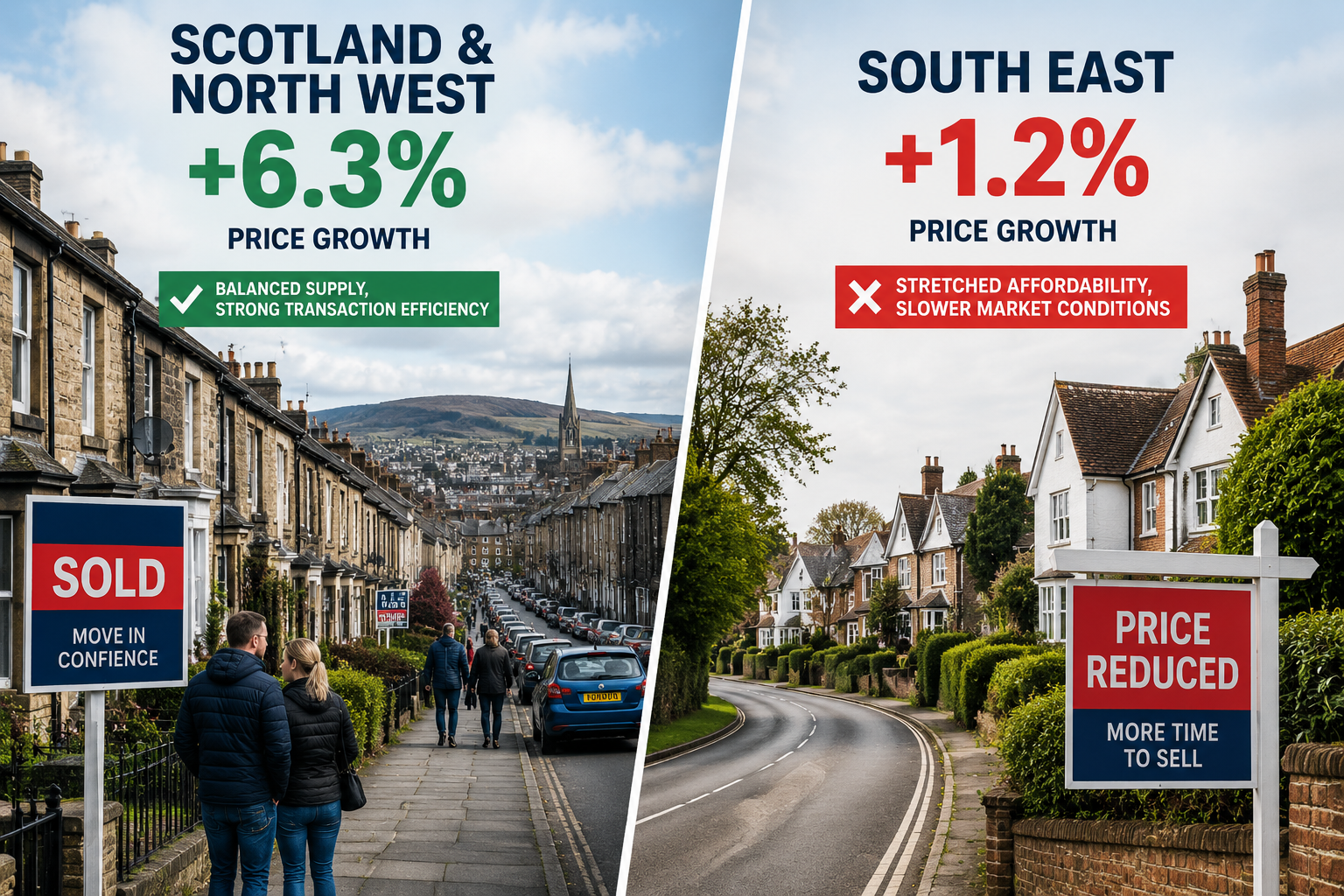

Scotland and Northern England are forecast to outperform the rest of the UK property market in 2026 by a margin that is impossible for any serious building surveyor to ignore. Zoopla's analysis of 120 UK postal areas places Glasgow, Edinburgh, Motherwell, Paisley, and Wigan among the strongest performers — with annual price growth projected between 2% and over 4% — while London and South East locations languish near the bottom of the same rankings [1]. This is not a minor statistical blip. It is a structural realignment of the UK housing market, and valuation divergence between regions: how building surveyors adapt to Scotland, North West, and South East price variations in 2026 has become one of the most pressing professional challenges in the surveying sector.

For clients buying, selling, or remortgaging across different regions, the implications are significant. A surveyor applying a single national lens risks producing valuations that are either dangerously conservative in high-growth northern markets or recklessly optimistic in stretched southern ones.

Key Takeaways 📌

- Scotland and the North West are leading UK house price growth in 2026, driven by affordability, balanced supply, and efficient transaction speeds [1].

- South East markets show restrained conditions overall, though pockets like Medway and Dover are delivering ~3% growth [3].

- Structural affordability gaps — not short-term sentiment — are the primary driver of regional price divergence [1].

- Building surveyors must apply region-specific comparables, local economic intelligence, and tailored client communication to remain accurate and credible.

- Understanding valuation factors and regional market dynamics is now a core professional competency, not an optional extra.

Why Regional Price Divergence Has Accelerated in 2026

The Affordability Engine Driving Northern Growth

The single most important factor behind regional divergence in 2026 is affordability. Average property values in Scottish cities and northern English towns remain considerably below those in London and the South East — a gap that has become increasingly decisive in a market shaped by elevated borrowing costs [1].

In practical terms, a buyer in Glasgow or Wigan can access a family home at a price-to-income ratio that remains broadly manageable. In Surrey or central London, that same ratio has stretched to a point where demand is structurally suppressed. Higher mortgage rates have not hit all markets equally — they have acted as a regional filter, accelerating growth where prices are realistic and cooling markets where they are not.

💬 "Geographical divergence is now the defining characteristic of the UK housing market — areas where pricing aligns with local incomes are positioned to lead growth." [1]

Supply Dynamics: Balanced in the North, Strained in the South

The UK entered 2026 with the highest level of homes for sale in over eight years, with the average agent marketing 32 properties across the national market [3]. But this headline figure masks a sharp regional split:

| Region | Unsold Stock (>6 months) | Price Reductions | Transaction Speed |

|---|---|---|---|

| Scotland | Low | Rare | Fast |

| North West | Low-Moderate | Uncommon | Efficient |

| South East | Elevated | Common | Slower |

| London | High | Frequent | Slowest |

In Scotland and the North West, the proportion of homes sitting unsold for more than six months remains modest, and widespread discounting is far less common than in southern markets [1]. Homes are transacting efficiently — a signal of balanced conditions rather than overheating [1].

The Rental Market Adds Another Layer 🏘️

Rents across the UK remain 2.4% higher year-on-year as of early 2026, despite recent short-term softening [3]. Average rents fell 1.1% in January 2026 to £1,302 — the third consecutive monthly decline — in line with typical seasonal patterns. Notably, the North West and South East both avoided these seasonal falls [3], which has implications for surveyors working on buy-to-let valuations and investment appraisals in those regions.

How Building Surveyors Adapt to Scotland, North West, and South East Price Variations in 2026

Understanding the valuation divergence between regions: how building surveyors adapt to Scotland, North West, and South East price variations in 2026 requires more than awareness of headline statistics. It demands a systematic change in methodology, comparable selection, and client communication.

1. Region-Specific Comparable Evidence

The foundation of any credible valuation is comparable evidence. In a diverging market, surveyors must:

- Tighten the geographic radius of comparables — a 5-mile radius that works in a homogenous suburban market may span three entirely different micro-markets in Scotland or the North West.

- Weight recent transactions more heavily in fast-moving northern markets, where six-month-old sales data may already understate current values.

- Apply downward adjustments cautiously in the South East, where price reductions are common but do not always reflect the true market value of well-presented, well-located stock.

For surveyors operating across chartered surveyor services in Surrey or Hampshire, the challenge is distinguishing between genuine market softening and temporary oversupply in specific price bands.

2. Understanding Local Economic Drivers

Regional price variation does not exist in a vacuum. Surveyors must engage with local economic intelligence:

Scotland 🏴

- Strong demand in Glasgow, Edinburgh, and smaller cities like Perth and Inverness [1]

- However, a notable economic divergence exists between Scotland's north east and the rest of the UK, with businesses in that sub-region facing more challenging conditions than their counterparts elsewhere [2]

- Surveyors must distinguish between the buoyant central belt market and more nuanced conditions in Aberdeen and the north east

North West 🏙️

- Wigan, Manchester commuter belt, and surrounding areas benefit from infrastructure investment and relative affordability

- Employment growth in professional services and logistics supports sustained demand

- Rental market resilience (avoiding January 2026's seasonal decline) signals strong underlying occupier demand [3]

South East 🏡

- Overall performance restrained, with average values up just 1% year-on-year in measured areas [3]

- Pockets of outperformance exist: Medway and Dover recorded approximately 3% growth during the assessed period [3]

- Surveyors must avoid treating the South East as a monolith — coastal and commuter markets are diverging from prime Home Counties locations

3. Survey Type Selection and Regional Risk Profiles

Regional price divergence also affects which survey product is most appropriate for a given property. In high-growth northern markets where older housing stock is common — Victorian terraces, tenements, stone-built properties — a comprehensive RICS Level 3 Building Survey is frequently the most appropriate choice. The risk of undisclosed structural issues is higher in older stock, and the cost of getting it wrong in a fast-moving market is significant.

In the South East, where newer-build properties are more prevalent and transactions are slower, a RICS Level 2 Home Survey may suffice for standard residential purchases — but surveyors should always help clients choose the right property survey based on property age, condition, and the specific risks of the local market.

4. Communicating Uncertainty to Clients

One of the most underappreciated skills in a diverging market is client communication. Surveyors must:

- Clearly explain why a valuation in Glasgow may reflect strong upward pressure, while a comparable property in Guildford may be subject to downward revision risk

- Avoid false precision — in volatile or transitional markets, a valuation range is often more honest than a single figure

- Reference the price of valuation services transparently, helping clients understand that regional complexity justifies thorough professional assessment

💬 "A surveyor who cannot explain why two superficially similar properties in different regions carry different risk profiles is not serving their client well."

Regional Valuation in Practice: Tactical Adjustments for 2026

Scotland: Capitalising on Growth While Managing Sub-Regional Risk

Scottish valuations in 2026 require surveyors to hold two realities simultaneously. The central belt — Glasgow, Edinburgh, Falkirk, Kirkcaldy — is genuinely strong, with demand consistent, supply controlled, and prices aligned with local incomes [1]. Surveyors working in these markets should:

✅ Use tight, recent comparables (within 3 months where possible)

✅ Scrutinise tenement and stone-built properties for damp, structural movement, and shared maintenance obligations

✅ Factor in the Scottish legal system's distinct conveyancing process, which affects transaction timelines and valuation certainty windows

In Scotland's north east, however, the picture is more complex. An economic divergence between this sub-region and the rest of the UK has prompted calls for targeted government intervention [2]. Surveyors here should apply more conservative assumptions and engage closely with local agents on current achievable prices.

North West: Efficiency and Opportunity

The North West represents perhaps the clearest opportunity for surveyors to add value in 2026. Balanced supply, efficient transactions, and sustained rental demand [1][3] create conditions where accurate, well-evidenced valuations can support confident client decision-making.

Key tactical considerations:

- Leasehold properties are prevalent in Manchester and Liverpool — surveyors should factor in lease length, ground rent, and service charge implications. Understanding leasehold valuation complexities is essential in this market.

- Shared ownership is increasingly common in affordable North West developments — a specialist area requiring careful shared ownership property valuation methodology.

- Older industrial-era housing stock carries specific risks around damp, drainage, and structural integrity that warrant thorough inspection.

South East: Precision in a Cautious Market

The South East demands precision rather than pessimism. While overall performance is restrained — up just 1% year-on-year on average [3] — the region is not uniform:

| Sub-Market | 2026 Outlook | Surveyor Priority |

|---|---|---|

| Medway & Dover | ~3% growth [3] | Strong comparable evidence, upward pressure |

| Prime Home Counties | Flat to -1% | Careful downward adjustment methodology |

| London commuter belt | Mixed | Transport link premium analysis |

| Coastal South East | Selective growth | Lifestyle premium vs. flood/coastal risk |

Surveyors covering South East London and surrounding areas must be especially rigorous in distinguishing between properties that retain strong fundamentals and those where vendor expectations have not yet adjusted to market reality.

For commercial property work in the South East, RICS commercial building surveys remain essential tools for investors navigating a more cautious occupier market.

The Broader Professional Implications

Continuing Professional Development (CPD) in a Diverging Market

RICS members operating across multiple regions in 2026 face a genuine CPD imperative. Regional market literacy — understanding the specific drivers, risks, and comparable frameworks for each area — is no longer a specialist skill. It is a baseline requirement.

Surveyors should:

- 📚 Engage regularly with regional market reports from Zoopla, Rightmove, and local agents

- 🤝 Build relationships with regional estate agents to access real-time transaction intelligence

- 🔍 Review valuation methods regularly to ensure approaches remain appropriate for specific regional conditions

- 📊 Document regional adjustment rationale clearly in all valuation reports to withstand challenge

Technology and Data as Regional Equalizers

Advanced automated valuation models (AVMs) are increasingly used as starting points for residential valuations. However, in a market defined by regional divergence, AVMs trained primarily on southern data will systematically undervalue northern and Scottish properties. Professional surveyors add irreplaceable value by applying local judgment that no algorithm can replicate.

Conclusion: Actionable Next Steps for Surveyors and Clients

The valuation divergence between regions: how building surveyors adapt to Scotland, North West, and South East price variations in 2026 is not a temporary disruption — it reflects deep structural differences in affordability, supply, and economic momentum that are likely to persist for several years [1].

For building surveyors, the priority actions are clear:

- Recalibrate comparable selection for each region — tighter geography, more recent evidence in fast markets, careful adjustment in slow ones.

- Develop sub-regional expertise — Scotland's central belt and north east require different approaches; the South East is not one market.

- Communicate regional complexity to clients clearly and confidently, helping them understand why regional context shapes every valuation decision.

- Stay current on rental market trends, supply data, and local economic conditions — the 2026 market rewards surveyors who treat regional intelligence as a core professional asset.

For property buyers and owners, the message is equally direct: do not assume a national average tells you anything useful about your specific transaction. Commission a surveyor with genuine regional expertise, ensure the survey level matches the property and market, and treat professional valuation as an investment in decision-making certainty — not a box-ticking exercise.

The UK property market in 2026 rewards regional precision. Surveyors who deliver it will define the standard of the profession.

References

[1] Why Northern England And Scotland Are Set To Lead UK House Price Growth In 2026 – https://www.belvoir.co.uk/guides/news/why-northern-england-and-scotland-are-set-to-lead-uk-house-price-growth-in-2026/

[2] Survey Shows Unfavourable Divergence Between North East Firms And Rest Of UK – https://news.stv.tv/north/survey-shows-unfavourable-divergence-between-north-east-firms-and-rest-of-uk

[3] Article – https://www.stevensestateagents.com/blog/article.html?id=1772635874