The UK property market in 2026 presents a complex landscape of regional disparities that challenge traditional valuation approaches. As the market recovers from previous economic pressures, Valuation Challenges in a Recovering UK Market: North-South Price Divergence and RICS Adjustment Strategies for 2026 have become critical concerns for chartered surveyors, lenders, and property professionals. While overall UK house prices are projected to grow by 2-4% this year[1][2], this headline figure masks a dramatic north-south divide that requires sophisticated valuation methodologies and careful market analysis.

The stark reality facing valuers today is that London—traditionally the powerhouse of UK property values—remains the only major region experiencing price stagnation or decline, while northern markets demonstrate robust growth[1]. This geographical split creates unprecedented challenges for registered RICS valuers attempting to provide accurate, defensible valuations across different regional markets.

Key Takeaways

- 📊 Regional divergence is the defining characteristic of 2026's UK property market, with northern England outperforming southern regions significantly

- 🏘️ London properties are taking substantially longer to sell and experiencing price stagnation, while the North West shows consistent growth

- 💷 Premium property valuations face severe challenges, with 83% of offers on £2 million+ homes coming below asking price in early 2026[3]

- 📋 RICS Red Book methodologies require careful adjustment for regional market conditions and comparable evidence selection

- 🎯 Seller overoptimism combined with mortgage rate volatility creates significant valuation friction points across all market segments

Understanding the North-South Price Divergence in 2026

The Scale of Regional Disparities

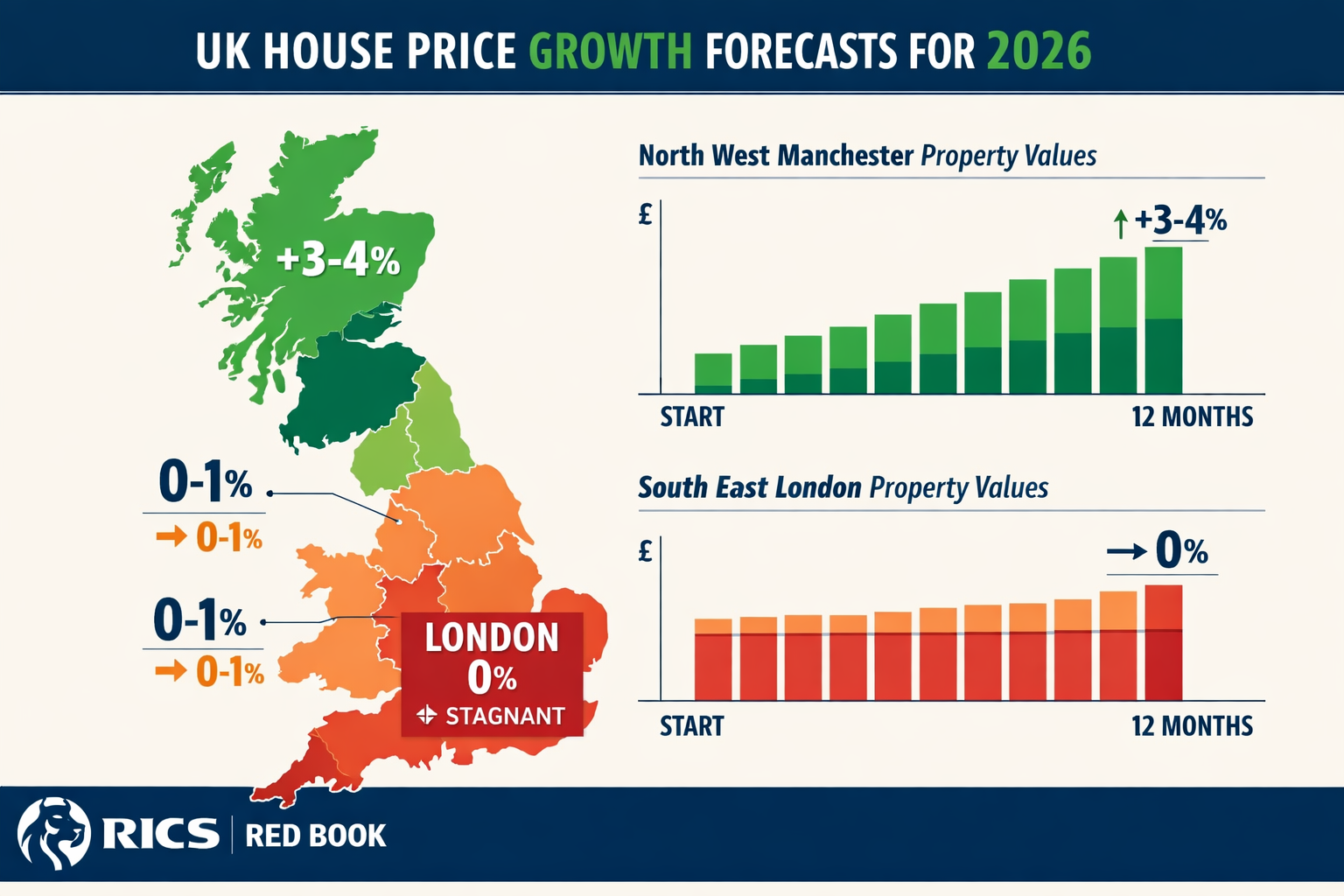

The Valuation Challenges in a Recovering UK Market: North-South Price Divergence and RICS Adjustment Strategies for 2026 begin with understanding the fundamental shift in regional performance. According to market forecasts, the north-south divide that emerged in previous years has not only persisted but intensified throughout 2026[2].

Key regional performance indicators include:

| Region | Projected Growth 2026 | Market Characteristics |

|---|---|---|

| North West England | 3-4% | Strong buyer demand, affordability advantage |

| Yorkshire | 3-4% | First-time buyer activity, wage growth support |

| London | 0-1% (stagnation) | Extended selling times, buyer caution |

| South East | 1-2% | Mixed performance, commuter belt variation |

| National Average | 2-4% | Moderate recovery trajectory |

This divergence creates immediate challenges for valuers working across multiple regions. A valuation methodology that accurately reflects Manchester market conditions may significantly overvalue comparable properties in central London.

London's Unique Market Stagnation

London's position as the only major UK region experiencing price decline or stagnation represents a fundamental shift in market dynamics[1]. Properties in the capital are taking significantly longer to sell compared to the rest of the UK, creating a buyer's market that contrasts sharply with the seller-favorable conditions in northern cities.

Several factors contribute to London's underperformance:

- Affordability ceiling – London prices reached levels that exceed sustainable income multiples

- Stamp duty burden – Higher transaction costs disproportionately affect London buyers

- Remote work flexibility – Reduced need for London proximity has dampened demand

- International buyer caution – Geopolitical uncertainty has reduced overseas investment

For chartered surveyors in South East London and surrounding areas, these conditions require careful consideration when selecting comparable evidence and applying market adjustments.

Northern Market Resilience and Growth Drivers

In contrast to southern stagnation, northern England demonstrates remarkable resilience. The affordability advantage in regions like the North West has attracted first-time buyers and investors seeking better value propositions. Steady wage growth in these areas supports mortgage affordability, creating sustainable demand rather than speculative bubbles.

"The current north-south divide in house price growth is expected to persist in 2026, with higher growth projected in northern England than in the south, reflecting stronger buyer demand and affordability advantages in northern regions."[2]

This sustained growth creates different valuation challenges. Valuers must distinguish between genuine market appreciation driven by fundamentals versus short-term momentum that may not be sustainable. The risk of overvaluation exists when comparable evidence from rapidly rising markets is applied without proper temporal adjustments.

RICS Red Book Valuation Strategies for Divergent Markets

Adapting Comparable Evidence Selection

Valuation Challenges in a Recovering UK Market: North-South Price Divergence and RICS Adjustment Strategies for 2026 require rigorous application of RICS Red Book principles with heightened attention to regional context. The selection of comparable evidence becomes more complex when regional markets move in opposite directions.

Best practices for comparable selection in 2026 include:

✅ Temporal relevance – Prioritize transactions from the past 3-6 months over older comparables due to rapid market shifts

✅ Geographic precision – Narrow the search radius in volatile markets; a 1-mile difference can represent distinct market conditions

✅ Transaction type verification – Distinguish between genuine arm's length transactions and distressed sales or family transfers

✅ Market condition adjustments – Apply explicit adjustments for changing market conditions between comparable sale date and valuation date

✅ Multiple data sources – Cross-reference Land Registry data with local agent intelligence and auction results

For valuation professionals working across regions, maintaining separate databases of comparables for northern and southern markets prevents inappropriate cross-regional application of evidence.

Addressing Seller Overoptimism and Market Friction

One of the most significant valuation challenges in 2026 is the persistent gap between seller expectations and market reality. Property market experts have identified seller and estate agent overoptimism as a key friction point, causing properties to sit unsold for extended periods[4].

This creates a dual challenge for valuers:

- Instructing clients often reference asking prices rather than achieved prices when forming value expectations

- Comparable evidence becomes distorted when overpriced properties dominate available listings

The solution requires transparent communication about the distinction between asking prices (seller aspirations) and achieved prices (market reality). RICS valuers must clearly document this distinction in valuation reports and provide robust evidence supporting their conclusions.

Case Study: North West Manchester Market

A terraced property in a desirable Manchester suburb illustrates the northern growth dynamic. In January 2025, similar properties sold for £285,000. By March 2026, comparable sales achieved £298,000—a 4.6% increase. However, current listings show asking prices of £315,000-£325,000.

A RICS-compliant valuation would:

- Weight recent achieved sales most heavily (£298,000)

- Apply modest positive adjustment for continued market momentum (+1-2%)

- Arrive at market value of approximately £301,000-£305,000

- Clearly distinguish this from inflated asking prices

Premium Property Valuation Adjustments

The high-value property segment faces particularly acute challenges. Data from February 2026 reveals that 83% of offers on homes priced within 10% of £2 million came in below the threshold—a dramatic increase from 64% just one year earlier[3]. This represents a severe valuation misalignment in the premium segment.

For valuers conducting probate valuations or capital gains tax valuations on high-value properties, this trend demands conservative approaches:

🔍 Enhanced due diligence – Verify all comparable transactions with completion statements where possible

🔍 Downward adjustments – Apply negative market condition adjustments for properties above £1.5 million in southern markets

🔍 Extended marketing period assumptions – Factor longer selling times into valuation advice for clients

🔍 Stamp duty impact analysis – Explicitly consider transaction cost burden at different price points

The £2 million threshold has become particularly sensitive due to stamp duty implications, creating artificial price clustering just below this level. Valuers must recognize this behavioral economics factor when analyzing comparable evidence.

Implementing RICS Adjustment Strategies Across Regional Markets

Quantifying Market Condition Adjustments

Valuation Challenges in a Recovering UK Market: North-South Price Divergence and RICS Adjustment Strategies for 2026 require explicit quantification of market condition adjustments. Unlike stable markets where time adjustments might be minimal, 2026's divergent regional performance demands careful calculation.

Framework for market condition adjustments:

Step 1: Establish Regional Trend

- Analyze 12-month price index movement for specific locality

- Distinguish between median and mean price changes

- Identify seasonal patterns specific to the region

Step 2: Calculate Monthly Adjustment Rate

- Northern growth markets: typically +0.25% to +0.35% per month

- London/stagnant markets: 0% to -0.15% per month

- Apply to time gap between comparable sale and valuation date

Step 3: Document Adjustment Rationale

- Provide transparent calculation methodology

- Reference specific market data sources

- Explain any departure from mechanical application

For example, a comparable sale in North London from six months ago at £650,000 in a stagnant micro-market might warrant a -1% adjustment (6 months × -0.15%), suggesting current market value of approximately £643,500 before other adjustments.

Integrating Mortgage Market Volatility

The early March 2026 mortgage rate increases driven by Middle East geopolitical volatility add another layer of complexity[4]. HSBC UK, Nationwide, and Coventry Building Society all raised rates, potentially dampening the affordability gains that were supporting market recovery.

Valuers must consider how changing mortgage affordability affects different market segments:

| Property Price Band | Mortgage Rate Sensitivity | Valuation Impact |

|---|---|---|

| £150,000-£300,000 | High – First-time buyers rate-dependent | Moderate negative adjustment warranted |

| £300,000-£600,000 | Medium – Mix of movers and equity buyers | Monitor closely, minimal current adjustment |

| £600,000-£1.5M | Low-Medium – Higher equity ratios | Limited direct impact |

| £1.5M+ | Low – Cash buyers prevalent | Minimal rate sensitivity |

This tiered approach recognizes that valuation factors vary significantly across price bands. The same 0.25% mortgage rate increase that substantially impacts first-time buyer affordability has minimal effect on premium property purchasers.

Case Study: Contrasting London and North West Valuations

London Case Study: £1.8M Property in South West London

A Victorian semi-detached house in South West London requires valuation for refinancing purposes. Comparable evidence shows:

- Comparable 1: Sold 4 months ago for £1,850,000

- Comparable 2: Sold 7 months ago for £1,920,000

- Comparable 3: Currently listed at £1,950,000 (6 months on market)

RICS-compliant valuation approach:

- Disregard Comparable 3 (asking price, not achieved sale)

- Apply negative time adjustment to Comparable 2: £1,920,000 × (1 – 0.01) = £1,900,800

- Weight recent Comparable 1 most heavily

- Consider market stagnation and extended selling periods

- Concluded value: £1,825,000 (conservative within range)

North West Case Study: £425,000 Property in Manchester Suburb

A modern detached property requires Help to Buy valuation in a growing Manchester suburb. Comparable evidence shows:

- Comparable 1: Sold 2 months ago for £418,000

- Comparable 2: Sold 5 months ago for £405,000

- Comparable 3: Sold 8 months ago for £398,000

RICS-compliant valuation approach:

- Apply positive time adjustments reflecting 3-4% annual growth

- Comparable 2 adjusted: £405,000 × (1 + 0.0125) = £410,063

- Comparable 3 adjusted: £398,000 × (1 + 0.025) = £407,950

- Weight recent Comparable 1 most heavily

- Concluded value: £422,000 (reflecting growth trajectory)

These contrasting examples demonstrate how identical RICS methodologies produce different adjustment patterns based on regional market dynamics.

Leveraging Technology and Data Analytics

Modern valuation practice increasingly incorporates technology-enhanced analysis to address regional divergence challenges. Advanced tools available to RICS valuers in 2026 include:

📱 Automated Valuation Models (AVMs) – Useful for initial range estimation but requiring professional override in volatile markets

📱 Geospatial analysis tools – Mapping price gradients across micro-markets to identify localized trends

📱 Transaction database platforms – Real-time access to Land Registry data with filtering capabilities

📱 Market sentiment indicators – Tracking viewing-to-offer ratios and time-on-market metrics

However, technology serves as a supplement rather than substitute for professional judgment. The nuanced understanding required for desktop house valuations and site inspections cannot be fully automated, particularly in divergent markets where local knowledge becomes paramount.

Strategic Recommendations for Valuation Professionals

Building Regional Market Intelligence

To effectively navigate Valuation Challenges in a Recovering UK Market: North-South Price Divergence and RICS Adjustment Strategies for 2026, valuers must develop deep regional expertise rather than relying on national trends.

Recommended intelligence-gathering practices:

🎯 Establish agent networks – Regular dialogue with local estate agents provides early indicators of market shifts

🎯 Monitor auction results – Auction sales provide transparent market evidence less subject to negotiation distortion

🎯 Track planning applications – Understanding development pipeline helps anticipate supply-side changes

🎯 Attend local property events – Networking builds knowledge of micro-market nuances

🎯 Subscribe to regional indices – Track Rightmove, Zoopla, and Land Registry data at postcode level

For practices serving multiple regions, consider designating regional specialists who develop concentrated expertise in specific markets rather than spreading resources thinly across all areas.

Enhancing Client Communication

The gap between client expectations and market reality requires enhanced communication strategies. When instructing clients reference inflated asking prices or outdated comparable evidence, valuers must provide education alongside valuation.

Effective communication techniques include:

✍️ Visual market analysis – Charts showing regional price trends make abstract concepts concrete

✍️ Comparable evidence tables – Transparent presentation of all comparables with adjustment rationale

✍️ Market context narratives – Brief written summaries explaining regional dynamics

✍️ Range valuations – Providing confidence ranges acknowledges market uncertainty

✍️ Follow-up consultations – Offering to discuss valuation findings reduces misunderstandings

This approach positions the valuer as a trusted advisor rather than merely a number provider, building long-term client relationships even when delivering unwelcome news about property values.

Maintaining Professional Standards Under Pressure

Market divergence creates pressure to deviate from rigorous standards. Clients in stagnant markets may seek optimistic valuations, while those in growth markets may request conservative figures for tax purposes. RICS professionals must maintain independence and objectivity regardless of client preferences.

Key professional standards to reinforce:

⚖️ Independence – Valuation conclusions must reflect market evidence, not client desires

⚖️ Transparency – All assumptions, limitations, and uncertainties must be clearly disclosed

⚖️ Competence – Only accept instructions in markets where adequate expertise exists

⚖️ Objectivity – Personal opinions about market direction must not override evidence

⚖️ Diligence – Thorough investigation of all available comparable evidence is mandatory

When market conditions create valuation uncertainty, the appropriate response is to widen confidence ranges and clearly communicate limitations rather than provide false precision. A valuation stating "£475,000-£495,000" with transparent explanation of uncertainty serves clients better than an unjustified point estimate of £485,000.

Future Outlook and Emerging Considerations

Anticipated Market Evolution Through 2026

As 2026 progresses, several factors will influence whether the north-south divergence continues or begins to moderate:

Potential convergence factors:

- London affordability improvement if prices remain flat while wages grow

- Infrastructure investment in northern regions potentially accelerating growth

- Mortgage rate stabilization reducing volatility across all markets

- Return of international buyers to London if geopolitical tensions ease

Potential divergence factors:

- Continued remote work adoption reducing London premium

- Regional economic growth differentials favoring northern cities

- Stamp duty policy changes potentially affecting different regions unequally

- Climate considerations influencing long-term location preferences

Valuers should monitor these trends while avoiding predictive overreach in current valuations. Market value reflects current conditions, not forecasts, though understanding trajectory helps inform professional judgment.

Adapting to Regulatory and Industry Changes

The RICS continues to refine guidance in response to market complexity. Valuers should anticipate potential updates to Red Book standards addressing:

- Enhanced requirements for market condition adjustment documentation

- Specific guidance on regional divergence scenarios

- Updated approaches to uncertainty communication in volatile markets

- Integration of sustainability factors into valuation methodology

Staying current with professional development ensures valuers can implement evolving best practices as industry standards adapt to changing market realities.

Conclusion

Valuation Challenges in a Recovering UK Market: North-South Price Divergence and RICS Adjustment Strategies for 2026 represent the most significant professional challenge facing chartered surveyors this year. The stark contrast between northern market growth and southern stagnation—particularly London's unique underperformance—demands sophisticated application of RICS Red Book principles with heightened regional awareness.

The key to navigating these challenges lies in rigorous methodology combined with local market intelligence. Valuers must resist the temptation to apply national trends to local markets, instead building deep understanding of regional dynamics through comprehensive comparable analysis, agent networking, and continuous market monitoring.

Actionable Next Steps for Valuation Professionals

📋 Audit your comparable databases – Ensure regional segmentation and recent transaction focus

📋 Develop regional adjustment frameworks – Create documented methodologies for market condition adjustments specific to each area you serve

📋 Enhance client communication protocols – Implement visual aids and detailed explanations to bridge expectation gaps

📋 Invest in continuing professional development – Attend regional market briefings and RICS technical updates

📋 Review and update standard valuation templates – Ensure reports adequately address regional market context and adjustment transparency

📋 Build professional networks – Establish relationships with local agents, auctioneers, and other market participants in your coverage areas

The UK property market's regional divergence in 2026 creates complexity, but also opportunity for skilled professionals who can provide accurate, defensible valuations across varied market conditions. By combining RICS technical standards with deep regional expertise and transparent communication, valuers can deliver exceptional service while maintaining the professional integrity that underpins market confidence.

For property professionals seeking expert valuation services that account for regional market nuances, working with experienced registered RICS valuers ensures compliance with industry standards while benefiting from local market knowledge essential for accurate property assessment in 2026's divergent landscape.

References

[1] Uk House Prices In 2026 Where The Market Is Headed What It Means For Buyers Sellers And Landlor – https://www.approvedbusinessfinance.co.uk/post/uk-house-prices-in-2026-where-the-market-is-headed-what-it-means-for-buyers-sellers-and-landlor

[2] House Price Forecast – https://hoa.org.uk/advice/guides-for-homeowners/i-am-buying/house-price-forecast/

[3] Post Budget 2026 Valuation Challenges Surveyor Strategies For High Value Properties Over 2 Million – https://nottinghillsurveyors.com/blog/post-budget-2026-valuation-challenges-surveyor-strategies-for-high-value-properties-over-2-million

[4] Watch – https://www.youtube.com/watch?v=fneUjaj5fMw