When property valuation becomes necessary—whether for securing a mortgage, settling a divorce, or resolving a tax matter—understanding the critical difference between a RICS Red Book valuation and a standard market appraisal can save UK homeowners, landlords, and lenders significant time, money, and legal complications. In 2026, with updated regulatory standards and enhanced ESG requirements, knowing which type of valuation your situation demands has never been more important.

Many property owners mistakenly believe that the free valuation from an estate agent serves the same purpose as a formal RICS valuation—a misconception that can prove costly when legal, financial, or regulatory scrutiny arises. This comprehensive guide explains RICS Red Book Valuations vs. Market Appraisals: What UK Homeowners, Landlords and Lenders Need to Know in 2026, clarifying when each is appropriate and why the distinction matters for lending, tax, matrimonial, and dispute purposes.

Key Takeaways

✅ RICS Red Book valuations are formal, regulated assessments required for legal, tax, lending, and dispute purposes, while market appraisals are informal estimates typically used for marketing properties.

✅ Lenders, courts, HMRC, and legal professionals only accept RICS-compliant valuations due to their adherence to international standards and professional indemnity insurance requirements.

✅ Since January 31, 2025, updated Red Book standards mandate ESG considerations, valuer rotation rules, and enhanced transparency in methodology—making professional valuations more comprehensive than ever.

✅ Costs differ significantly: market appraisals are often free or low-cost marketing tools, while Red Book valuations typically range from £250-£1,500+ depending on property complexity and purpose.

✅ Choosing the wrong type can invalidate legal proceedings, delay mortgage approvals, or result in incorrect tax assessments—making professional guidance essential.

Understanding the Fundamental Differences Between RICS Red Book Valuations and Market Appraisals

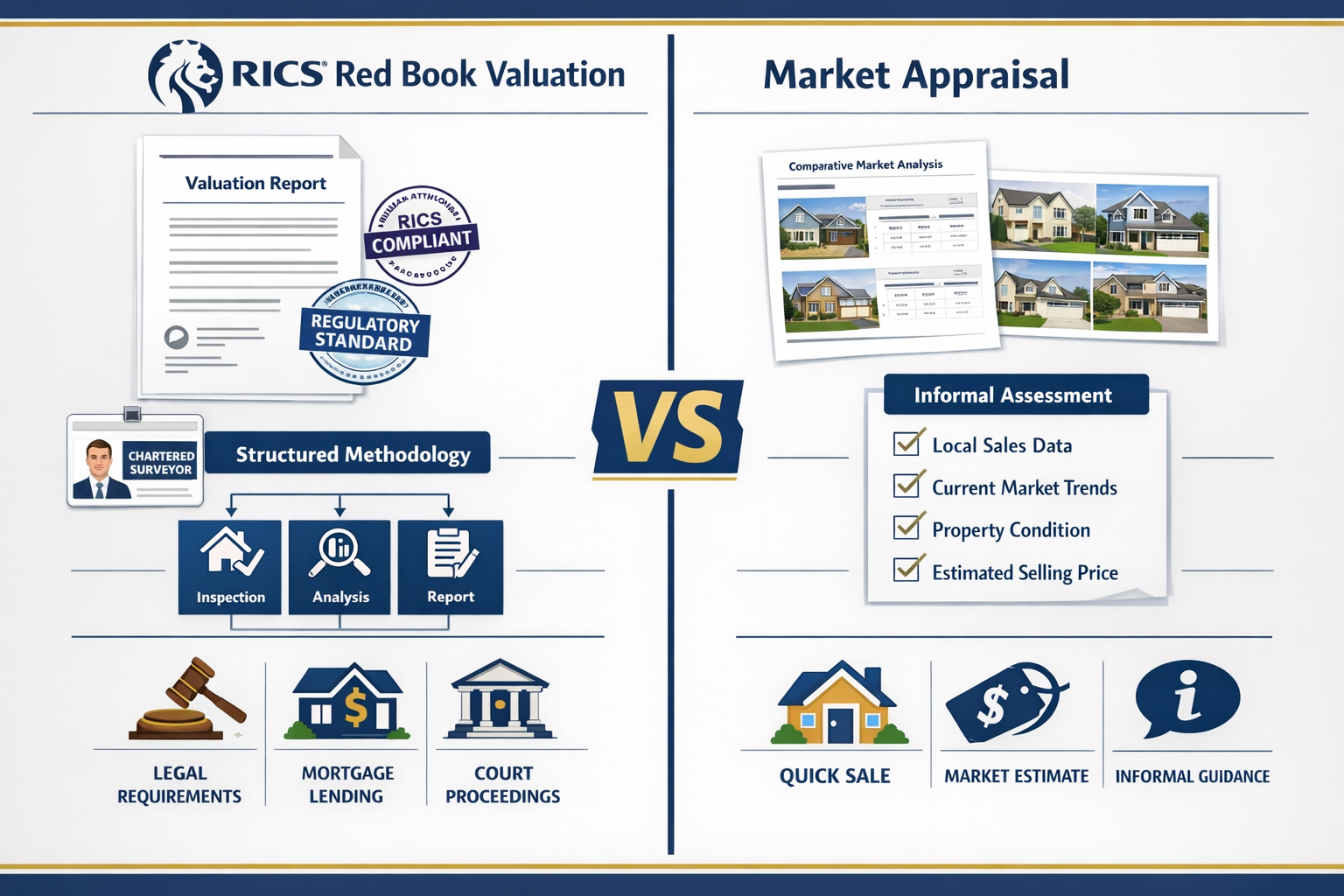

The distinction between RICS Red Book valuations and market appraisals centres on regulatory compliance, professional accountability, and legal recognition. While both involve assessing property value, they serve fundamentally different purposes and carry vastly different weight in formal proceedings.

What Is a RICS Red Book Valuation?

A RICS Red Book valuation is a formal property assessment conducted by a qualified chartered surveyor in accordance with the Royal Institution of Chartered Surveyors' Valuation – Global Standards (commonly known as the "Red Book"). These valuations must comply with:

- International Valuation Standards (IVS)

- UK-specific regulatory requirements

- Professional practice standards

- Mandatory reporting formats

The Red Book framework ensures consistency, transparency, and accountability across all valuations. Chartered surveyors performing these assessments must:

🔹 Hold appropriate RICS qualifications and memberships

🔹 Carry professional indemnity insurance

🔹 Declare any conflicts of interest

🔹 Follow prescribed methodologies

🔹 Provide detailed written reports with supporting evidence

Since the January 31, 2025 implementation of updated standards, Red Book valuations now incorporate mandatory ESG (Environmental, Social, Governance) considerations, including energy efficiency ratings, carbon footprint assessments, and sustainability factors that increasingly affect property values in 2026.

What Is a Market Appraisal?

A market appraisal (also called a "market valuation" or "estate agent valuation") is an informal estimate of a property's likely selling price, typically provided by estate agents as part of their marketing services. These appraisals:

- Are not regulated by professional standards bodies

- Require no specific qualifications to perform

- Carry no professional indemnity insurance

- Follow no standardized methodology

- Provide no legal standing in formal proceedings

Estate agents use market appraisals primarily as marketing tools to win instruction to sell properties. While experienced agents can provide valuable market insights, their estimates often reflect:

📊 Recent comparable sales in the area

📊 Current market conditions and buyer demand

📊 The agent's desire to secure the listing

📊 Marketing strategy considerations

The lack of regulatory oversight means market appraisals can vary significantly between agents viewing the same property—sometimes by tens of thousands of pounds.

Key Differences at a Glance

| Feature | RICS Red Book Valuation | Market Appraisal |

|---|---|---|

| Regulatory Status | Fully regulated, must comply with Red Book standards | Unregulated, no mandatory standards |

| Qualified Professional | RICS chartered surveyor required | Any estate agent can provide |

| Professional Insurance | Mandatory professional indemnity insurance | Not required |

| Legal Recognition | Accepted by courts, lenders, HMRC | Not accepted for formal purposes |

| Methodology | Standardized, evidence-based approach | Varies by agent, often marketing-focused |

| Written Report | Detailed formal report required | Often verbal or brief written estimate |

| Cost | £250-£1,500+ depending on complexity | Usually free (marketing tool) |

| Purpose | Legal, tax, lending, dispute resolution | Property marketing and sale pricing |

| ESG Considerations | Mandatory since 2025 updates | Not typically included |

| Liability | Surveyor professionally liable | Limited or no liability |

Understanding these valuation factors helps property stakeholders choose the appropriate assessment type for their specific needs.

When UK Homeowners, Landlords and Lenders Require RICS Red Book Valuations in 2026

Certain situations legally require or strongly benefit from RICS-compliant valuations rather than informal market appraisals. Understanding when RICS Red Book Valuations vs. Market Appraisals: What UK Homeowners, Landlords and Lenders Need to Know in 2026 becomes critical in these contexts:

Mortgage Lending and Remortgaging

All UK mortgage lenders require RICS Red Book valuations to assess lending risk. When homeowners or landlords apply for:

- Purchase mortgages

- Remortgage applications

- Buy-to-let financing

- Equity release products

- Commercial property loans

Lenders commission their own RICS valuations (often at the borrower's expense) because only Red Book-compliant assessments provide the professional assurance and legal protection necessary for lending decisions. Market appraisals from estate agents are never accepted for mortgage purposes.

The 2025 Red Book updates mean lenders now receive valuations incorporating sustainability metrics, which increasingly influence lending decisions as financial institutions factor climate risk into their portfolios.

Matrimonial and Divorce Proceedings

When couples divorce or separate, family courts require RICS valuations for fair asset division. A divorce valuation must be:

✔️ Impartial and independent

✔️ Professionally qualified and insured

✔️ Compliant with court requirements

✔️ Defensible under cross-examination

Courts reject market appraisals because estate agents lack the professional standing and accountability required for legal proceedings. Both parties may instruct separate RICS surveyors, with courts often appointing a single joint expert to avoid conflicting valuations.

Probate and Estate Administration

Following a death, executors must value the deceased's estate for inheritance tax purposes. HMRC requires probate valuations to be:

- Accurate as of the date of death

- Conducted by qualified professionals

- Supported by evidence and methodology

- Defensible if challenged

While HMRC technically accepts valuations from estate agents for properties under certain thresholds, RICS valuations provide superior protection against challenges and potential penalties for undervaluation. For complex estates, shared ownership properties, or high-value assets, Red Book compliance is essential.

Tax Purposes (Capital Gains, ATED, and More)

Various tax scenarios demand RICS valuations:

Capital Gains Tax (CGT): When calculating gains on property disposals, HMRC may require valuations for:

- Properties owned before 1982

- Inherited properties at probate value

- Properties becoming rental investments

Annual Tax on Enveloped Dwellings (ATED): Companies owning UK residential property over £500,000 require ATED valuations every five years.

Stamp Duty Land Tax: Disputed property values may require independent RICS assessment.

Market appraisals carry no weight with HMRC, and relying on them can result in disputes, penalties, and additional tax liabilities.

Lease Extensions and Enfranchisement

Leaseholders seeking to extend leases or pursue collective enfranchisement require RICS valuations to determine:

- Premium payable to the freeholder

- Marriage value calculations

- Diminution in freeholder's interest

The Leasehold Reform (Ground Rent) Act and ongoing leasehold reforms in 2026 make professional valuations increasingly important for these transactions. Freehold valuations must follow prescribed statutory methodologies that only qualified surveyors can properly apply.

Litigation and Expert Witness Testimony

When property disputes reach court—whether boundary disputes, professional negligence claims, or commercial disagreements—only RICS-qualified expert witnesses can provide admissible valuation evidence. Courts require:

🏛️ Professional qualifications and experience

🏛️ Compliance with Civil Procedure Rules

🏛️ Independence from parties involved

🏛️ Ability to withstand cross-examination

Estate agents cannot serve as expert witnesses in property valuation disputes, making Red Book compliance essential for litigation purposes.

Charitable and Statutory Purposes

Charities disposing of land require Charities Act valuations to demonstrate they've obtained the best price reasonably obtainable. Similarly, statutory compensation claims, compulsory purchase orders, and public sector transactions all demand RICS-compliant assessments.

Help to Buy and Shared Ownership Schemes

Government-backed schemes require specific valuation approaches:

- Help to Buy valuations for equity loan calculations

- Shared ownership property valuations for staircasing transactions

These specialized valuations must follow Red Book standards to ensure compliance with scheme requirements and protect all parties involved.

The 2025-2026 Red Book Updates: What's Changed and Why It Matters

Understanding RICS Red Book Valuations vs. Market Appraisals: What UK Homeowners, Landlords and Lenders Need to Know in 2026 requires awareness of significant regulatory changes implemented in early 2025 that continue to shape valuation practice throughout 2026.

January 31, 2025: Implementation of New Global Standards

The updated RICS Valuation – Global Standards became effective on January 31, 2025, following publication in December 2024. These changes introduced several important requirements that distinguish professional valuations even further from informal market appraisals.

Mandatory ESG Considerations

Perhaps the most significant change for 2026 is the mandatory incorporation of Environmental, Social, and Governance (ESG) factors into Red Book valuations. Chartered surveyors must now:

🌱 Assess energy efficiency and EPC ratings

🌱 Consider carbon footprint and emissions

🌱 Evaluate sustainability features (solar panels, insulation, green technologies)

🌱 Account for climate risk (flooding, overheating, future resilience)

🌱 Analyze market impact of environmental performance

This represents a fundamental shift in how properties are valued. In 2026, two otherwise identical properties can have significantly different valuations based solely on their environmental credentials. Properties with poor EPC ratings (E, F, or G) face valuation penalties as buyers and lenders increasingly factor in:

- Future improvement costs to meet rental standards

- Reduced buyer demand for inefficient properties

- Potential regulatory restrictions on sales or lettings

- Higher running costs affecting affordability

Market appraisals from estate agents rarely incorporate these sophisticated ESG considerations, potentially misleading sellers about their property's true market value in the current regulatory environment.

AI and Technology Transparency Requirements

The 2025 updates require valuers to clearly disclose any AI-driven data analysis used in their assessments. As valuation technology advances, the Red Book ensures transparency about:

- Automated valuation models (AVMs) and their limitations

- Data sources and reliability

- Human oversight and professional judgment

- Technology's role versus surveyor expertise

This transparency distinguishes professional RICS valuations from algorithm-based estimates that lack professional accountability.

Valuer Rotation Rules for Regulated Purposes

New valuer rotation requirements apply to regulated purpose valuations (primarily affecting financial institutions and investment funds):

📋 Maximum five-year initial engagement periods

📋 Ten-year firm rotation limits

📋 Five-year individual valuer tenure restrictions

These rules enhance independence and prevent over-familiarity between valuers and clients. However, all public sector valuations are excluded from these rotation requirements.

For individual homeowners and landlords, these rotation rules have limited direct impact, but they demonstrate the Red Book's emphasis on independence and objectivity—qualities entirely absent from market appraisals where agents have vested interests in securing listings.

Enhanced Reporting Standards

The updated standards require more detailed reporting, including:

- Clearer methodology explanations

- More comprehensive comparable evidence

- Explicit assumptions and special assumptions

- Enhanced uncertainty disclosure

- Sustainability and ESG commentary

These requirements ensure clients receive comprehensive, transparent valuations that can withstand scrutiny in legal, lending, or regulatory contexts—something informal appraisals simply cannot provide.

Minimal Client Disruption

Despite these significant updates, RICS advised that recipients of valuations would experience minimal disruption. The changes primarily affect how surveyors conduct and report valuations rather than fundamentally altering the client experience. However, clients can expect:

✅ More comprehensive reports with ESG analysis

✅ Potentially longer turnaround times for complex properties

✅ More detailed questioning about sustainability features

✅ Enhanced professional service reflecting current best practices

Choosing Between RICS Valuations and Market Appraisals: Practical Guidance for 2026

Understanding when to commission each type of assessment helps UK homeowners, landlords, and lenders make informed decisions about RICS Red Book Valuations vs. Market Appraisals: What UK Homeowners, Landlords and Lenders Need to Know in 2026.

When a Market Appraisal Is Sufficient

Market appraisals serve legitimate purposes in specific circumstances:

✓ Initial marketing price guidance: When first considering selling, obtaining multiple agent appraisals helps gauge market positioning.

✓ Informal value estimates: For general awareness of property value without legal or financial implications.

✓ Rental pricing guidance: When setting rental rates for lettings (though professional rental valuations exist for formal purposes).

✓ Agent selection: Comparing agent estimates as part of choosing an estate agent to instruct.

Important caveat: Never rely solely on market appraisals for financial decisions, tax planning, or legal matters, even if they seem adequate for informal purposes.

When a RICS Red Book Valuation Is Essential

Commission a professional Red Book valuation whenever:

🔴 Legal proceedings are involved or anticipated

🔴 Mortgage lending or refinancing is required

🔴 Tax implications exist (inheritance, capital gains, ATED)

🔴 Formal disputes need independent assessment

🔴 Statutory requirements demand professional valuation

🔴 Significant financial decisions depend on accurate value

🔴 Professional accountability and insurance protection matter

Cost Considerations and Value for Money

While market appraisals are typically free, the price of professional valuations reflects the expertise, liability, and regulatory compliance involved:

Residential RICS valuations: £250-£800 for standard properties

Complex residential: £800-£1,500+ for unusual features, large estates

Commercial properties: £1,000-£5,000+ depending on complexity

Specialist valuations: Variable based on purpose and complexity

This investment provides:

- Professional indemnity insurance protection

- Legal defensibility if challenged

- Regulatory compliance for formal purposes

- Peace of mind from qualified expertise

- Detailed documentation supporting the valuation

The cost of an inappropriate market appraisal—leading to rejected mortgage applications, HMRC penalties, or lost legal cases—far exceeds the investment in proper professional valuation.

Understanding Different Valuation Methods

Professional surveyors employ various methods of valuation depending on property type and purpose:

Comparative method: Most common for residential properties, analyzing recent comparable sales.

Investment method: Used for rental properties, calculating value based on income potential.

Residual method: Applied to development sites, working backward from completed value.

Profits method: For specialized properties like hotels or care homes.

Depreciated replacement cost: For unique properties with no market comparables.

Market appraisals typically use only crude comparative analysis without the rigor and evidence required by Red Book standards.

Questions to Ask When Commissioning a Valuation

When engaging a chartered surveyor for a Red Book valuation, ask:

❓ Are you RICS-qualified and registered?

❓ Do you have professional indemnity insurance?

❓ Have you conducted similar valuations recently?

❓ What is your experience with [property type/purpose]?

❓ Will the valuation comply with current Red Book standards?

❓ How will ESG factors be incorporated?

❓ What is the turnaround time?

❓ What exactly is included in the fee?

❓ Will you be available to explain the report if needed?

For complex situations—such as commercial property valuations, reinstatement cost assessments, or specialized purposes—ensure the surveyor has specific relevant experience.

The Importance of Independence and Objectivity

A critical advantage of RICS valuations over market appraisals is independence. Estate agents have inherent conflicts of interest:

⚠️ Commission incentive: Agents earn fees based on sale prices, creating pressure to inflate values

⚠️ Listing competition: Agents may overvalue to win instructions

⚠️ Market positioning: Strategic pricing may not reflect true market value

RICS surveyors, by contrast, must:

✅ Declare conflicts of interest or decline instructions

✅ Provide impartial assessments regardless of client preferences

✅ Follow evidence-based methodology rather than marketing strategy

✅ Maintain professional standards under regulatory oversight

This independence makes Red Book valuations reliable for third parties (lenders, courts, tax authorities) who need objective assessments.

Regional Considerations Across the UK

Property markets vary significantly across the UK, affecting both valuation approaches and market conditions. Whether seeking valuation services in London or elsewhere, ensure your surveyor has local market knowledge combined with Red Book compliance.

Regional factors affecting valuations in 2026 include:

- Local planning policies and development potential

- Regional economic conditions and employment

- Transport infrastructure and connectivity

- School catchment areas and local amenities

- Environmental risks (flooding, coastal erosion, subsidence)

- Local market dynamics and buyer demographics

Professional surveyors combine this local expertise with standardized methodology, whereas market appraisals may rely too heavily on local knowledge without proper analytical framework.

Conclusion: Making Informed Decisions About Property Valuations in 2026

The distinction between RICS Red Book valuations and market appraisals represents far more than a technical difference in methodology—it reflects the fundamental divide between regulated professional service and informal marketing estimates. For UK homeowners, landlords, and lenders navigating property decisions in 2026, understanding when each type of assessment is appropriate can prevent costly mistakes, legal complications, and financial losses.

RICS Red Book valuations provide the professional accountability, regulatory compliance, and legal recognition essential for mortgage lending, tax purposes, divorce proceedings, probate, litigation, and statutory requirements. The January 2025 updates incorporating mandatory ESG considerations, enhanced transparency, and valuer rotation rules have strengthened these professional standards even further, ensuring valuations reflect contemporary market realities including sustainability and climate considerations.

Market appraisals, while useful for initial marketing guidance and informal value estimates, lack the professional standing, insurance protection, and evidentiary weight required for formal purposes. Their role remains limited to preliminary property marketing decisions rather than situations with legal, financial, or regulatory implications.

Actionable Next Steps

For homeowners, landlords, and lenders requiring property valuations in 2026:

1. Identify your specific purpose: Determine whether your situation requires formal Red Book compliance or if an informal appraisal suffices.

2. Engage qualified professionals: For RICS valuations, verify surveyor credentials, insurance, and relevant experience. Explore comprehensive valuation services from qualified chartered surveyors.

3. Budget appropriately: Recognize that professional valuations represent investments in accuracy, accountability, and legal protection rather than unnecessary expenses.

4. Provide complete information: Share all relevant property details, including sustainability features, planning permissions, and any defects or issues.

5. Understand the methodology: Ask surveyors to explain their approach and how current Red Book standards apply to your property.

6. Keep documentation: Retain valuation reports for future reference, tax purposes, and potential disputes.

7. Seek specialist advice when needed: Complex situations may require specialist valuers with specific expertise beyond general practice.

The property market continues evolving, with sustainability, technology, and regulatory changes shaping how properties are valued and transacted. By understanding the critical differences between RICS Red Book valuations and market appraisals, property stakeholders can make informed decisions that protect their interests and ensure compliance with current standards throughout 2026 and beyond.

Whether securing financing, resolving legal matters, or planning tax-efficient strategies, the choice between professional valuation and informal appraisal should reflect the stakes involved and the consequences of inaccuracy. In situations where property value determines financial, legal, or regulatory outcomes, the expertise, accountability, and recognition of RICS Red Book valuations remain irreplaceable.