{"cover":"Professional landscape format (1536×1024) hero image with bold text overlay: 'Scotland & Northern Ireland Price Surges: Building Survey Adjustments for RICS Jan 2026' in extra large 72pt white bold sans-serif font with dark semi-transparent background bar for contrast, centered upper third. Background shows dramatic split composition: left side Edinburgh castle skyline with Georgian terraced housing, right side Belfast Victorian red-brick townhouses, both under a moody blue-grey sky. Foreground features a RICS-branded survey clipboard and rising price graph arrow overlay. Color palette: deep navy blue, white, gold accent. Magazine cover editorial quality, high contrast, professional.","content":["Detailed landscape format (1536×1024) infographic-style image showing a UK regional heat map with Scotland and Northern Ireland glowing in bright amber/gold indicating strongest price growth, contrasted against muted grey tones for London and South East. Overlaid bar chart showing RICS net balance figures: Northern Ireland +41%, Scotland +21% new buyer enquiries. Clean white background sections with data labels, upward trend arrows, RICS logo watermark, professional financial data visualization aesthetic, editorial quality.","Landscape format (1536×1024) showing a RICS Level 3 Building Survey in progress: close-up aerial perspective of a chartered surveyor in high-visibility vest and hard hat inspecting the stone masonry and roof of a traditional Scottish granite detached house, holding a tablet with digital survey checklist. Autumn morning light, misty hills in background. Inset panel shows construction cost index graph rising 4.25% with BCIS branding. Professional documentary photography style, warm natural tones, editorial quality.","Landscape format (1536×1024) depicting a professional surveyor consultation scene set in a modern Belfast office: two chartered surveyors reviewing large printed valuation adjustment reports spread across a glass desk, with a laptop showing RICS Jan 2026 market data dashboard. Wall-mounted screen displays Northern Ireland construction output chart hitting 15-year high. Bookshelves with RICS Red Book and professional references visible. Warm office lighting, business professional tone, editorial quality, distinct from previous images."]

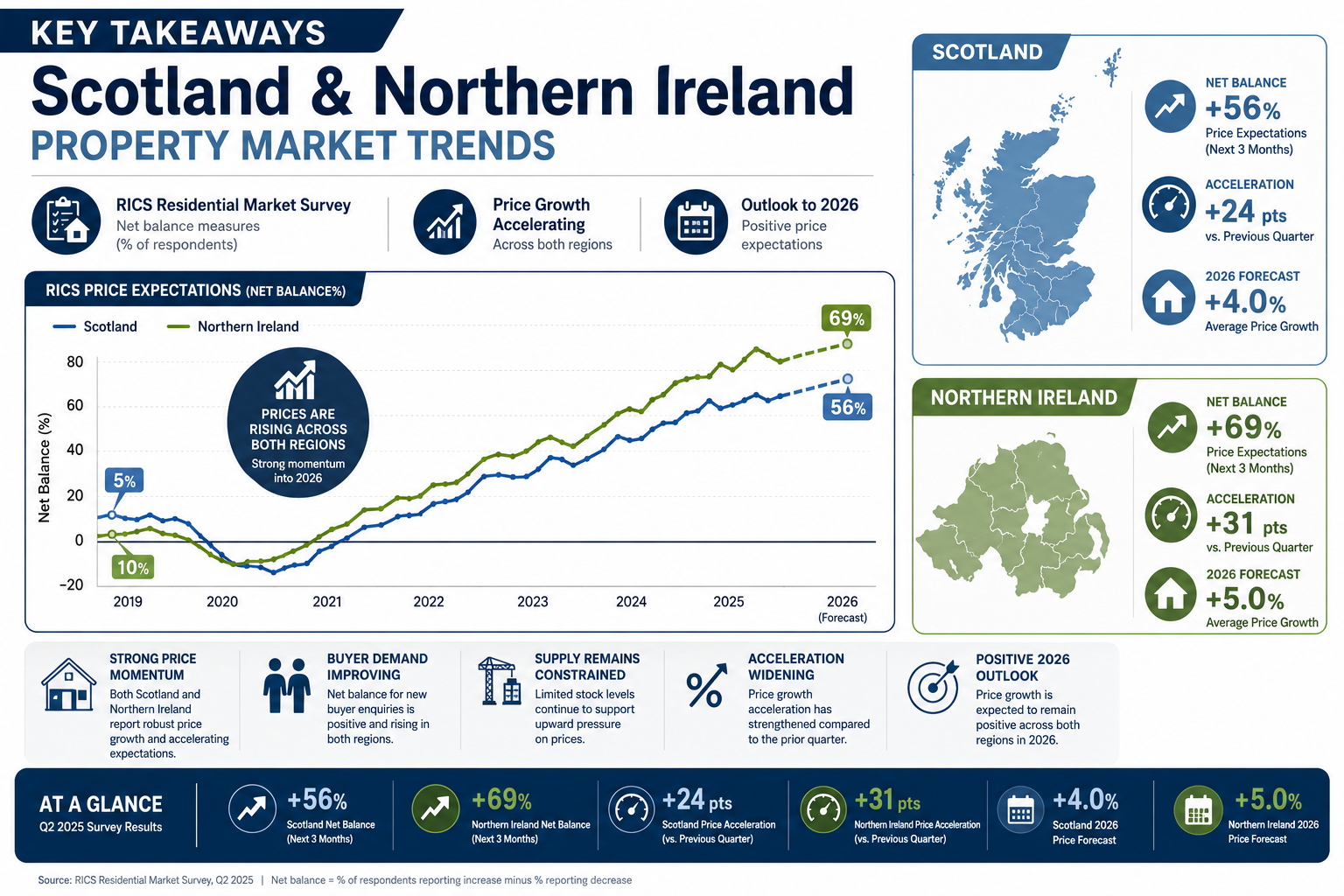

A net balance of 41% of Northern Ireland surveyors reported rising new buyer enquiries in January 2026 — the highest reading in the region for years — while Scotland recorded a +21% net balance on the same measure. These are not modest fluctuations. They are structural signals that demand a direct response from every chartered surveyor, property buyer, and developer operating in these markets. Understanding Scotland and Northern Ireland price surges: building survey adjustments for RICS Jan 2026 upward trends is no longer optional for professionals who want to deliver accurate valuations and sound advice in rapidly shifting regional markets [1][2].

Key Takeaways 📌

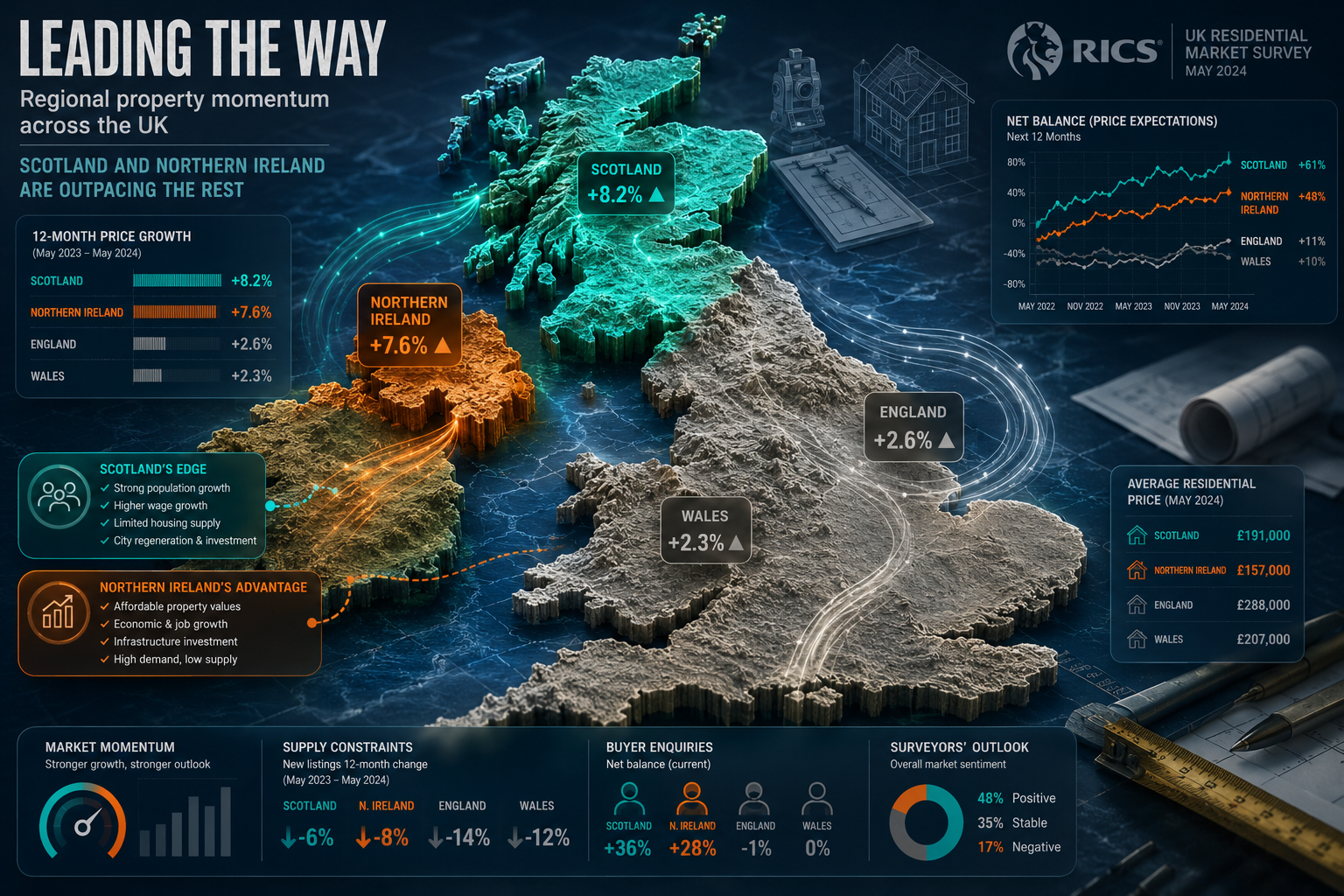

- 🏴 Scotland and Northern Ireland are the UK's strongest-performing price regions in January 2026, according to the RICS UK Residential Market Survey.

- 📈 Construction costs in Scotland rose 4.25% year-on-year to Q1 2026, directly affecting rebuild and reinstatement valuations.

- 🏗️ Northern Ireland's construction output hit a 15-year high, creating supply chain pressures that surveyors must factor into Level 3 assessments.

- 🔍 RICS Level 3 Building Surveys need regional cost calibration to remain accurate in high-growth areas — standard national benchmarks are no longer sufficient.

- ⚠️ Tender price inflation of 3.5%–5% per year is forecast through 2026–2027, meaning survey-based cost estimates must build in forward-looking buffers.

Why Scotland and Northern Ireland Are Outpacing the Rest of the UK

The RICS UK Residential Market Survey for January 2026 paints a clear picture: while the national house price balance improved marginally from -13% in December 2025 to -10% in January 2026, the regional story is far more dramatic [8]. Scotland and Northern Ireland are not simply recovering — they are accelerating, and in opposite directions to London and the South East, where affordability constraints continue to suppress demand.

The Demand Picture

In Northern Ireland, the net balance of new buyer enquiries jumped to 41% in January 2026, up from 35% in the previous survey period [2]. This is a meaningful leap. In Scotland, surveyors reported a +21% net balance on new buyer enquiries, alongside a +27% net balance on new instructions to sell — a combination that historically precedes a sustained rise in agreed sales [5].

What is driving this? Several converging factors:

- Relative affordability: Average house prices in Scotland and Northern Ireland remain significantly lower than in England's commuter belts, attracting first-time buyers and relocators.

- Remote working permanence: Buyers are no longer anchored to major English cities, expanding their search radius into more affordable Celtic nations.

- Post-pandemic catch-up: Both regions experienced compressed transaction volumes during 2022–2023; pent-up demand is now releasing.

- Supply constraints: Limited new housing stock in key urban areas — Edinburgh, Glasgow, Belfast, and Derry — is amplifying price competition.

💬 "Regional disparities are widening, with Scotland and Northern Ireland leading in price growth while London and the South East continue to face affordability headwinds." — RICS UK Residential Market Survey, January 2026 [1]

Construction Cost Pressures Compound the Trend

Rising demand is only half the equation. On the supply and cost side, the Building Cost Information Service (BCIS) reported a 4.25% increase in construction input costs in Scotland over the year leading to Q1 2026 [3]. This rise is linked to an unpredictable project pipeline and regional market growth variations — factors that directly affect how surveyors must approach reinstatement cost assessments and repair estimates within building surveys.

Meanwhile, Turner & Townsend's Winter 2025 UK Market Intelligence report forecasts tender price inflation of 3.5% per year across real estate and 5% for infrastructure through 2026 and 2027 [9]. These are not background numbers. They are the arithmetic that underpins every cost schedule a surveyor produces.

Building Survey Adjustments for RICS Jan 2026 Upward Trends: What Surveyors Must Do Differently

The Scotland and Northern Ireland price surges and building survey adjustments for RICS Jan 2026 upward trends require surveyors to move beyond templated national benchmarks. Here is a structured breakdown of the adaptations required.

1. Recalibrate Reinstatement Cost Assessments

Reinstatement cost assessments (RCAs) embedded within Level 3 Building Surveys must reflect current regional labour and material costs, not national averages. With Scottish construction input costs up 4.25% year-on-year [3], a surveyor relying on 2024 BCIS regional factors without updating them risks producing a figure that is materially understated.

Practical steps:

- Cross-reference the latest BCIS regional location factors for Scotland and Northern Ireland quarterly.

- Apply forward-looking inflation buffers of at least 3.5%–5% to cost estimates that will be used for insurance or project planning beyond a 12-month horizon [9].

- Flag explicitly in survey reports that regional cost escalation is ongoing and that estimates should be reviewed annually.

For clients seeking a RICS Home Survey or Level 3 Building Survey, these regional adjustments should be clearly communicated as part of the reporting narrative.

2. Upgrade Defect Severity Ratings in High-Demand Markets

In a rising market, buyers under competitive pressure are more likely to proceed despite identified defects. Surveyors have a professional obligation to ensure that Condition Ratings 2 and 3 defects are described with sufficient specificity to cut through buyer optimism. This means:

- Providing cost ranges (not just descriptions) for significant repairs, calibrated to regional contractor rates.

- Noting where specialist follow-up investigations are required — particularly for properties in Scotland's older granite and sandstone stock, or Northern Ireland's Victorian red-brick terraces, both of which carry specific damp, structural, and roofing vulnerabilities.

- Recommending damp surveys or structural surveys where the Level 3 inspection identifies indicators that warrant deeper investigation.

3. Adjust Comparable Evidence Weighting

For surveyors also providing market valuations alongside building surveys, the rapidly shifting price environment in Scotland and Northern Ireland demands tighter comparable evidence windows. Using comparables older than three to four months in these markets risks producing a valuation that is already stale at the point of delivery.

Recommended approach:

| Comparable Age | Weighting in Rising Market |

|---|---|

| 0–2 months | Primary evidence — full weight |

| 3–4 months | Secondary evidence — apply upward time adjustment |

| 5–6 months | Use with caution — significant adjustment required |

| 6+ months | Avoid unless no alternatives exist |

Understanding valuation factors in the context of regional price surges is essential for producing defensible Red Book valuations.

4. Factor in Northern Ireland's Construction Output Surge

Northern Ireland's construction output increased by 7.3% as of mid-2025, reaching its highest level since 2010 [4]. This growth — driven by strong repair and maintenance activity and a significant rise in housing output — has two direct implications for surveyors:

- Labour availability is tighter: Contractor quotes for remedial works identified in surveys may be harder to obtain and more expensive than in previous years.

- New-build snagging demands are higher: With housing output at a 15-year high, the volume of new properties requiring snagging inspections has risen sharply. Surveyors should expect increased instruction volumes and plan capacity accordingly.

5. Housebuilding Activity as a Survey Volume Indicator

The RICS Construction Monitor for Q1 2026 shows that while overall construction activity in Scotland remained relatively subdued, housebuilding activity rose, with a net balance of 3% reporting increased workloads [6]. This is a leading indicator: more new homes entering the market means more pre-purchase survey instructions in the pipeline.

Surveyors operating in Scotland should prepare for:

- Higher instruction volumes in urban growth corridors (Edinburgh, Glasgow, Aberdeen).

- Greater demand for Level 2 versus Level 3 survey comparisons as buyers navigate which product suits their purchase.

- Increased requests for schedule of condition reports on older properties adjacent to new development sites.

Strategic Implications for Buyers, Developers, and Lenders

The Scotland and Northern Ireland price surges and building survey adjustments for RICS Jan 2026 upward trends carry distinct implications depending on your role in the transaction.

For Property Buyers 🏠

Do not let competitive market conditions compress your due diligence. In a bidding environment, the temptation to skip or downgrade a survey is real — and dangerous. A Level 3 Building Survey remains the most comprehensive pre-purchase protection available, and its cost is trivial relative to the repair bills it can uncover.

Key actions:

- Commission a survey early — before finalising your offer where possible, or immediately after offer acceptance.

- Request regional cost estimates within the survey report, not just condition ratings.

- Ask your surveyor explicitly whether their reinstatement cost figures reflect current Scottish or Northern Irish construction cost indices.

Understanding surveyor pricing in the context of regional market conditions helps buyers budget accurately for professional advice.

For Developers and Investors 🏗️

Rising prices and construction costs create a narrowing viability window. The RICS Scotland Manifesto 2026 specifically highlights the need to boost housing delivery and address skills and capacity challenges in the built environment [7]. Developers must:

- Build cost escalation buffers of at least 5% into project appraisals for infrastructure-heavy schemes.

- Commission commercial building surveys on acquisition targets that reflect current regional contractor rates.

- Engage chartered surveyors with demonstrable regional expertise — national firms applying London cost matrices to Scottish or Northern Irish projects will produce unreliable outputs.

For Mortgage Lenders and Valuers 🏦

The improvement in the RICS house price balance — from -13% in December 2025 to -10% in January 2026 nationally, with Scotland and Northern Ireland in positive territory — signals that loan-to-value ratios calculated on 2025 valuations may already be conservative in these regions [8]. Lenders should:

- Trigger revaluation reviews on properties in Scotland and Northern Ireland where valuations are more than six months old.

- Ensure panel valuers are applying current regional comparable evidence rather than national indices.

- Consider instructing RICS Red Book valuations for higher-value or complex properties where market movement creates material uncertainty.

The RICS Framework: Net Balance Data as a Regional Adaptation Tool

The RICS net balance methodology — which measures the percentage of surveyors reporting an increase minus those reporting a decrease — is more than a headline statistic. For surveyors adapting their practice to regional conditions, it is a calibration instrument.

Here is how to use it practically:

| RICS Net Balance Indicator | What It Signals for Surveyors |

|---|---|

| New buyer enquiries (NI: +41%) | Rising transaction volumes → increase survey capacity |

| New instructions to sell (Scotland: +27%) | More stock entering market → more pre-purchase surveys |

| Price balance (national: -10%, improving) | Cost estimates need upward adjustment in positive regions |

| Sales expectations (positive in both regions) | Plan for sustained instruction volumes through H1 2026 |

💬 "Several indicators are becoming less negative, with house prices appearing to stabilise at a national level — but the regional story in Scotland and Northern Ireland is one of genuine growth, not merely stabilisation." — RICS UK Residential Market Survey, January 2026 [1]

The practical implication is clear: surveyors in Scotland and Northern Ireland should treat the January 2026 RICS data not as a one-off snapshot but as confirmation of a sustained regional divergence that requires permanent adjustments to methodology, cost benchmarking, and client communication.

Conclusion: Actionable Next Steps for Navigating the 2026 Regional Surge

The convergence of rising buyer demand, escalating construction costs, and tightening supply in Scotland and Northern Ireland creates both opportunity and risk for everyone in the property ecosystem. The data from the RICS January 2026 survey is unambiguous: these regions are the UK's price growth leaders, and the building survey profession must adapt accordingly.

Actionable next steps:

- ✅ Update regional cost benchmarks now — pull the latest BCIS Scotland and Northern Ireland location factors and apply them to all current and pending survey instructions.

- ✅ Apply forward-looking inflation buffers of 3.5%–5% to all repair cost estimates and reinstatement assessments with a horizon beyond 12 months.

- ✅ Tighten comparable evidence windows to a maximum of four months in Scotland and Northern Ireland for any market valuation work.

- ✅ Commission Level 3 surveys on all pre-1980 properties in these regions — the combination of older stock and rising prices makes comprehensive inspection non-negotiable.

- ✅ Review survey capacity to meet anticipated instruction volume growth driven by rising new buyer enquiries and housebuilding output.

- ✅ Communicate regional context clearly in all survey reports — clients in high-growth markets need to understand that cost estimates carry greater uncertainty than in stable markets.

For buyers, developers, and professionals seeking expert guidance on RICS building surveys that reflect current regional market conditions, working with chartered surveyors who actively monitor and apply RICS net balance data to their methodology is the most effective form of protection in a rapidly moving market.

References

[1] UK Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution?utm_source=openai

[2] Northern Ireland Housing Market Off To A Strong Start In 2026 – https://www.businesseye.co.uk/news/northern-ireland-housing-market-off-to-a-strong-start-in-2026/?utm_source=openai

[3] Movement In Contractors Construction Costs In Scotland – https://www.bcis.co.uk/news/movement-in-contractors-construction-costs-in-scotland/?utm_source=openai

[4] Northern Ireland Construction Output Hits 15 Year High – https://www.businesseye.co.uk/news/northern-ireland-construction-output-hits-15-year-high/?utm_source=openai

[5] RICS Surveyors Expect Sales Rise In Scottish Housing Market As Demand And Supply Ticks Up – https://www.scottishconstructionnow.com/articles/rics-surveyors-expect-sales-rise-in-scottish-housing-market-as-demand-and-supply-ticks-up?utm_source=openai

[6] Construction Workloads Relatively Subdued In Scotland But Housebuilding Activity Rises – https://projectscot.com/2026/05/construction-workloads-relatively-subdued-in-scotland-but-housebuilding-activity-rises/?utm_source=openai

[7] UK Influence And Advocacy Update January 2026 – https://www.rics.org/news-insights/uk-influence-and-advocacy-update-january-2026?utm_source=openai

[8] Trading Economics — UK RICS House Price Balance – https://tradingeconomics.com/united-kingdom/rics-house-price-balance/news/525158?utm_source=openai

[9] Sustained Cost Escalation Putting Pressure On Viability Of New Projects – https://projectscot.com/2026/01/sustained-cost-escalation-putting-pressure-on-viability-of-new-projects/?utm_source=openai