Roughly one in five homes sold in the UK each year triggers a lender query about construction type — and a significant proportion of those queries result in a mortgage decline or a heavily caveated valuation. Providing clear, well-structured valuation advice for properties with non-standard construction is one of the most technically demanding responsibilities a surveyor faces, and the consequences of getting it wrong fall squarely on buyers, lenders, and the professionals who advise them.

This guide examines the key construction categories, the valuation challenges each presents, and the specific disclosures surveyors must make to protect all parties in a transaction.

Key Takeaways

- Non-standard construction includes timber frame, BISF steel frame, PRC concrete, and system-built homes — all of which present distinct valuation and lending challenges.

- A RICS Level 3 Building Survey is strongly recommended for any non-standard property; a basic HomeBuyer Report is rarely sufficient.

- Lenders assess mortgage risk based on construction type, structural condition, and the availability of specialist repair certificates.

- Surveyors must justify all value adjustments with documented comparable evidence and clearly communicate value uncertainty to both buyers and lenders.

- Buyers should engage specialist mortgage brokers and budget for higher insurance premiums and ongoing specialist maintenance costs.

What Counts as Non-Standard Construction and Why It Matters

Standard construction, in the context of UK residential property, generally refers to a home with brick or stone cavity walls, a pitched roof covered in slate or tile, and a concrete or timber suspended floor. Any significant departure from this definition — whether in the walls, roof structure, or floor — places a property in the non-standard category [6].

The most commonly encountered non-standard types include:

| Construction Type | Era | Key Characteristics |

|---|---|---|

| Timber frame | 1960s–present | Structural timber panels with cladding |

| BISF steel frame | 1945–1960s | British Iron and Steel Federation design |

| PRC concrete | 1940s–1970s | Precast reinforced concrete panels |

| Wimpey No-Fines | 1940s–1960s | Poured concrete without fine aggregate |

| Airey houses | 1940s–1950s | Precast concrete columns and cladding |

| System-built | 1950s–1980s | Various prefabricated panel systems |

| Mundic block | Cornwall/SW | Aggregate containing reactive minerals |

Each type carries a different risk profile for structural deterioration, energy performance, and mortgage availability. Providing accurate valuation advice for properties with non-standard construction requires surveyors to understand not just the construction method but the specific defects that each system is prone to developing over time [1].

Why lenders care: Mortgage lenders are primarily concerned with the resale value of a property in a forced-sale scenario. A non-standard home that is difficult to mortgage is, by definition, harder to sell — which reduces the lender's security and increases their risk exposure. This is why many high-street lenders either decline non-standard properties outright or apply significant loan-to-value restrictions.

The Surveyor's Core Obligations: Identification, Assessment, and Disclosure

Effective valuation advice for properties with non-standard construction begins with precise identification. This sounds straightforward, but many non-standard homes have been re-clad, re-roofed, or rendered to resemble conventional brick construction. A surveyor who fails to identify the underlying structure is exposed to significant professional liability.

Identifying the Construction Type

Surveyors should look for the following indicators during inspection:

- Wall thickness: Non-standard walls are often thinner or thicker than typical cavity brick construction.

- Fixings and junctions: Timber frame homes often show characteristic fixings at wall-to-floor junctions.

- Planning records and title documents: Local authority records may confirm the original construction system.

- Structural repair certificates: PRC homes that have been repaired under licensed schemes (such as the PRC Homes Ltd scheme) should carry documentation confirming the works.

Once identified, the construction type must be clearly stated in the report. Vague language such as "possibly non-standard" is not acceptable in a formal valuation document [1].

Assessing Structural Condition

A RICS Level 3 Building Survey is the appropriate instruction for any non-standard property. Basic HomeBuyer Reports and desktop valuations do not provide the depth of investigation needed to assess structural integrity, identify latent defects, or advise on remediation costs [2].

Key areas of structural assessment for common non-standard types:

- PRC concrete: Carbonation of the concrete, corrosion of the reinforcing steel, and condition of the panel joints.

- Timber frame: Interstitial condensation, fungal decay, insect infestation, and the integrity of the vapour control layer.

- BISF steel frame: Corrosion of the steel frame, condition of the external cladding, and thermal bridging.

- Mundic block: Laboratory testing to determine the class of mundic contamination (Class A, B, or C).

For properties where the floor construction is uncertain, a solid floor slab survey may be warranted to assess the condition of the sub-structure.

Documenting and Disclosing Findings

The report must clearly explain what was found, what it means for the property's structural integrity, and what further investigations are recommended. Surveyors should avoid technical jargon in buyer-facing sections of the report. The goal is to ensure that a buyer without a construction background can understand the risks they are taking on [6].

"A robust report should detail the construction type, structural integrity, and market comparisons — not simply flag the property as non-standard and leave the buyer to draw their own conclusions." [1]

Valuation Methodology for Non-Standard Properties

Valuing a non-standard property is not simply a matter of applying a percentage discount to a comparable brick-built home. The valuation must be defensible, evidence-based, and clearly explained to both the buyer and the lender. Understanding the available methods of valuation is essential before selecting the most appropriate approach.

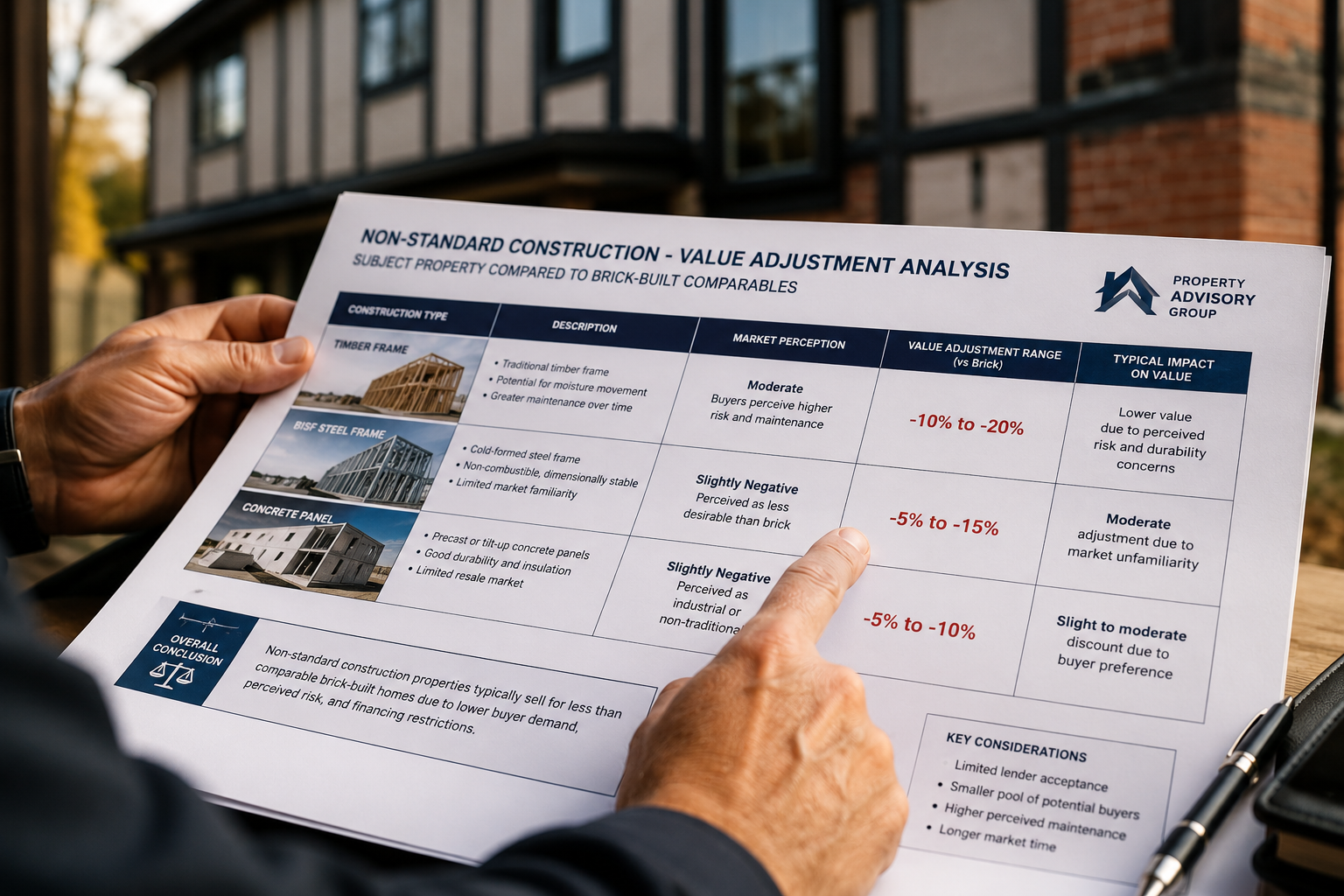

The Comparable Sales Method

The primary approach for residential valuation remains the comparison of recent sales of similar properties. For non-standard homes, this creates an immediate challenge: truly comparable sales — same construction type, similar condition, same locality — are often scarce.

Where direct comparables exist, surveyors must document:

- The sale price and date of each comparable

- The construction type of each comparable

- Any material differences in condition, size, or specification

- The adjustments made to arrive at the subject property's value

Where direct comparables are unavailable, surveyors may use sales of standard-construction properties in the same locality and apply reasoned, documented adjustments. The key word is "reasoned" — the basis for any adjustment must be explained, not simply stated [1].

The Cost Approach

For unique non-standard properties where comparable sales data is genuinely scarce, the cost approach provides a useful cross-check. This method estimates value by adding the land value to the cost of rebuilding the structure, then subtracting depreciation for age, condition, and functional obsolescence [3].

The cost approach is particularly relevant for:

- Highly unusual system-built properties with no local comparable sales

- Properties where significant structural repairs have been carried out

- Insurance reinstatement valuations for non-standard homes

For formal lending purposes, a Red Book valuation prepared in accordance with RICS Valuation — Global Standards is required. This framework mandates transparency about the methodology used and the degree of uncertainty in the final figure.

Quantifying and Communicating Value Uncertainty

Non-standard properties inherently carry greater valuation uncertainty than conventional homes. Surveyors should explicitly state the degree of this uncertainty in their reports. This is not a sign of professional weakness — it is a professional obligation and protects both the surveyor and the client.

Factors that increase valuation uncertainty include:

- Absence of comparable sales data for the specific construction type

- Unknown extent of structural deterioration behind cladding or render

- Uncertainty about the availability of mortgage finance

- Potential future changes in lender appetite for the construction type

The valuation factors that surveyors must weigh are more numerous and more complex for non-standard properties than for conventional homes, and the report should reflect this complexity honestly.

What Surveyors Must Explain to Lenders

Lenders receive a mortgage valuation report, not a full building survey. However, for non-standard properties, the valuation report must go beyond a simple opinion of value. The following information is essential for lenders to make an informed lending decision.

Construction Type and Its Implications

The report must name the construction system precisely. "Concrete construction" is insufficient; "Wimpey No-Fines poured concrete, circa 1955" gives the lender the information needed to assess their lending criteria.

Surveyors should also confirm:

- Whether the property is listed on any defective housing register

- Whether any statutory repair scheme applies (particularly relevant for PRC homes under the Housing Defects Act 1984)

- Whether repair works have been carried out to an approved standard and are evidenced by a valid certificate [1]

Mortgage and Insurance Availability

Many mainstream lenders will not lend on PRC concrete homes unless they have been repaired under an approved scheme and a valid PRC certificate is in place. BISF steel-framed homes are similarly restricted by many lenders. Timber frame homes built to modern standards are generally more widely accepted, though older examples may face restrictions.

Surveyors should note in their report where mortgage availability is likely to be restricted, even if this falls outside the strict scope of a valuation. This information is directly relevant to the lender's security and to the buyer's ability to complete the purchase [1].

Insurance costs for non-standard homes are typically higher than for conventional properties, and some specialist insurers are the only viable option for certain construction types [6]. Buyers should be advised to obtain insurance quotes before exchange of contracts.

Unpermitted Works and Legal Compliance

Non-standard properties are disproportionately likely to have had alterations carried out without building regulations approval. Extensions, loft conversions, and structural modifications to a system-built home can compromise the integrity of the original structure in ways that are not immediately visible [4].

Surveyors should flag any evidence of unpermitted works and recommend that buyers obtain indemnity insurance or retrospective building regulations approval where appropriate. The presence of such works can reduce the appraised value and may cause a lender to decline the application entirely [4].

Practical Guidance for Buyers of Non-Standard Properties

Buyers who receive valuation advice for properties with non-standard construction often feel overwhelmed by the volume of caveats and conditions in a surveyor's report. The following practical steps help buyers navigate the process effectively.

Before Making an Offer

- Identify the construction type early. Ask the estate agent or seller directly. Check the EPC register, which sometimes records construction type.

- Commission the right survey. A Level 3 Building Survey provides the most comprehensive assessment of structural condition and is the appropriate choice for non-standard properties. Understanding the differences between survey levels can help buyers make an informed decision.

- Engage a specialist mortgage broker. High-street mortgage advisers may not have access to the specialist lenders who are willing to lend on non-standard construction. A broker with experience in this area can identify viable lending options before a survey is commissioned.

After Receiving the Survey Report

- Request clarification on any technical terms. Surveyors have an obligation to communicate clearly; buyers have a right to ask for plain-language explanations.

- Obtain specialist contractor quotes. If the report recommends remediation works, obtain at least two quotes from contractors with experience in the specific construction type.

- Check for existing certificates. Sellers of PRC homes should be asked to produce a valid PRC certificate. Absence of this document is a significant red flag.

- Budget for ongoing maintenance. Non-standard homes often require specialist maintenance that cannot be carried out by a general builder [6]. This ongoing cost should be factored into the purchase decision.

Sellers of Non-Standard Properties

Sellers can improve their prospects by being transparent about the construction type from the outset and by presenting any existing structural repair certificates, planning consents, and building regulations completion certificates. Transparency reduces the risk of a transaction collapsing at the survey stage and builds buyer confidence [1].

Conclusion: Actionable Steps for Surveyors in 2026

The demand for clear, well-evidenced valuation advice for properties with non-standard construction is growing in 2026, as a generation of post-war system-built homes continues to change hands and as modern timber frame construction becomes more prevalent. Surveyors who handle these instructions well provide genuine value to buyers, lenders, and the wider property market.

Actionable steps for surveyors:

- Always identify construction type precisely. Do not rely on visual inspection alone; consult planning records, title documents, and specialist databases where necessary.

- Recommend a Level 3 Building Survey for any non-standard property, regardless of the instruction type received.

- Select and document comparables carefully. Where direct comparables are unavailable, explain the adjustments made and the basis for them.

- Quantify value uncertainty explicitly. State the range of possible values and the factors that drive that range.

- Flag mortgage and insurance implications in the report, even where this goes beyond the strict scope of a valuation instruction.

- Advise buyers to engage specialist professionals — mortgage brokers, specialist contractors, and legal advisers with experience in non-standard construction.

- Ensure all reports comply with RICS Red Book standards where a formal lending valuation is required.

For buyers and lenders working with properties in areas where non-standard construction is common, engaging local chartered surveyors with specific experience in the relevant construction types is the single most effective way to manage risk and ensure a well-informed transaction.

References

[1] Valuing Uk Properties With Significant Non Standard Construction Prc Timber Frames Bisf And More In 2026 – https://wimbledonsurveyors.com/valuing-uk-properties-with-significant-non-standard-construction-prc-timber-frames-bisf-and-more-in-2026/?utm_source=openai

[2] Non Standard Construction And Building Surveys Identifying Hidden Risks In Converted And Altered Properties – https://princesurveyors.co.uk/blog/non-standard-construction-and-building-surveys-identifying-hidden-risks-in-converted-and-altered-properties/?utm_source=openai

[3] Cost Approach To Value Methodology And Application In Appraisal – https://legalclarity.org/cost-approach-to-value-methodology-and-application-in-appraisal/?utm_source=openai

[4] How Unpermitted Work Easements And Disclosures Affect Value – https://legalclarity.org/how-unpermitted-work-easements-and-disclosures-affect-value/?utm_source=openai

[5] Class Valuations Nikkita Phanda On Uad 3 6 And Collateral Modernization What Lenders Need To Know – https://newslink.mba.org/mba-newslinks/2026/march/mba-newslink-monday-march-30-2026/class-valuations-nikkita-phanda-on-uad-3-6-and-collateral-modernization-what-lenders-need-to-know?utm_source=openai

[6] Standard Construction House 3905 – https://www.samconveyancing.co.uk/news/house-survey/standard-construction-house-3905?utm_source=openai