Approximately 5.2 million properties in England are at risk of flooding, yet until recently, the formal valuation framework treated flood resilience measures as little more than a footnote. That changes in 2026. The introduction of mandatory physical climate risk requirements under the new RICS global ESG standard — effective 30 April 2026 — means that valuation surveys for flood-resilient properties: 2026 RICS adjustments post-EA updates are no longer a niche specialism. They are a core professional obligation for every RICS-regulated valuer working on affected assets.

This article explains what has changed, why it matters, and precisely how surveyors should incorporate flood risk data and resilience measures into their valuation methodology.

Key Takeaways

- From 30 April 2026, RICS members must treat physical climate risk — including flood exposure — as a mandatory component of commercial property valuations, not optional commentary.

- The RICS October 2025 insight paper on flooding instructs valuers to use Environment Agency flood maps, climate-change allowances, and local flood authority data as standard inputs.

- Flood-resilience measures such as flood doors, raised electrics, and resilient materials are now explicitly value-relevant factors that must be evidenced in valuation reports.

- Valuers are expected to assess exposure to 2050 climate scenarios and evaluate planned adaptation capital expenditure.

- Residential and commercial surveyors both need to understand how the updated EA flood data integrates with RICS Red Book requirements.

Why 2026 Marks a Turning Point for Flood Risk Valuation

For years, flood risk sat in the margins of property valuation. A surveyor might note proximity to a watercourse or flag a property's flood zone classification, but the analytical weight given to that information — and to any measures installed to counter it — was largely discretionary. That discretion has now been formally removed.

The New RICS ESG Standard: Physical Climate Risk Goes Mandatory

The 4th edition of the RICS global professional standard on ESG in commercial property valuation takes effect on 30 April 2026. It applies to all RICS members and regulated firms undertaking commercial property valuations worldwide. The critical shift is that ESG factors — including physical climate hazards such as flooding — move from advisory guidance to mandatory requirements [2].

Valuers must now "actively investigate, evidence and report on ESG factors where these are significant to the valuation." Flood risk is explicitly captured within this obligation. The standard is embedded in the RICS Red Book Global Standards and aligns with International Valuation Standards (IVS), meaning flood resilience sits within the core valuation framework rather than in peripheral commentary [2].

A professional summary of the new standard published in 2026 makes the practical implication clear: physical climate risk is moving from an ESG appendix into mandatory valuation analysis. It must form part of the core valuation reasoning, not an optional addendum [3].

Minimum Expectations for Valuers Under the 2026 Standard

The same professional guidance sets out minimum expectations for valuers assessing climate risk, including flooding [3]:

| Requirement | Detail |

|---|---|

| Recognised climate data providers | Use of sources such as Munich Re, Moody's, or XDI |

| Evidence of mitigation and resilience measures | Document existing flood-resilience interventions at the property |

| Exposure assessment to 2050 | Evaluate how risk profile changes under future climate scenarios |

| Planned adaptation CapEx | Consider capital expenditure planned or required for future resilience |

These are not aspirational benchmarks. From 30 April 2026, they represent the professional floor for any RICS-regulated valuer working on a commercial property where flood risk is a material factor.

Incorporating EA Flood Data: The RICS October 2025 Insight Paper

The mandatory ESG standard does not stand alone. It is reinforced by the most specific RICS document on flooding and valuation currently in circulation: the RICS insight paper "Flooding and its implications for property professionals", published in October 2025 [5].

This paper is essential reading for any surveyor conducting valuation surveys for flood-resilient properties under the 2026 RICS adjustments post-EA updates framework. It sets out a clear data hierarchy for flood risk assessment.

Standard Data Inputs for Flood Risk Assessment

The October 2025 paper instructs surveyors and valuers to use the following as standard data inputs when assessing flood risk [6]:

- Environment Agency (EA) flood maps — the primary spatial reference for flood zone classification in England

- Climate-change allowances — EA guidance on how flood risk is projected to change over the lifetime of a building

- Local flood authority information — data held by Lead Local Flood Authorities (LLFAs) on surface water, groundwater, and ordinary watercourse flooding

- Insurance data and claims history — where available, to evidence actual flood exposure

The integration of EA flood maps is particularly significant. The EA updates its flood mapping data on a rolling basis, and the 2025 paper makes explicit that valuers should use the most current available data rather than relying on historic flood zone classifications that may no longer reflect actual risk profiles [6].

For surveyors working in areas where the EA has recently updated its flood modelling — particularly in catchments affected by recent flood events — this means actively checking for revised flood zone boundaries before completing a valuation report. A property that was in Flood Zone 2 under older mapping may now sit in Flood Zone 3, with material implications for value, insurability, and mortgage availability.

Understanding the full scope of a property's condition is also important in this context. A RICS Level 3 Building Survey provides the depth of structural investigation needed to identify flood-related damage, resilience installations, and material condition issues that a standard valuation inspection alone might not capture.

How Flood-Resilience Measures Affect Market Value

The central question for any valuer working on a flood-risk property is not simply "is this property at risk?" but "how does the installed resilience affect its value, insurability, and functional obsolescence?"

The RICS October 2025 insight paper addresses this directly. It states that flood-resilience and resistance measures can materially affect repair cost, insurability, and functional obsolescence, and should therefore be considered by valuers when forming an opinion of value for at-risk properties [6].

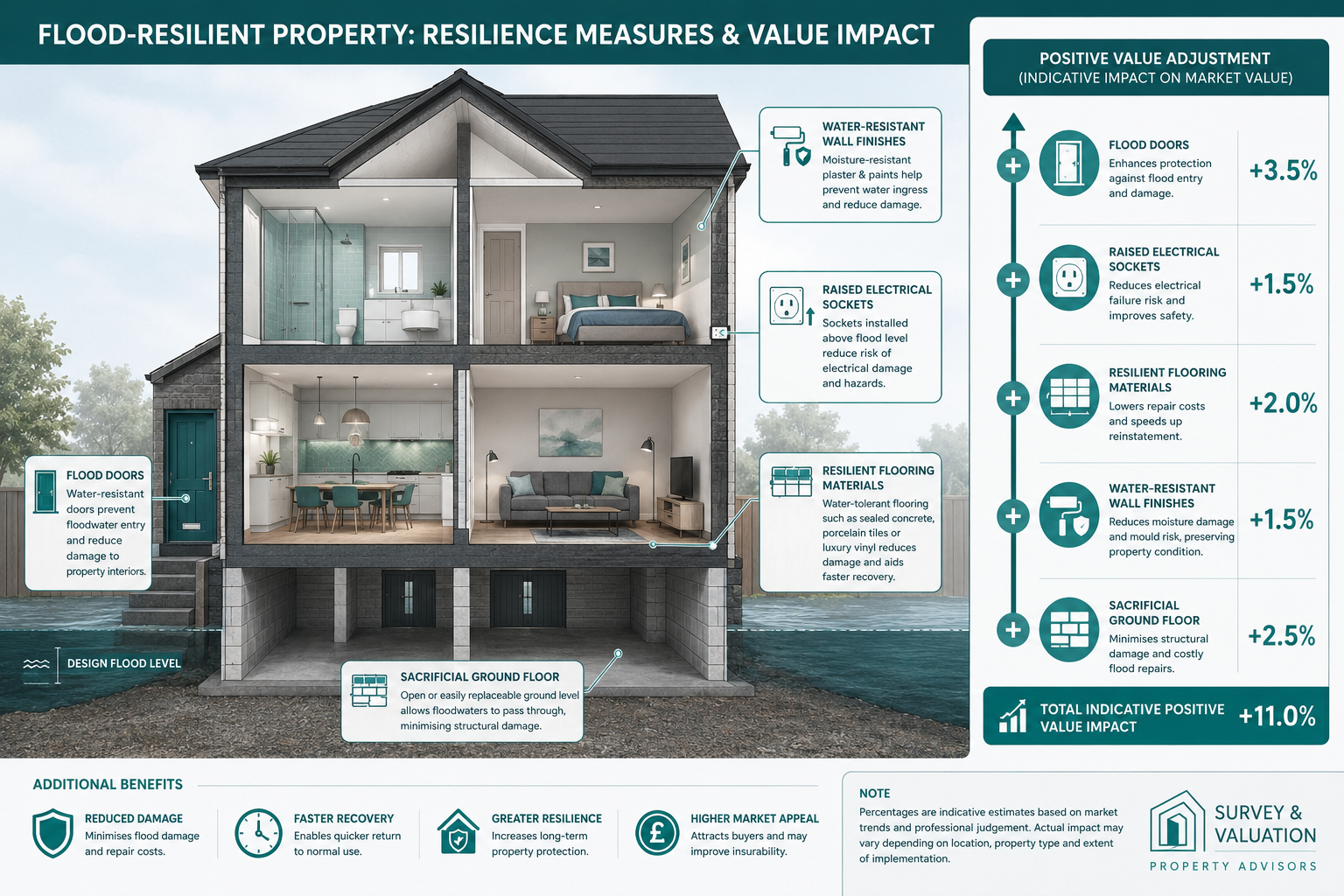

Categories of Flood-Resilience Measures

Resilience measures fall into two broad categories, both of which carry valuation implications:

Flood Resistance Measures (designed to keep water out):

- Flood doors and flood gates

- Demountable barriers

- Air brick covers

- Non-return valves on drainage systems

Flood Resilience Measures (designed to reduce damage when water enters):

- Raised electrical sockets and consumer units

- Resilient flooring materials (e.g. concrete, ceramic tile)

- Water-resistant wall finishes and plasterboard

- Sacrificial ground floors designed for easy replacement

- Raised kitchen and bathroom units

Each of these has a direct bearing on the cost of reinstatement following a flood event. A property with raised electrics and resilient finishes will cost significantly less to repair after inundation than an equivalent property with standard fittings. This differential in repair cost feeds directly into insurance premiums, the availability of cover, and ultimately into market value.

For properties where reinstatement cost is a key valuation input — particularly for insurance purposes — a dedicated insurance reinstatement valuation will need to account for these resilience features explicitly. Similarly, a reinstatement cost valuation must reflect the reduced reinstatement liability that properly installed resilience measures can deliver.

The Value Premium for Resilience

Market evidence on flood-resilience premiums is still developing, but the direction of travel is clear. Properties in high flood-risk areas that have invested in accredited resilience measures — particularly those meeting the PAS 1188 standard for flood-resilience products — are increasingly achieving better mortgage terms, lower insurance premiums, and stronger buyer confidence than comparable unprotected properties.

The UNEP FI has noted that physical climate risk, including flood exposure, is increasingly being priced into real estate values as data availability improves and institutional investors apply more rigorous climate screening [7]. The 2026 RICS mandatory standard accelerates this pricing mechanism by requiring valuers to make the evidence base explicit.

"Flood-resilience interventions are now expected to be explicitly captured as value-relevant factors in standard valuation reports for affected assets." — Professional summary of the 2026 RICS ESG standard [3]

Practical Steps for Surveyors: Conducting Valuation Surveys Post-EA Updates

Translating the new requirements into day-to-day survey practice requires a structured approach. The following framework reflects the combined requirements of the 2026 RICS ESG standard and the October 2025 RICS flooding insight paper.

Step 1: Pre-Inspection Data Gathering

Before visiting the property, surveyors should compile:

- Current EA flood zone classification (Flood Zone 1, 2, or 3) using the live EA flood map for planning

- EA climate-change allowances applicable to the relevant watercourse or surface water source

- Local flood authority records for surface water and groundwater risk

- Any available flood history for the specific address

- Insurance market data, including Flood Re eligibility where applicable

This pre-inspection data gathering is not optional under the 2026 framework. It forms the evidential foundation that the valuation report must reference.

Step 2: On-Site Inspection of Resilience Measures

During the physical inspection, the surveyor should systematically record:

- The presence, type, and apparent condition of any flood-resistance installations

- Evidence of flood-resilience measures (raised electrics, resilient materials, etc.)

- Any signs of previous flood damage and the quality of subsequent reinstatement

- Drainage condition and the risk of surface water ingress

For properties where drainage condition is a concern, a professional drainage survey can provide the detailed evidence needed to assess the risk of drainage-related flooding and the effectiveness of any installed non-return valve systems.

Where damp or moisture penetration is evident — which may indicate historic flood ingress or ongoing water management issues — a damp survey will provide the technical data needed to distinguish between condensation, rising damp, and flood-related moisture.

Step 3: Valuation Methodology Adjustments

The valuation methodology must now explicitly address flood risk and resilience. Key adjustments include:

- Comparable selection: Where possible, use comparables that share a similar flood-risk profile. Where no direct comparables exist, apply a transparent adjustment with documented rationale.

- Depreciation for unmitigated risk: Properties in Flood Zone 3 without resilience measures should reflect a depreciation that accounts for higher insurance costs, reduced mortgage availability, and functional obsolescence risk.

- Premium for accredited resilience: Where resilience measures meet recognised standards (e.g. PAS 1188), this should be evidenced and reflected positively in the valuation.

- Adaptation CapEx: Where resilience measures are absent but the property is in a high-risk zone, the cost of installing appropriate measures should be considered as a deduction from gross value.

Step 4: Reporting Requirements

The valuation report must now include a dedicated section on physical climate risk where flood risk is material. This section should:

- Identify the data sources used (EA flood maps, climate-change allowances, recognised climate data providers)

- Describe the flood-risk profile of the property under current and 2050 climate scenarios

- Document all resilience measures identified during inspection

- Explain how flood risk and resilience have been reflected in the valuation figure

- Flag any limitations in the available data

For commercial properties, this reporting obligation is now mandatory under the 2026 RICS ESG standard [2]. For residential properties, the October 2025 RICS insight paper makes clear that the same analytical rigour is expected, even where the formal mandatory standard applies primarily to commercial valuations [6].

Surveyors who are uncertain about the appropriate survey type for a given property — particularly where flood risk intersects with other structural concerns — will find it useful to review the different types of survey comparison to ensure the right level of investigation is commissioned.

Valuation Surveys for Flood-Resilient Properties: 2026 RICS Adjustments and the Broader Professional Landscape

The 2026 adjustments do not exist in isolation. They reflect a broader shift in how the property profession is being asked to engage with climate risk — one that has implications beyond individual valuation reports.

Implications for Lenders and Mortgage Valuations

Mortgage lenders are increasingly scrutinising flood risk as part of their lending decisions. The mandatory RICS requirement to evidence flood risk and resilience in valuation reports will generate more consistent and comparable data for lenders, which is likely to accelerate the differentiation of mortgage terms between flood-resilient and non-resilient properties in high-risk zones.

Valuers conducting mortgage valuations on properties in Flood Zone 2 or 3 should expect lenders to ask specific questions about resilience measures and insurance availability. The ability to provide a clear, evidenced answer — grounded in the EA data and RICS methodology described above — will become a standard professional expectation.

Implications for Commercial Property Portfolios

For commercial property portfolios, the mandatory ESG standard creates a direct reporting obligation. Asset managers and their appointed valuers must now ensure that physical climate risk — including flood exposure — is captured in the main body of valuation analysis, not relegated to an appendix [3].

This has particular relevance for portfolio valuations where multiple properties in flood-risk areas are assessed simultaneously. A commercial building survey provides the structural and condition data that underpins a robust flood-risk assessment for commercial assets, ensuring that resilience measures are properly identified and evidenced before the valuation is prepared.

Monitoring and Ongoing Compliance

Flood risk is not static. EA flood maps are updated, climate-change allowances are revised, and the condition of resilience measures deteriorates over time. Surveyors advising property owners in high-risk areas should consider recommending periodic monitoring surveys to track changes in structural condition and the ongoing effectiveness of installed resilience measures.

Conclusion

The 2026 RICS adjustments post-EA updates represent the most significant change to flood risk valuation practice in a generation. For surveyors, the message is unambiguous: physical climate risk, including flood exposure and the resilience measures installed to counter it, must now be treated as a core component of valuation analysis — not an optional extra.

Actionable next steps for surveyors:

- Update your pre-inspection data workflow to include live EA flood map checks, climate-change allowances, and local flood authority records as standard for all properties in Flood Zones 2 and 3.

- Develop a resilience measure checklist for on-site inspections that captures the type, condition, and accreditation status of all flood-resistance and flood-resilience installations.

- Review your comparable selection methodology to ensure flood-risk profile is treated as a material comparability factor, with transparent adjustments documented where direct comparables are unavailable.

- Ensure your valuation reports include a dedicated physical climate risk section for all properties where flood risk is material, referencing the data sources used and explaining how resilience measures have been reflected in the valuation figure.

- Stay current with EA flood map updates for your operating area, particularly in catchments where recent flood events may have triggered revised flood zone boundaries.

- Commission specialist surveys where needed — a RICS building survey or drainage survey can provide the technical depth required to support a robust flood-risk valuation on complex or high-value properties.

The properties that will hold value in a changing climate are those where resilience has been invested in and properly evidenced. The surveyors who will serve their clients best are those who can assess, document, and communicate that resilience clearly — and the 2026 RICS framework gives them the professional mandate to do exactly that.

References

[2] Rics Update The New Standard For Esg In Commercial Property Valuation – https://utopi.co.uk/news-and-insights/rics-update-the-new-standard-for-esg-in-commercial-property-valuation/

[3] Sophie Taysom Real Asset Resilience Is No Longer Strategic Activity 7430523137479446528 By3u – https://www.linkedin.com/posts/sophie-taysom_real-asset-resilience-is-no-longer-strategic-activity-7430523137479446528-by3U

[5] Rics Releases New Insight Paper Flooding Property – https://www.rics.org/news-insights/rics-releases-new-insight-paper-flooding-property

[6] Flooding And Its Implications For Property Professionals October 2025 – https://www.rics.org/content/dam/ricsglobal/documents/research/Flooding-and-its-implications-for-property-professionals-October-2025.pdf

[7] Climate Risk And Real Estate Value Aug2021 – https://www.unepfi.org/wordpress/wp-content/uploads/2021/08/Climate-risk-and-real-estate-value_Aug2021.pdf

[8] Flooding And Its Implications For Property Professionals – https://www.rics.org/news-insights/research-and-insights/flooding-and-its-implications-for-property-professionals