Residential property investors who relied on a single valuation method lost an average of 12–18% on distressed disposals during the last major UK market correction — not because the numbers were wrong, but because they were incomplete. In Q2 2026, with transaction volumes recovering and rental demand sustaining elevated gross yields in many commuter zones, the discipline of cross-checking yield vs comparable valuation methods has never been more commercially critical. This guide breaks down how surveyors structure blended approaches, what checklists they use to stress-test assumptions, and how investors can apply the same rigour to residential investment sanity checks.

Key Takeaways 📌

- Never rely on a single method. Comparable and yield approaches answer different questions; reconciling both produces a defensible valuation.

- Gross yield is a headline figure only. Net yield and cap rate — anchored in comparable evidence — are the metrics that actually protect investment decisions.

- At least three quality comparables are the professional standard for a defensible sales-comparison valuation.

- Surveyor checklists follow a structured sequence: subject property data → market data → environmental context → highest-and-best-use → method selection → reconciliation.

- Q2 2026 market conditions (rising rents, cautious lending) make stress-testing both income assumptions and comparable adjustments essential before committing capital.

Understanding the Two Core Valuation Approaches

Before building any checklist, it helps to be precise about what each method actually measures. The methods of valuation used by chartered surveyors broadly fall into five recognised categories, but for residential investment property, two dominate day-to-day practice.

The Comparable (Sales Comparison) Method

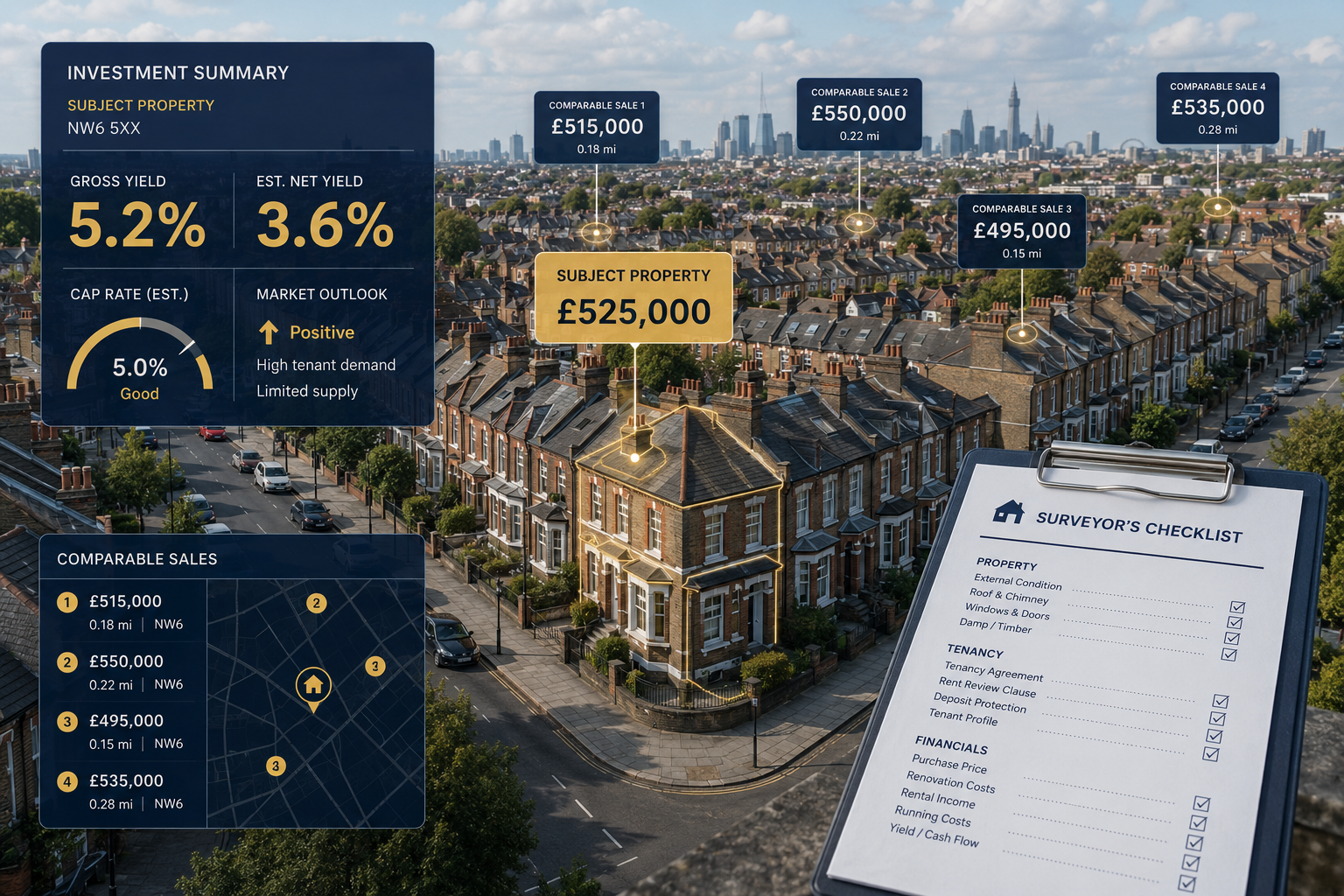

The comparable method estimates value by analysing recent sales of similar properties and adjusting for differences. It is the primary benchmark for residential and small residential investment properties because it directly reflects what the market has actually paid [2][7].

Key mechanics:

- Identify three or more recent, arm's-length transactions of similar properties

- Adjust for differences in size, condition, location, tenure, and specification

- Derive an adjusted price per square foot or per unit

- Apply to the subject property

💬 "At least three good-quality comparables are typically required for a defensible sales-comparison valuation, to avoid over-reliance on outliers." [2]

The strength of this method is its market-anchored objectivity. Its weakness is that it can lag in fast-moving markets and becomes unreliable where transaction evidence is thin — a common problem in niche micro-markets or for unusual property types.

The Yield (Income Capitalisation) Method

The income approach estimates value based on the income a property generates, using the formula:

V = NOI ÷ Cap Rate

Where:

- V = estimated value

- NOI = Net Operating Income (annual rent minus operating costs)

- Cap Rate = capitalisation rate derived from comparable investment transactions [3][5]

This method is most powerful where a well-developed rental investment market exists and where yield evidence from comparable sales is available [2]. For residential investment, it functions as a cross-check rather than a primary driver, unless the property is a purpose-built rental block or HMO.

| Feature | Comparable Method | Yield / Income Method |

|---|---|---|

| Primary use | Owner-occupied & investment | Investment / income-producing |

| Data required | Recent sales comparables | Rental income + cap rate evidence |

| Strength | Market-reflective | Income-focused |

| Weakness | Lags in thin markets | Sensitive to cap rate assumptions |

| Role in residential | Primary | Cross-check / sanity test |

Surveyor Checklists for Residential Investment Sanity Checks: The Structured Framework

Professional surveyors do not simply pick a method and run numbers. RICS-aligned frameworks require a structured sequence of data gathering and analysis before any valuation method is applied [8]. Understanding this sequence is what separates a robust investment sanity check from a back-of-envelope calculation.

Stage 1: Subject Property Data Collection ✅

Before touching a comparable or a yield figure, surveyors document the subject property in full. This stage is non-negotiable.

Checklist — Subject Property:

- Full address, tenure (freehold/leasehold), and unexpired lease term

- Gross internal area (GIA) and net internal area (NIA) measured to RICS standards

- Physical condition and construction type (note any structural concerns — see residential structural engineering surveys)

- Current occupancy status and tenancy details (rent passing, lease expiry, break clauses)

- Planning history and any restrictions on use

- Service charge and ground rent liability (critical for leasehold — see lease extension valuation)

- EPC rating and any compliance obligations

⚠️ Red flag: A leasehold property with fewer than 80 years remaining will attract a marriage value premium in any lease extension negotiation, materially affecting both yield and comparable evidence.

Stage 2: Market Data — Comparables and Yield Evidence

This is where the yield vs comparable valuation methods discipline becomes most demanding. Surveyors must gather both datasets simultaneously, not sequentially.

Comparable Sales Checklist:

- Minimum three arm's-length sales within the last 12 months (24 months in thin markets)

- Transactions within a defined radius (typically 0.5–1 mile for urban residential)

- Adjustments documented for: size, floor level, condition, parking, garden, specification

- Source verified (Land Registry, agent evidence, auction results)

- Any distressed or non-arm's-length sales flagged and excluded or heavily adjusted

Yield Evidence Checklist:

- Current market rent (CMR) established from letting agent evidence and comparable lettings

- Gross yield calculated: (Annual Rent ÷ Purchase Price) × 100

- Net yield calculated after: management fees (typically 10–15%), maintenance allowance (1–2% of value), voids allowance (4–8 weeks per year), insurance, ground rent/service charge

- Cap rate cross-referenced against comparable investment sales in the same sub-market [5][6]

- Stress-tested at +1% cap rate to model downside scenario

Stage 3: Environmental and Governmental Context 🌍

Surveyors are expected to consider factors beyond the property itself [8]. In Q2 2026, several macro-level factors are directly affecting both yield assumptions and comparable evidence in UK residential markets:

- Renters' Rights Act implications on void periods and rent review mechanisms

- EPC upgrade requirements and their cost impact on net yield

- Local authority licensing for HMOs and selective licensing zones

- Flood risk and ground stability (relevant to subsidence surveys)

- Infrastructure projects affecting local demand (HS2 ripple effects, Crossrail extension zones)

Stage 4: Highest and Best Use Conclusion

Before selecting a valuation method, surveyors determine the highest and best use (HBU) of the property — the legally permissible, physically possible, financially feasible, and maximally productive use [4][8].

For residential investment, this often involves asking:

- Is the property better valued as a single let, an HMO, or a serviced apartment?

- Does permitted development allow conversion that would materially change value?

- Is the freehold interest worth more than the sum of the leasehold parts? (See valuing freehold interests)

Applying Yield vs Comparable Valuation Methods: Reconciliation and Stress-Testing in Practice

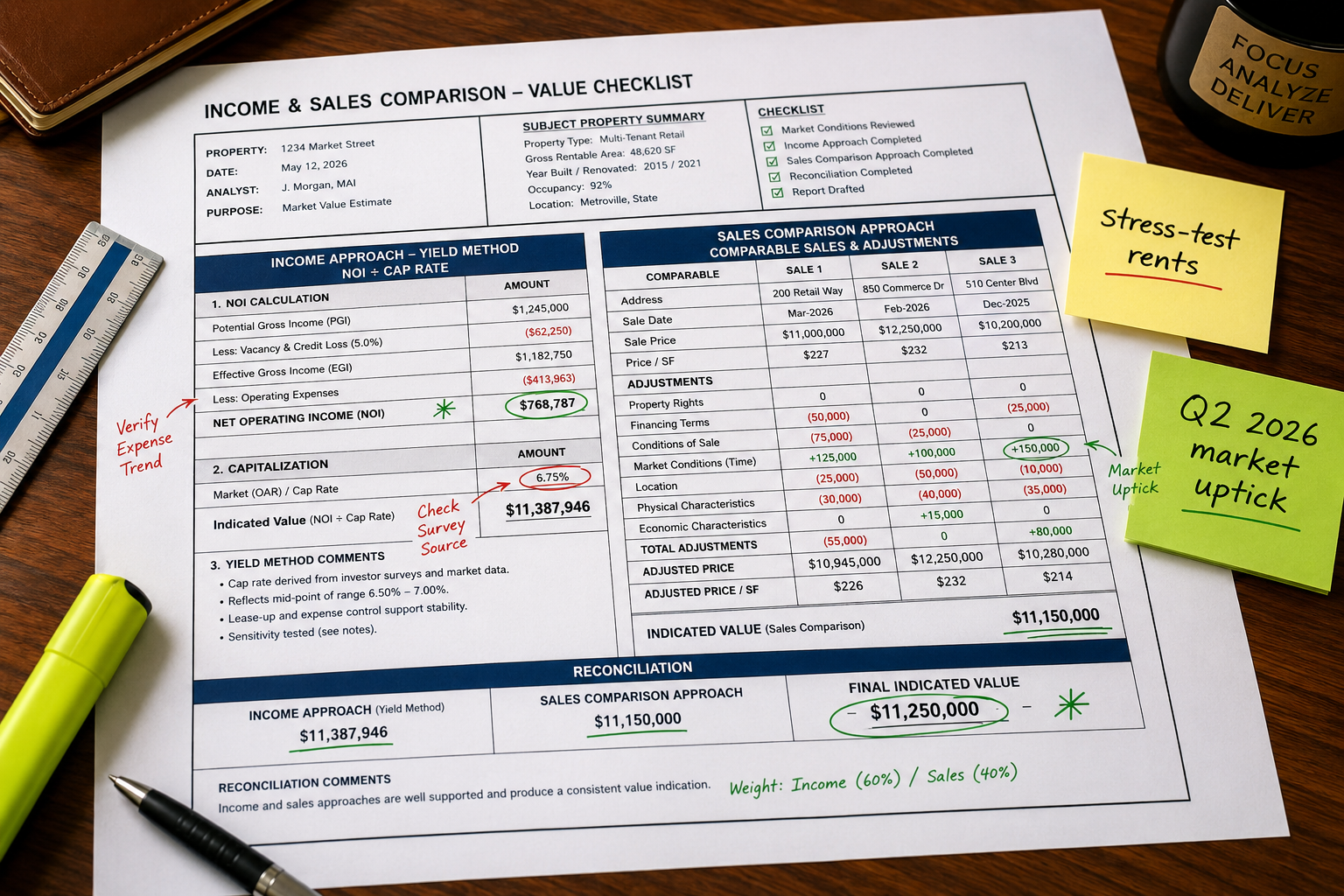

Once data is gathered and HBU is established, the surveyor applies both methods and reconciles the outputs. This reconciliation stage is where investment sanity checks either hold or collapse [2][9].

The Reconciliation Process

Surveyors are expected to explain the weighting given to each method, not simply average the results [2]. The weighting depends on:

- Quality of comparable evidence — if three strong comparables exist within 0.5 miles and 12 months, the comparable method carries more weight

- Stability of rental income — a fully let property with a long lease and a reliable tenant supports higher income method weighting

- Market conditions — in a rising market with thin sales evidence, yield evidence from investment transactions may be more current

Example Reconciliation Table:

| Method | Indicated Value | Weighting | Weighted Value |

|---|---|---|---|

| Comparable (Sales) | £485,000 | 60% | £291,000 |

| Yield / Income | £470,000 | 40% | £188,000 |

| Reconciled Value | 100% | £479,000 |

Stress-Testing Rents and Yields Against Surveyor Conservatism

In a Q2 2026 uptick environment, optimistic rental projections from letting agents can inflate income method valuations. Professional surveyors apply a conservative lens that investors should replicate:

Rent Stress-Test Protocol:

- Use the lower of passing rent and current market rent (CMR) as the base

- Apply a minimum 5% void allowance even for apparently strong markets

- Deduct a maintenance reserve of at least 1% of capital value annually

- Model the impact of a 10% rent reduction on net yield — if the investment only works at peak rents, it fails the sanity check

Cap Rate Stress-Test Protocol:

- Identify the cap rate implied by comparable investment sales [6]

- Apply the income formula at that rate: V = NOI ÷ Cap Rate

- Then re-run at cap rate + 1% (e.g., 5.5% → 6.5%)

- A 1% cap rate expansion on a £500,000 property can reduce indicated value by £75,000–£90,000

💬 "The cap rate itself must be anchored in comparable evidence — not assumed from national averages or marketing materials." [2][5]

Common Errors That Fail the Sanity Check ❌

Understanding the key valuation factors that surveyors weigh helps investors avoid the most common analytical errors:

- Using gross yield as a decision metric — net yield is what matters; gross yield routinely overstates returns by 2–3 percentage points

- Accepting agent-supplied comparables without verification — always cross-reference against Land Registry data

- Ignoring lease length on leasehold flats — a flat with 75 years remaining will trade at a discount to one with 125 years, affecting both comparable adjustments and yield expectations

- Failing to adjust for condition — a comparable that sold following full refurbishment is not directly comparable to a property requiring £30,000 of works

- Treating yield evidence from different property types as interchangeable — HMO yields, single-let yields, and serviced apartment yields operate in different markets

When to Engage a Chartered Surveyor for a Formal Valuation

Not every investment decision requires a full RICS Red Book valuation, but several scenarios make professional input essential:

- Purchase price is materially above comparable evidence and the investor is relying on yield to justify the premium

- Leasehold property where lease length, ground rent, or service charge anomalies exist

- Mixed-use or conversion potential where HBU analysis is complex

- Portfolio acquisition where aggregate pricing masks individual asset mispricing

- Lender-required valuation for mortgage or refinancing purposes

For investors operating across London and the South East, local chartered surveyors with sub-market expertise will have access to comparable evidence and yield data that national platforms cannot replicate. Specialists covering areas such as North London, Surrey, and South West London bring granular market knowledge that strengthens both the comparable and yield legs of any valuation.

Quick-Reference: Surveyor's Residential Investment Valuation Checklist

Use this consolidated checklist as a pre-offer sanity check on any residential investment:

📋 Pre-Offer Residential Investment Sanity Check

Property Fundamentals

- Tenure confirmed (freehold / leasehold / share of freehold)

- Lease length verified (if leasehold, unexpired term noted)

- Floor area measured or verified against title

- Condition assessed (structural survey commissioned if any doubt)

- EPC rating and upgrade cost estimated

Comparable Evidence

- Minimum 3 comparable sales identified and verified via Land Registry

- Adjustments made for size, condition, floor, parking, garden

- Price per sq ft range established for the micro-market

- Subject property positioned within that range with justification

Yield and Income Analysis

- Current market rent established from at least 2 letting agent opinions

- Gross yield calculated

- Net yield calculated (after all deductions)

- Cap rate benchmarked against comparable investment sales

- Income method value calculated (V = NOI ÷ Cap Rate)

- Stress-test run at CMR -10% and Cap Rate +1%

Reconciliation

- Both method outputs compared

- Variance explained (if >5%, investigate further)

- Weighted reconciled value established

- Investment decision tested against reconciled value, not asking price

Conclusion: Actionable Next Steps for Residential Investors in 2026

The discipline of applying yield vs comparable valuation methods with a surveyor's structured checklist is not bureaucratic overhead — it is the mechanism by which serious investors separate genuine opportunities from overpriced assets dressed up with optimistic yield projections.

In Q2 2026, with rents elevated and some comparable evidence still catching up with transaction volumes, the risk of overpaying based on income assumptions alone is real. The antidote is the blended approach: use comparables as the primary anchor, use yield evidence as the cross-check, stress-test both, and reconcile with documented weighting.

Actionable next steps:

- Run the checklist above on every prospective acquisition before submitting an offer — it takes 2–3 hours and can save five-figure mistakes.

- Commission a formal RICS valuation for any purchase where the asking price sits above your comparable-derived range, or where leasehold complexity exists.

- Engage a local chartered surveyor with sub-market comparable data — national AVMs and portal estimates are not a substitute for professional evidence.

- Review your existing portfolio using the net yield and cap rate stress-test protocol — assets that only work at peak assumptions may warrant disposal before the next market shift.

- Stay current on regulatory changes (EPC requirements, licensing, tenancy law) that directly affect net yield calculations in 2026 and beyond.

For specialist valuation support, including formal investment valuations and residential sanity checks, contact Canterbury Surveyors to discuss your specific requirements.

References

[1] Fulltext01 – https://kth.diva-portal.org/smash/get/diva2:475833/FULLTEXT01.pdf

[2] Apc 5 Valuation Methods – https://ww3.rics.org/uk/en/journals/property-journal/apc-5-valuation-methods.html

[3] Real Estate Appraisal Valuation Methods – https://www.dealpath.com/blog/real-estate-appraisal-valuation-methods/

[4] Three Approaches To Value – https://www.citrincooperman.com/In-Focus-Resource-Center/Three-Approaches-to-Value

[5] Commercial Real Estate Valuation Approaches – https://www.jpmorgan.com/insights/real-estate/commercial-real-estate/commercial-real-estate-valuation-approaches

[6] Major Methods Commercial Real Estate Valuation – https://www.altusgroup.com/insights/major-methods-commercial-real-estate-valuation/

[7] Valuing Real Estate – https://www.investopedia.com/articles/mortgages-real-estate/11/valuing-real-estate.asp

[8] Appraisal Process – https://pickensassessor.org/wp-content/uploads/sites/26/2018/07/Appraisal-Process.pdf

[9] Real Estate Valuation Methods – https://www.pricehubble.com/blog/real-estate-valuation-methods