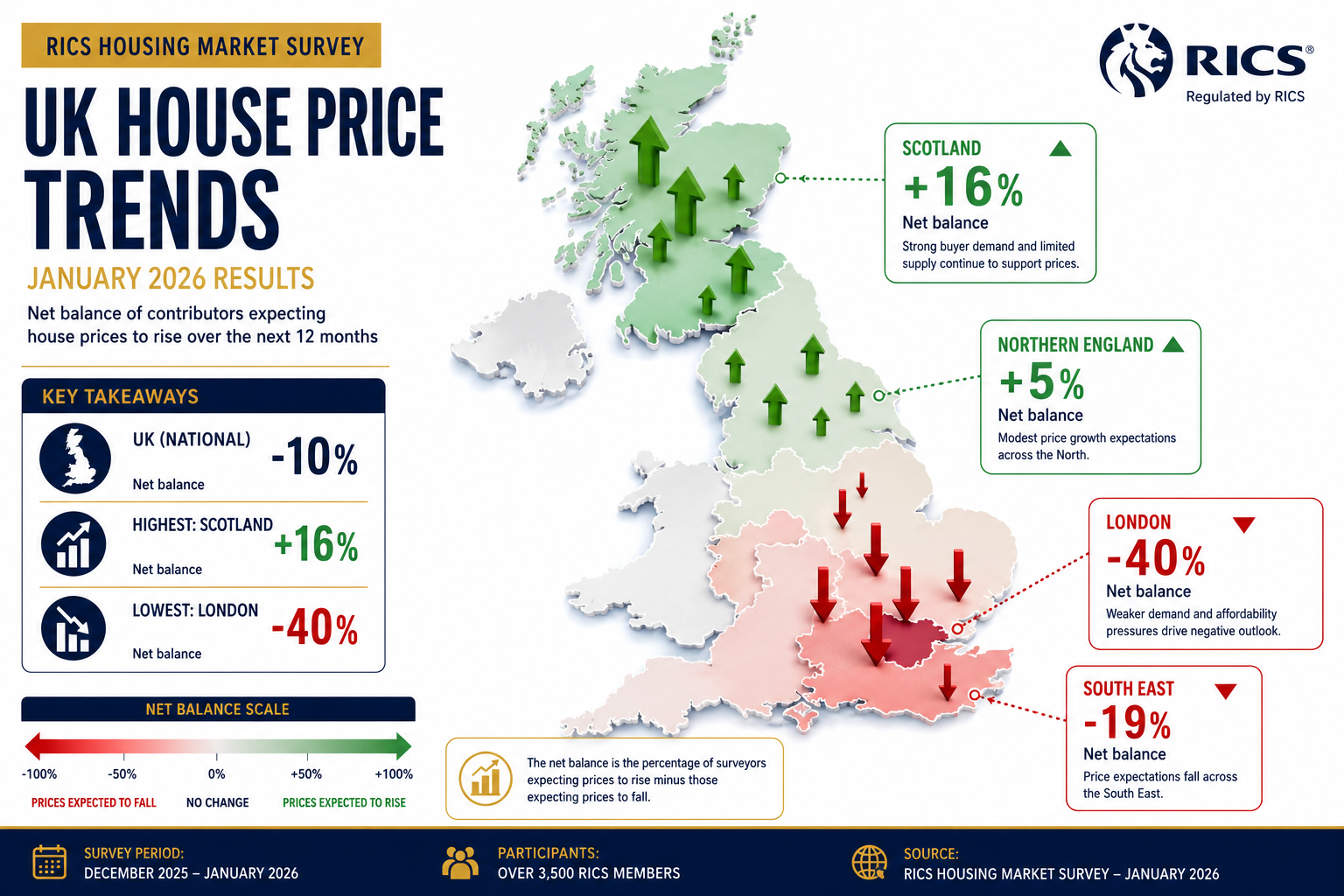

Only -10% net balance — that is where UK house prices now sit according to the latest RICS data, a significant improvement from -19% in October 2025 and a clear signal that the market is shifting beneath surveyors' feet [1]. The RICS January 2026 Market Survey: What UK Building Surveyors and Valuers Really Need to Change in Their Reports is not simply another set of headline statistics to file away. It is a live instruction manual for every chartered surveyor and valuer working in the UK today, demanding concrete updates to assumptions, commentary, and caveats — before the next report lands on a client's desk.

Key Takeaways 📋

- The market is stabilising, not recovering uniformly — surveyors must stop using blanket "declining market" language and adopt region-specific commentary.

- Regional divergence is at its widest in years — London sits at -40% price balance while Scotland and Northern Ireland are in positive territory.

- Buyer enquiries and agreed sales are both improving — valuation reports should reflect rising transactional momentum without overstating confidence.

- The rental market is tightening — buy-to-let valuations need updated yield calculations as tenant demand rises and landlord supply shrinks.

- The 12-month outlook is the most positive since December 2024 — market commentary sections in reports should acknowledge cautious optimism, not doom.

Why the RICS January 2026 Data Demands Immediate Report Updates

Surveyors who wrote reports in Q4 2025 using language calibrated to a falling market may now be misleading clients. The RICS January 2026 Market Survey: What UK Building Surveyors and Valuers Really Need to Change in Their Reports makes that risk concrete.

Consider the trajectory of buyer enquiries. The net balance moved from -29% in November 2025 to -15% in January 2026 — a meaningful improvement that signals more active buyers in the market [3]. Agreed sales reached their least negative reading since June 2025 at -9% [1]. These are not noise; they are trend signals that should directly influence how surveyors frame marketability assessments.

💬 "A report written for yesterday's market can cost a client tens of thousands of pounds in a mispriced transaction."

The problem is institutional inertia. Many surveyors rely on templated commentary blocks that describe "subdued buyer activity" or "ongoing price pressure" — language that was accurate in mid-2025 but is now partially obsolete. The January 2026 data demands a rewrite.

What "Stabilising" Actually Means for Report Language

Stabilisation is not recovery. That distinction matters enormously in professional report writing. A stabilising market means:

- Price declines are slowing, not reversing everywhere

- Transaction volumes are recovering, but remain below long-run averages

- Uncertainty persists, particularly in the short term (+4% net balance for 3-month sales expectations) [3]

Surveyors should replace phrases like "the market continues to experience downward pressure" with more nuanced language such as "the market is showing early signs of stabilisation, with price declines moderating and buyer activity improving, though short-term uncertainty remains."

For clients considering a Level 2 HomeBuyer Survey or a Level 3 Building Survey, this language shift is not cosmetic — it directly affects how they interpret marketability risk and negotiate purchase prices.

The Regional Divide: How the RICS January 2026 Market Survey Changes Localised Valuation Methodology

The most operationally significant finding in the RICS January 2026 Market Survey: What UK Building Surveyors and Valuers Really Need to Change in Their Reports is the widening regional price divergence [4]. This is not a minor variation — it is a structural split that demands fundamentally different valuation approaches depending on geography.

The North-South Divide in Numbers

| Region |

Price Balance (Jan 2026) |

Direction |

| London |

-40% |

⬇️ Strongly negative |

| South East |

-24% |

⬇️ Negative |

| East Anglia |

-26% |

⬇️ Negative |

| Scotland |

Positive |

⬆️ Growing |

| Northern Ireland |

Positive |

⬆️ Growing |

| North West England |

Positive |

⬆️ Growing |

| North of England |

Positive |

⬆️ Growing |

Source: RICS January 2026 Residential Market Survey [4]

This table should be pinned above every valuer's desk in the UK. A surveyor operating in Surrey or West London is working in a fundamentally different market to a colleague in Manchester or Edinburgh — and their reports must reflect that.

Practical Changes for Southern England Surveyors

Southern England markets face persistent affordability challenges [1]. For surveyors working in London, the South East, and East Anglia, the following report adjustments are now essential:

- Comparable evidence weighting — Prioritise comparables from the last 90 days over older transactions; the market has been moving and older data overstates values.

- Affordability caveats — Explicitly note that mortgage affordability constraints continue to suppress demand in high-value areas.

- Days on market commentary — Where properties are sitting longer before sale, this should be quantified and referenced.

- Downward adjustment justification — When applying adjustments to comparables, document the affordability rationale clearly.

Surveyors covering Chelsea, Battersea, or Islington are operating in markets where the -40% London price balance is particularly acute. Generic national commentary in reports from these areas is not just unhelpful — it may constitute a professional shortcoming.

Practical Changes for Northern and Scottish Surveyors

The opposite problem exists in growth regions. Surveyors in Scotland, Northern Ireland, and the North West must guard against under-valuation by:

- Ensuring comparable evidence reflects recent price growth, not historical averages

- Noting positive buyer demand and supply constraints in market commentary

- Avoiding templated "cautious market" language that does not reflect local conditions

Updating Valuation Assumptions: A Section-by-Section Guide for 2026 Reports

The RICS January 2026 Market Survey: What UK Building Surveyors and Valuers Really Need to Change in Their Reports provides enough data to justify specific updates across multiple sections of a standard valuation or building survey report. Here is a structured breakdown.

1. Market Commentary Section

Old approach (2025): Describe a declining market with subdued buyer activity and falling prices.

New approach (2026): Acknowledge the improvement trajectory. Key data points to reference:

- Buyer enquiries net balance improved to -15% (from -29% in November 2025) [3]

- 12-month sales outlook at +35%, the strongest since December 2024 [1]

- 43% of respondents anticipate higher prices over the year ahead [1]

However, balance this with short-term caution: the 3-month sales expectation sits at only +4% net balance [3], indicating the recovery is not yet entrenched.

2. Comparable Evidence and Price Adjustment Section

New instructions to follow:

- 🗓️ Date-weight your comparables — transactions from Q4 2025 may reflect a more negative market than currently exists; apply appropriate adjustments.

- 📍 Hyper-localise your evidence — national averages are misleading given the regional divide; use sub-regional or even postcode-level data where possible.

- 📊 Note the direction of travel — RICS guidance supports commentary on whether the market is rising, falling, or stabilising at the point of inspection.

For properties requiring a structural survey alongside valuation, condition findings should be cross-referenced with local marketability — a property with structural issues in a strong northern market may still achieve a good price; the same property in a weak London market faces compounded risk.

3. Marketability and Saleability Commentary

This is where the January 2026 data has the most direct impact. Surveyors should now:

- Replace "limited buyer pool" language in strong northern markets with acknowledgement of competitive demand

- Retain affordability risk commentary in London and South East reports

- Note the improving new instructions balance (+1% net) [3] — supply remains constrained, which supports values even in softer markets

4. Buy-to-Let and Investment Property Valuations

The rental market data from the January 2026 survey demands specific updates to investment property reports:

- Tenant demand improved to +13% in the three months to January, ending two consecutive quarters of flat or negative readings [3]

- Landlord instructions remain constrained at -24% [3] — a supply-demand imbalance that supports rental values

- 28% of respondents expect rental prices to rise in the near term, up from 16% previously [3]

For surveyors preparing valuations on buy-to-let properties, rental yield calculations based on 2025 rental data may now understate current and forward rental values. Reports should explicitly note this upward rental pressure and its implications for investment returns.

This is particularly relevant for commercial property surveyors and those handling mixed-use valuations where residential rental income forms part of the yield calculation.

5. Caveats and Limitations Section

Every valuation report should now include a calibrated caveat that reflects the current market environment. A suggested framework:

"This valuation has been prepared in a market showing early signs of stabilisation following a period of price adjustment. Regional conditions vary significantly, and the figures above reflect conditions specific to [location] as at the date of inspection. Short-term economic uncertainty persists; the 12-month outlook is more positive, with 43% of RICS survey respondents anticipating price growth nationally. Clients should seek updated advice before exchanging contracts if more than 90 days have elapsed since this report was prepared."

The Outlook Section: Communicating Cautious Optimism Without Overpromising

One of the most common failures in surveyor reports is the binary treatment of market outlook — either doom-laden caution or uncritical optimism. The January 2026 data supports neither extreme.

The 12-month sales outlook at +35% is genuinely encouraging [1]. So is the fact that 43% of respondents anticipate higher prices [1]. But the +4% net balance for 3-month sales expectations [3] is a clear reminder that the near-term picture remains uncertain.

Surveyors should communicate this nuance explicitly. Clients making decisions based on a 12-month horizon can be more confident than those transacting in the next quarter. That distinction belongs in the report.

For clients in areas like Hertfordshire, Buckinghamshire, or Hampshire — markets that sit between the strongly negative London picture and the more positive northern markets — this balanced outlook commentary is especially important. These commuter-belt areas are sensitive to both London affordability spillover and mortgage rate movements, and reports should acknowledge both factors.

Common Mistakes Surveyors Must Stop Making in 2026 Reports

Based on the January 2026 survey data, here are the most critical errors to eliminate:

❌ Using national averages to describe local markets — The -10% national price balance is meaningless in a London borough at -40% or a Scottish city in positive territory.

❌ Copying Q3/Q4 2025 market commentary — The market has moved. Templated language from six months ago is now inaccurate.

❌ Ignoring rental market dynamics in investment valuations — With tenant demand at +13% and landlord supply at -24%, rental yield assumptions need updating [3].

❌ Failing to date-weight comparable evidence — Transactions from mid-2025 reflect a more negative market; applying them without adjustment understates current values in recovering areas.

❌ Omitting a forward-looking caveat — The 90-day validity window for valuations has never been more important to communicate clearly.

✅ Do: Use RICS survey data as a named source in market commentary sections — it demonstrates professional rigour and gives clients confidence in the analysis.

Conclusion: Actionable Next Steps for UK Surveyors and Valuers

The RICS January 2026 Market Survey: What UK Building Surveyors and Valuers Really Need to Change in Their Reports is not background reading — it is a professional obligation. The data is clear, the regional divergence is stark, and the direction of travel is improving. Reports that fail to reflect this are not just outdated; they risk misleading clients at a critical moment in the market cycle.

Here are the immediate actions every UK surveyor should take:

- ✅ Audit your report templates — Remove blanket declining-market language and replace with region-specific, data-referenced commentary.

- ✅ Update your comparable evidence protocols — Apply date-weighting to Q3/Q4 2025 transactions and prioritise recent sales.

- ✅ Revise rental yield assumptions — For buy-to-let and investment properties, recalculate yields using current rental demand data.

- ✅ Add a structured market outlook caveat — Reference the 12-month positive outlook alongside the short-term uncertainty.

- ✅ Localise everything — If your report could apply to any region of the UK, it is not good enough. Every market commentary must be postcode-specific.

Whether conducting a Level 2 HomeBuyer Survey, a full Level 3 Building Survey, or a specialist commercial building survey, the quality of market commentary is now a differentiator. Clients are more informed than ever, and the RICS January 2026 data gives every surveyor the tools to serve them better.

The market is changing. The reports must change with it.

References

[1] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] tradingeconomics – https://tradingeconomics.com/united-kingdom/rics-house-price-balance/news/525158

[3] Uk Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[4] Latest Rics Survey Reveals Global Headwinds Are Weighing On Housing Market Confidence – https://www.buyassociationgroup.com/en-gb/news/latest-rics-survey-reveals-global-headwinds-are-weighing-on-housing-market-confidence/

[5] Rics January 2026 Survey Insights Building Survey Strategies For Stabilising House Prices And Regional Divides – https://wimbledonsurveyors.com/rics-january-2026-survey-insights-building-survey-strategies-for-stabilising-house-prices-and-regional-divides/

[6] Market View January 2026 – https://www.watsons-property.co.uk/market-view-january-2026/

[7] Valuation Strategies Amid January 2026 Rics Residential Survey Spotting Early Market Recovery Signals – https://nottinghillsurveyors.com/blog/valuation-strategies-amid-january-2026-rics-residential-survey-spotting-early-market-recovery-signals

[9] Rics January 2026 Residential Survey Insights Implications For Valuation Surveyors In A Stabilising Market – https://manchestersurveyors.com/rics-january-2026-residential-survey-insights-implications-for-valuation-surveyors-in-a-stabilising-market/

[10] Rics January 2026 Residential Survey Insights Valuation Strategies For Widening North South Price Gaps – https://princesurveyors.co.uk/blog/rics-january-2026-residential-survey-insights-valuation-strategies-for-widening-north-south-price-gaps/

RICS January 2026 Market Survey: What UK Building Surveyors and Valuers Really Need to Change in Their Reports

// Categories

Only -10% net balance — that is where UK house prices now sit according to the latest RICS data, a significant improvement from -19% in October 2025 and a clear signal that the market is shifting beneath surveyors' feet [1]. The RICS January 2026 Market Survey: What UK Building Surveyors and Valuers Really Need to Change in Their Reports is not simply another set of headline statistics to file away. It is a live instruction manual for every chartered surveyor and valuer working in the UK today, demanding concrete updates to assumptions, commentary, and caveats — before the next report lands on a client's desk.

Key Takeaways 📋

Why the RICS January 2026 Data Demands Immediate Report Updates

Surveyors who wrote reports in Q4 2025 using language calibrated to a falling market may now be misleading clients. The RICS January 2026 Market Survey: What UK Building Surveyors and Valuers Really Need to Change in Their Reports makes that risk concrete.

Consider the trajectory of buyer enquiries. The net balance moved from -29% in November 2025 to -15% in January 2026 — a meaningful improvement that signals more active buyers in the market [3]. Agreed sales reached their least negative reading since June 2025 at -9% [1]. These are not noise; they are trend signals that should directly influence how surveyors frame marketability assessments.

The problem is institutional inertia. Many surveyors rely on templated commentary blocks that describe "subdued buyer activity" or "ongoing price pressure" — language that was accurate in mid-2025 but is now partially obsolete. The January 2026 data demands a rewrite.

What "Stabilising" Actually Means for Report Language

Stabilisation is not recovery. That distinction matters enormously in professional report writing. A stabilising market means:

Surveyors should replace phrases like "the market continues to experience downward pressure" with more nuanced language such as "the market is showing early signs of stabilisation, with price declines moderating and buyer activity improving, though short-term uncertainty remains."

For clients considering a Level 2 HomeBuyer Survey or a Level 3 Building Survey, this language shift is not cosmetic — it directly affects how they interpret marketability risk and negotiate purchase prices.

The Regional Divide: How the RICS January 2026 Market Survey Changes Localised Valuation Methodology

The most operationally significant finding in the RICS January 2026 Market Survey: What UK Building Surveyors and Valuers Really Need to Change in Their Reports is the widening regional price divergence [4]. This is not a minor variation — it is a structural split that demands fundamentally different valuation approaches depending on geography.

The North-South Divide in Numbers

Source: RICS January 2026 Residential Market Survey [4]

This table should be pinned above every valuer's desk in the UK. A surveyor operating in Surrey or West London is working in a fundamentally different market to a colleague in Manchester or Edinburgh — and their reports must reflect that.

Practical Changes for Southern England Surveyors

Southern England markets face persistent affordability challenges [1]. For surveyors working in London, the South East, and East Anglia, the following report adjustments are now essential:

Surveyors covering Chelsea, Battersea, or Islington are operating in markets where the -40% London price balance is particularly acute. Generic national commentary in reports from these areas is not just unhelpful — it may constitute a professional shortcoming.

Practical Changes for Northern and Scottish Surveyors

The opposite problem exists in growth regions. Surveyors in Scotland, Northern Ireland, and the North West must guard against under-valuation by:

Updating Valuation Assumptions: A Section-by-Section Guide for 2026 Reports

The RICS January 2026 Market Survey: What UK Building Surveyors and Valuers Really Need to Change in Their Reports provides enough data to justify specific updates across multiple sections of a standard valuation or building survey report. Here is a structured breakdown.

1. Market Commentary Section

Old approach (2025): Describe a declining market with subdued buyer activity and falling prices.

New approach (2026): Acknowledge the improvement trajectory. Key data points to reference:

However, balance this with short-term caution: the 3-month sales expectation sits at only +4% net balance [3], indicating the recovery is not yet entrenched.

2. Comparable Evidence and Price Adjustment Section

New instructions to follow:

For properties requiring a structural survey alongside valuation, condition findings should be cross-referenced with local marketability — a property with structural issues in a strong northern market may still achieve a good price; the same property in a weak London market faces compounded risk.

3. Marketability and Saleability Commentary

This is where the January 2026 data has the most direct impact. Surveyors should now:

4. Buy-to-Let and Investment Property Valuations

The rental market data from the January 2026 survey demands specific updates to investment property reports:

For surveyors preparing valuations on buy-to-let properties, rental yield calculations based on 2025 rental data may now understate current and forward rental values. Reports should explicitly note this upward rental pressure and its implications for investment returns.

This is particularly relevant for commercial property surveyors and those handling mixed-use valuations where residential rental income forms part of the yield calculation.

5. Caveats and Limitations Section

Every valuation report should now include a calibrated caveat that reflects the current market environment. A suggested framework:

The Outlook Section: Communicating Cautious Optimism Without Overpromising

One of the most common failures in surveyor reports is the binary treatment of market outlook — either doom-laden caution or uncritical optimism. The January 2026 data supports neither extreme.

The 12-month sales outlook at +35% is genuinely encouraging [1]. So is the fact that 43% of respondents anticipate higher prices [1]. But the +4% net balance for 3-month sales expectations [3] is a clear reminder that the near-term picture remains uncertain.

Surveyors should communicate this nuance explicitly. Clients making decisions based on a 12-month horizon can be more confident than those transacting in the next quarter. That distinction belongs in the report.

For clients in areas like Hertfordshire, Buckinghamshire, or Hampshire — markets that sit between the strongly negative London picture and the more positive northern markets — this balanced outlook commentary is especially important. These commuter-belt areas are sensitive to both London affordability spillover and mortgage rate movements, and reports should acknowledge both factors.

Common Mistakes Surveyors Must Stop Making in 2026 Reports

Based on the January 2026 survey data, here are the most critical errors to eliminate:

❌ Using national averages to describe local markets — The -10% national price balance is meaningless in a London borough at -40% or a Scottish city in positive territory.

❌ Copying Q3/Q4 2025 market commentary — The market has moved. Templated language from six months ago is now inaccurate.

❌ Ignoring rental market dynamics in investment valuations — With tenant demand at +13% and landlord supply at -24%, rental yield assumptions need updating [3].

❌ Failing to date-weight comparable evidence — Transactions from mid-2025 reflect a more negative market; applying them without adjustment understates current values in recovering areas.

❌ Omitting a forward-looking caveat — The 90-day validity window for valuations has never been more important to communicate clearly.

✅ Do: Use RICS survey data as a named source in market commentary sections — it demonstrates professional rigour and gives clients confidence in the analysis.

Conclusion: Actionable Next Steps for UK Surveyors and Valuers

The RICS January 2026 Market Survey: What UK Building Surveyors and Valuers Really Need to Change in Their Reports is not background reading — it is a professional obligation. The data is clear, the regional divergence is stark, and the direction of travel is improving. Reports that fail to reflect this are not just outdated; they risk misleading clients at a critical moment in the market cycle.

Here are the immediate actions every UK surveyor should take:

Whether conducting a Level 2 HomeBuyer Survey, a full Level 3 Building Survey, or a specialist commercial building survey, the quality of market commentary is now a differentiator. Clients are more informed than ever, and the RICS January 2026 data gives every surveyor the tools to serve them better.

The market is changing. The reports must change with it.

References

[1] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] tradingeconomics – https://tradingeconomics.com/united-kingdom/rics-house-price-balance/news/525158

[3] Uk Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[4] Latest Rics Survey Reveals Global Headwinds Are Weighing On Housing Market Confidence – https://www.buyassociationgroup.com/en-gb/news/latest-rics-survey-reveals-global-headwinds-are-weighing-on-housing-market-confidence/

[5] Rics January 2026 Survey Insights Building Survey Strategies For Stabilising House Prices And Regional Divides – https://wimbledonsurveyors.com/rics-january-2026-survey-insights-building-survey-strategies-for-stabilising-house-prices-and-regional-divides/

[6] Market View January 2026 – https://www.watsons-property.co.uk/market-view-january-2026/

[7] Valuation Strategies Amid January 2026 Rics Residential Survey Spotting Early Market Recovery Signals – https://nottinghillsurveyors.com/blog/valuation-strategies-amid-january-2026-rics-residential-survey-spotting-early-market-recovery-signals

[9] Rics January 2026 Residential Survey Insights Implications For Valuation Surveyors In A Stabilising Market – https://manchestersurveyors.com/rics-january-2026-residential-survey-insights-implications-for-valuation-surveyors-in-a-stabilising-market/

[10] Rics January 2026 Residential Survey Insights Valuation Strategies For Widening North South Price Gaps – https://princesurveyors.co.uk/blog/rics-january-2026-residential-survey-insights-valuation-strategies-for-widening-north-south-price-gaps/