{"cover":"Professional landscape format (1536×1024) hero image with bold text overlay: 'Valuation Services for Probate & Matrimonial Disputes: RICS Protocols Amid 2026 Inheritance Tax Shifts', extra large 72pt bold white sans-serif font with dark semi-transparent overlay box, centered upper-third composition. Background shows a split-scene: left side a formal probate legal setting with documents and scales of justice, right side a modern property valuation report with RICS branding and UK townhouses. Color palette: deep navy blue, gold accents, crisp white text. Magazine cover aesthetic, editorial quality, high contrast, 2026 tax reform theme.","content":["Landscape format (1536×1024) editorial illustration showing a RICS Red Book valuation report open on a mahogany desk beside a property deed and inheritance tax form IHT400, with a chartered surveyor's stamp and pen. Background features a blurred UK residential street with Victorian terraced houses. Warm amber and navy color tones, professional documentary photography style, sharp foreground detail on documents, depth of field blur on background. Represents RICS probate valuation protocols and 2026 IHT compliance requirements.","Landscape format (1536×1024) split-composition infographic-style image: left panel shows a courtroom or mediation table with two opposing legal teams and property floor plans, representing matrimonial dispute valuation; right panel displays a structured comparison table showing RICS Red Book standards vs informal estate agent appraisals, with green checkmarks and red crosses. Central dividing element is a balanced scale icon. Professional blue-grey color scheme, clean sans-serif typography, data-driven visual aesthetic, editorial quality.","Landscape format (1536×1024) wide-angle aerial photograph of a large UK agricultural estate with farmland, barns, and farm machinery visible from above, overlaid with a semi-transparent data panel showing inheritance tax calculation figures, percentage thresholds, £2 million property threshold markers, and stock valuation figures. Gold and dark green color palette representing agricultural wealth and 2026 IHT reform impact. Photorealistic aerial drone photography style with clean data overlay graphics, editorial quality.","Landscape format (1536×1024) close-up macro photograph of a professional chartered surveyor's hands writing in a structured valuation engagement letter, with a laptop screen visible in background showing HMRC portal and RICS UK VPGA 15 guidance document. Desk surface shows a printed comparable evidence report with highlighted figures. Shallow depth of field, warm office lighting, teal and charcoal color tones, professional documentary photography style representing mandatory RICS documentation standards and HMRC compliance."]

Nearly £7 billion in inheritance tax was collected by HMRC in the 2024/25 fiscal year — and with sweeping reforms that took effect on 6 April 2026, that figure is set to climb significantly. For executors, solicitors, divorcing couples, and property owners, the accuracy of professional property valuations has never carried higher financial stakes. Valuation Services for Probate and Matrimonial Disputes: RICS Protocols Amid 2026 Inheritance Tax Shifts sit at the intersection of legal obligation, tax compliance, and professional standards — and getting them wrong can result in HMRC challenges, financial penalties, or unfair asset division in court.

This article explains what the 2026 IHT reforms mean in practice, how RICS protocols govern valuations in both probate and matrimonial contexts, and what clients and practitioners must do to remain compliant and defensible.

Key Takeaways 📌

- April 2026 IHT reforms represent the most significant overhaul of inheritance tax rules in decades, with new valuation requirements and relief structures now in force.

- RICS Red Book standards are effectively mandatory for IHT compliance — informal estate agent appraisals are no longer acceptable to HMRC.

- The term "probate valuation" is a misnomer; valuations are formally conducted for Inheritance Tax purposes and then applied within probate proceedings.

- Agricultural stock and machinery are now subject to IHT calculations for the first time in decades under the 2026 framework.

- Matrimonial dispute valuations require the same rigorous RICS methodology, with court-admissible reports essential for fair and legally sound asset division.

Understanding RICS Protocols for Probate Valuations in 2026

What "Probate Valuation" Actually Means — And Why Terminology Matters

One of the most important clarifications in current RICS guidance is that there is no formal valuation category called a "probate valuation." [1] This is not a pedantic distinction — it has real legal and professional implications.

Valuations are formally conducted for Inheritance Tax (IHT) purposes, based on statutory definitions of value. These valuations are then used within probate proceedings. RICS standards require practitioners to avoid using the term "probate value" in reports and to clearly communicate this distinction to clients from the outset of any instruction. [1]

💡 Pull Quote: "Valuers must confirm the purpose of valuation with clients during instruction — particularly where a client requests a 'probate valuation' when an IHT valuation is actually needed." — RICS Guidance, UK VPGA 15 [1]

This matters because the basis of value, the methodology applied, and the legal defensibility of the report all flow from correctly identifying the purpose. A probate valuation conducted to the right standard will state clearly that it is prepared for IHT purposes, reference the statutory definition of open market value, and document comparable evidence accordingly.

The Open Market Value Standard

For IHT purposes, HMRC requires property assets to be valued at open market value as at the date of death. [3] This assumes:

- A willing buyer and a willing seller

- Normal market conditions at the relevant date

- Neither party under compulsion to transact

- Full knowledge of relevant facts on both sides

This principle is central to RICS Red Book compliance and applies regardless of whether the property is residential, commercial, agricultural, or mixed-use. The date of death is fixed — valuers cannot substitute a more favourable market date, even if values have shifted significantly since.

RICS Red Book: The Non-Negotiable Standard

Under the 2026 reforms, estate agent market appraisals and informal estimates are no longer acceptable for HMRC purposes. [2] Only RICS Red Book valuations — comprehensive, evidence-backed reports adhering to RICS professional standards — satisfy tax authority requirements for IHT assessments.

The governing framework is the 2024 UK supplement to the 2025 Global Red Book, which incorporates UK VPGA 15 — the specific guidance for practitioners conducting IHT valuations within the new regulatory framework. [1]

Key requirements under this framework include:

| Requirement | Detail |

|---|---|

| Purpose identification | Confirmed in writing at instruction stage |

| Basis of value | Open market value per statutory definition |

| Comparable evidence | Documented, dated, and referenced in report |

| Market conditions analysis | Conditions at date of death, not report date |

| Engagement letter | Must clearly state IHT purpose and methodology |

| Report format | RICS Red Book compliant, professionally structured |

Although IHT valuations are not formally required to be "Red Book valuations" per se, the statutory definition of value is applied alongside Red Book principles to ensure defensibility and professional standards. [1] In practice, the distinction is minimal — practitioners should always apply Red Book methodology.

For properties with complex features — non-standard construction, structural issues, or contamination concerns — the valuation process may require additional specialist input before a defensible figure can be reached.

Valuation Services for Probate and Matrimonial Disputes: RICS Protocols Amid 2026 Inheritance Tax Shifts in Contested Proceedings

Matrimonial Dispute Valuations: A Distinct but Parallel Framework

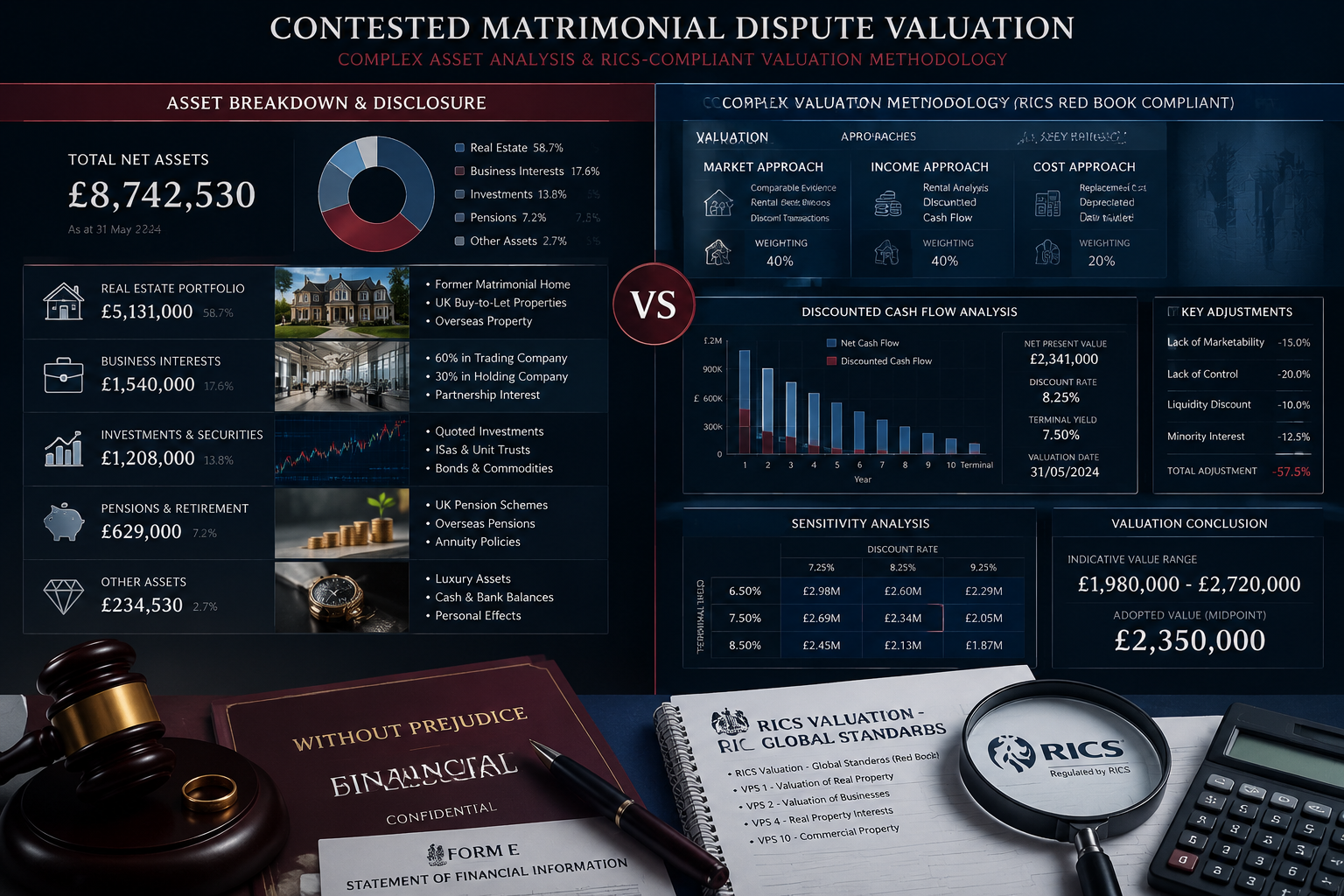

Divorce and separation proceedings often require property valuations that are just as rigorous as those prepared for IHT purposes — but the legal context is different. In matrimonial disputes, valuations are used to establish the net asset position of both parties, inform financial remedy orders, and — where parties cannot agree — provide court-admissible expert evidence.

The divorce valuation process under RICS protocols requires:

- Independence: The valuer must be impartial and not act for either party exclusively without disclosure

- Agreed single joint expert (SJE): Courts frequently direct parties to instruct a single RICS-registered valuer jointly, reducing cost and conflict

- Current market value: Unlike IHT valuations fixed to date of death, matrimonial valuations reflect value at the time of instruction or a court-specified date

- Full disclosure of methodology: Reports must be transparent, reproducible, and capable of withstanding cross-examination

⚠️ Important Note: Where one party instructs their own valuer and the other disputes the figure, the court may require both experts to meet, exchange reports, and produce a joint statement of agreed and disputed points. A robust, RICS-compliant report is essential at this stage.

HMRC Challenge Risk and the Importance of Professional Documentation

HMRC retains the right to challenge assessed property values — and it exercises that right regularly, particularly for high-value estates. [3] Professionally prepared RICS Red Book reports with clearly documented methodology, comparable evidence, and market conditions analysis significantly reduce dispute risk compared to informal valuations.

The same principle applies in matrimonial proceedings. A poorly evidenced valuation is vulnerable to challenge by the opposing party's legal team, potentially resulting in costly re-valuations, delays, and adverse cost orders.

Key documentation that strengthens any valuation's defensibility:

- ✅ Signed engagement letter confirming purpose and basis of value

- ✅ Inspection notes and photographic record

- ✅ Comparable transaction evidence with adjustments explained

- ✅ Market commentary relevant to the valuation date

- ✅ RICS-registered valuer's credentials and PI insurance confirmation

- ✅ Clear statement of assumptions and limiting conditions

For practitioners acting as expert witnesses in contested proceedings, compliance with the Civil Procedure Rules (CPR Part 35) is also mandatory. The duty to the court overrides any duty to the instructing party — a principle that must be reflected in the report's framing and conclusions.

The 2026 Multi-Layered Tax Framework for High-Value Properties

The 2026 Budget introduced a multi-layered tax framework specifically targeting high-value properties, requiring surveyors to apply valuation adjustments and develop tactical approaches for properties at £2 million thresholds and above. [4]

For estates containing properties in this bracket, the interaction between IHT, additional rate stamp duty land tax, and potential capital gains tax exposure creates a complex calculation environment. Valuers must:

- Identify which tax regime applies to each asset

- Apply the correct basis of value for each purpose

- Avoid conflating IHT market value with CGT market value where these differ

- Document the rationale for any valuation adjustments clearly

Clients with high-value residential assets should also consider a capital gains tax valuation alongside any IHT assessment, as the two calculations may require separate reports with different effective dates.

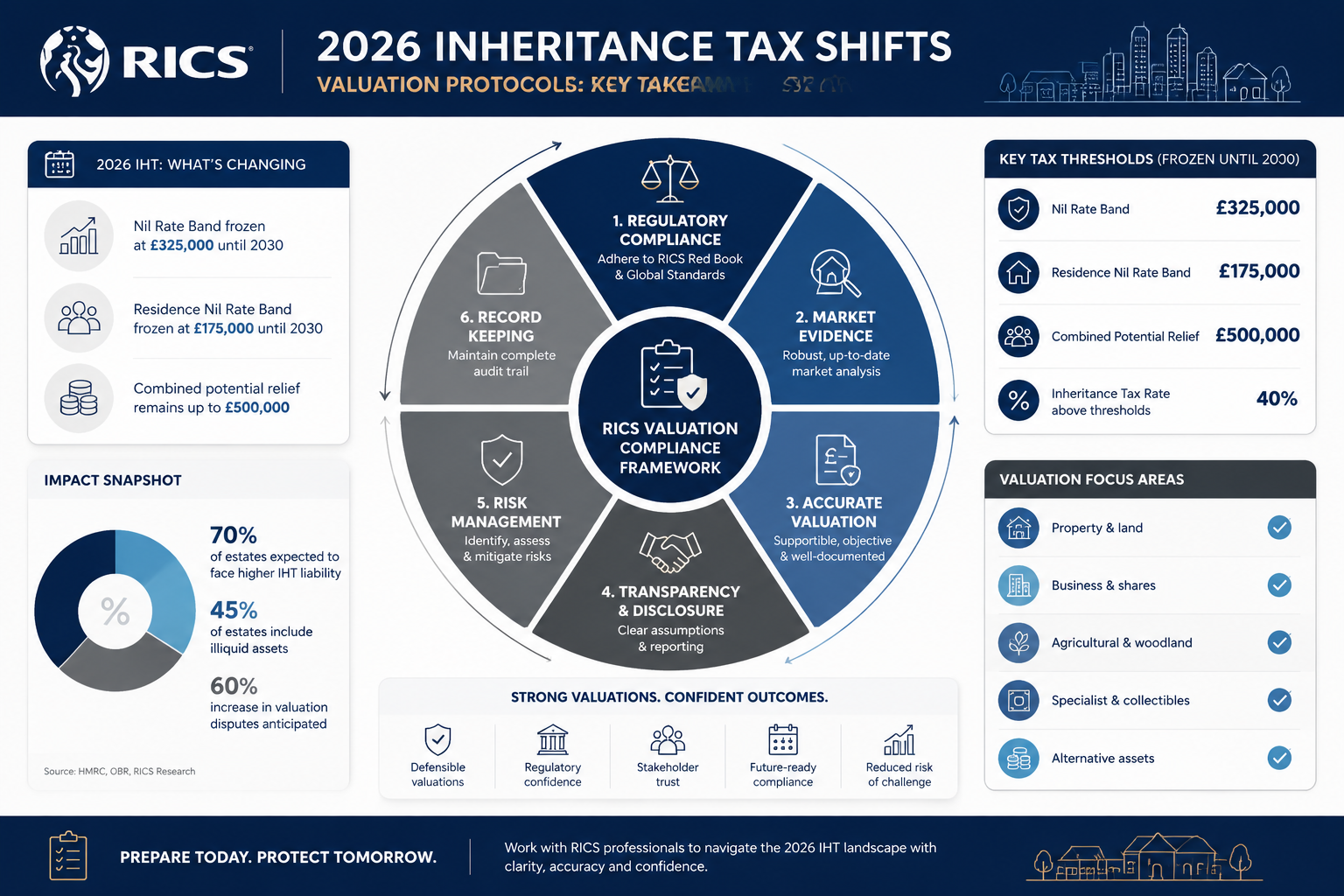

The 2026 IHT Reforms: Agricultural Assets, Stock, and New Compliance Demands

What Changed on 6 April 2026

The reforms that took effect on 6 April 2026 represent the first major overhaul of inheritance tax rules in decades. [2] For most residential property owners, the core change is the tightening of relief structures and the introduction of new valuation thresholds. But the reforms have their most dramatic impact on agricultural and rural estates.

Key changes include:

| Reform Area | Pre-2026 Position | Post-2026 Position |

|---|---|---|

| Agricultural Relief (APR) | 100% relief on qualifying agricultural property | Capped relief structure with new conditions |

| Business Property Relief (BPR) | Broad application to trading businesses | Narrowed scope; combined APR/BPR cap introduced |

| Agricultural stock & machinery | Generally outside IHT calculations | Now included in IHT calculations for the first time in decades |

| Valuation standard | Informal valuations sometimes accepted | RICS Red Book effectively mandatory |

Agricultural Stock and Machinery: A New Valuation Frontier

Under the 2026 framework, the value of agricultural stock and machinery is now brought into IHT calculations for the first time in decades. [2] This is a significant change for farming families and rural estate owners.

Crucially, for IHT purposes, stock valuations must reflect true market value rather than the accounting depreciation methods used in annual stocktaking. [2] Market values for agricultural stock are often considerably higher than book values — meaning estates that relied on accounting figures could face substantially larger IHT liabilities than anticipated.

💡 Pull Quote: "Market values for agricultural stock are often considerably higher than book values — estates relying on accounting figures could face substantially larger IHT liabilities than expected." [2]

This creates an urgent need for HMRC-compliant stocktaking conducted alongside RICS Red Book property valuations. The two exercises must be coordinated so that the total estate value presented to HMRC is consistent, defensible, and accurately reflects the interaction between property values, stock values, and available reliefs.

Factors That Affect Valuation Outcomes 🏡

Whether for probate, matrimonial, or tax purposes, several property-specific factors influence final valuation figures. Understanding these helps clients set realistic expectations and helps practitioners justify their conclusions. Key valuation factors include:

- Location and local market conditions at the relevant date

- Property condition — including structural defects, damp, or non-standard construction

- Tenure — freehold vs leasehold, with freehold valuations typically commanding a premium

- Planning status and development potential

- Agricultural tenancies or occupancy restrictions affecting marketability

- Comparable sales evidence in the relevant period

For leasehold properties, the length of the remaining lease and the terms of the lease significantly affect value — a consideration that applies equally in probate and matrimonial contexts.

HMRC's Authoritative Guidance Framework

Practitioners are directed to consult HMRC's Practice Note 1 on Valuations for Revenue Purposes, published in the Valuation Office Manual, for tax compliance standards. [1] This document sets out HMRC's expectations for how valuations are prepared, presented, and supported — and it forms the basis on which HMRC's District Valuer Service (DVS) will review challenged valuations.

The interaction between UK VPGA 15, the RICS Red Book Global Standards (incorporating IVS), and HMRC's own guidance creates a layered compliance framework that practitioners must navigate carefully. [1] [6]

Practical Steps: Commissioning Compliant Valuation Services for Probate and Matrimonial Disputes: RICS Protocols Amid 2026 Inheritance Tax Shifts

Selecting the Right Valuer

Not all valuers are equal — and for IHT and matrimonial purposes, only RICS-registered valuers with relevant experience should be instructed. When selecting a professional, verify:

- ✅ RICS membership (MRICS or FRICS designation)

- ✅ Registered Valuer status under RICS Valuer Registration scheme

- ✅ Experience with IHT valuations and HMRC correspondence

- ✅ Familiarity with the specific property type (residential, commercial, agricultural)

- ✅ Professional indemnity insurance adequate for the estate's value

- ✅ Ability to act as expert witness if proceedings become contested

For commercial properties within an estate, a specialist commercial valuation is required — residential valuers should not extend their instructions to asset classes outside their competence.

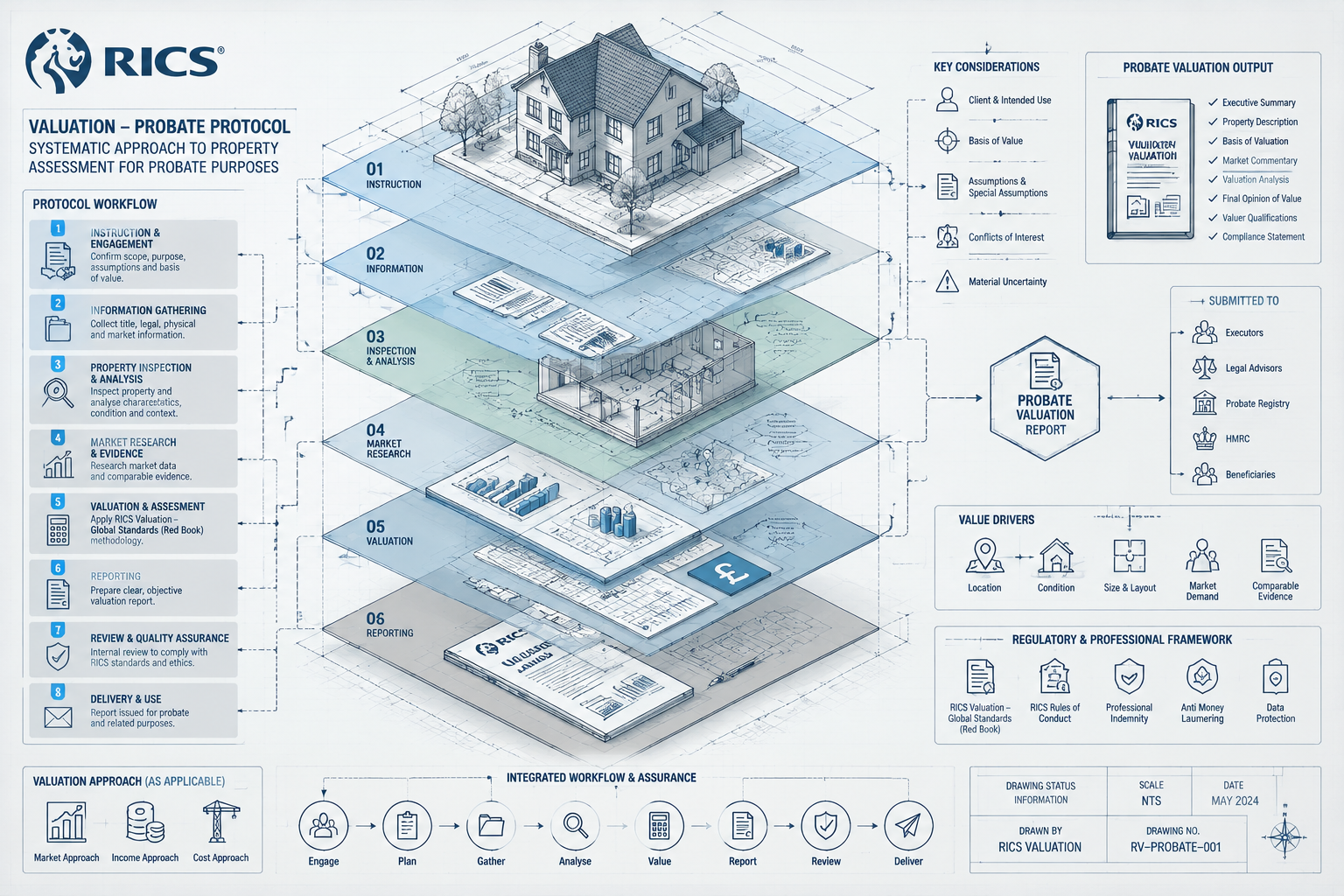

The Instruction and Engagement Process

The RICS framework places significant weight on correct instruction from the outset. [1] The engagement letter must:

- Confirm the purpose of the valuation (IHT purposes, matrimonial proceedings, etc.)

- State the basis of value (open market value, at the date of death or specified date)

- Identify the property and any relevant interests to be valued

- Set out the scope of inspection and any agreed limitations

- Confirm fee arrangements and expected delivery timeline

- State the intended use of the report and who may rely on it

Where a client uses the term "probate valuation," the valuer must clarify that the instruction is for an IHT valuation and document this correction in the engagement letter. [1] This seemingly minor point can have significant consequences if a report is later challenged on the grounds of incorrect purpose identification.

Timeline Considerations for Executors and Solicitors

Executors have a legal obligation to report the estate to HMRC and pay any IHT due within six months of the date of death. Interest accrues on unpaid IHT after this point. Instructing a RICS-registered valuer early in the probate process is therefore critical.

Recommended timeline for executors:

| Stage | Recommended Action | Timing |

|---|---|---|

| Week 1–2 | Identify all property assets in the estate | Immediately after death |

| Week 2–4 | Instruct RICS-registered valuer(s) | As early as possible |

| Week 4–8 | Receive and review valuation report(s) | Allow adequate inspection time |

| Week 8–12 | Submit IHT400 to HMRC with valuations | Before 6-month deadline |

| Ongoing | Respond to any HMRC queries or challenges | As required |

Conclusion: Actionable Next Steps for 2026 Compliance ✅

The 2026 inheritance tax reforms have fundamentally raised the bar for property valuation in both probate and matrimonial contexts. Valuation Services for Probate and Matrimonial Disputes: RICS Protocols Amid 2026 Inheritance Tax Shifts are no longer a procedural formality — they are a critical risk management tool for executors, beneficiaries, divorcing parties, and their legal advisers.

Here are the most important actions to take right now:

-

Instruct early — Do not wait until HMRC deadlines are imminent. RICS-registered valuers need adequate time to inspect, research comparables, and prepare compliant reports.

-

Use the right terminology — Brief your legal team and clients on the distinction between "IHT valuations" and "probate valuations." Correct framing from the start prevents costly errors later.

-

Apply Red Book standards without exception — Informal appraisals and estate agent estimates are not acceptable to HMRC under the 2026 framework. Every valuation must meet RICS Red Book methodology.

-

Address agricultural assets proactively — If the estate includes farming assets, stock, or machinery, commission HMRC-compliant stocktaking alongside the property valuation. Do not rely on accounting book values.

-

Prepare for HMRC scrutiny at £2 million+ — High-value properties face enhanced HMRC review under the 2026 multi-layered tax framework. Ensure reports contain robust comparable evidence and clearly documented adjustments.

-

Seek specialist expert witness support for contested matters — Where valuations are disputed in probate or matrimonial proceedings, engage a RICS-registered expert witness with CPR Part 35 experience.

The cost of a professionally prepared RICS Red Book valuation is modest compared to the financial exposure created by an HMRC challenge or a contested court proceeding. In 2026, professional compliance is not optional — it is essential.

References

[1] Inheritance Tax Valuations – https://community.rics.org/viewdocument/inheritance-tax-valuations

[2] Inheritance Tax Reform 2026 Importance Of Accurate Rics Red Book Valuations And Hmrc Compliant Stocktaking For Owners Of Agricultural Land And Property – https://www.krestonreeves.com/news/inheritance-tax-reform-2026-importance-of-accurate-rics-red-book-valuations-and-hmrc-compliant-stocktaking-for-owners-of-agricultural-land-and-property/

[3] Rics Red Book Valuation Reports For Probate – https://www.vickeryholman.com/news/rics-red-book-valuation-reports-for-probate/

[4] Valuation Adjustments For High Value Properties Under 2026 Budget Tax Changes Surveyor Tactics For 2m Thresholds – https://nottinghillsurveyors.com/blog/valuation-adjustments-for-high-value-properties-under-2026-budget-tax-changes-surveyor-tactics-for-2m-thresholds

[6] Red Book Global Standards Incorporating Ivs – https://www.rics.org/content/dam/ricsglobal/documents/standards/Red-Book-Global-Standards-incorporating-IVS.pdf