From May 2026, the legal mechanism that once gave landlords their most powerful exit tool — the Section 21 "no-fault" eviction notice — no longer exists. For buy-to-let investors and the chartered surveyors who value their assets, this is not a minor regulatory tweak. It is a structural shift in the risk profile of every tenanted residential property in England.

Valuing Rental Properties Under the Renters' Rights Act 2026: Surveyor Adjustments for Section 21 Abolition is now one of the most pressing valuation challenges facing the profession. The rules governing how landlords can recover possession, increase rents, and sell tenanted properties have changed fundamentally — and RICS-registered valuers must reflect these changes in every assessment they produce.

Key Takeaways 📋

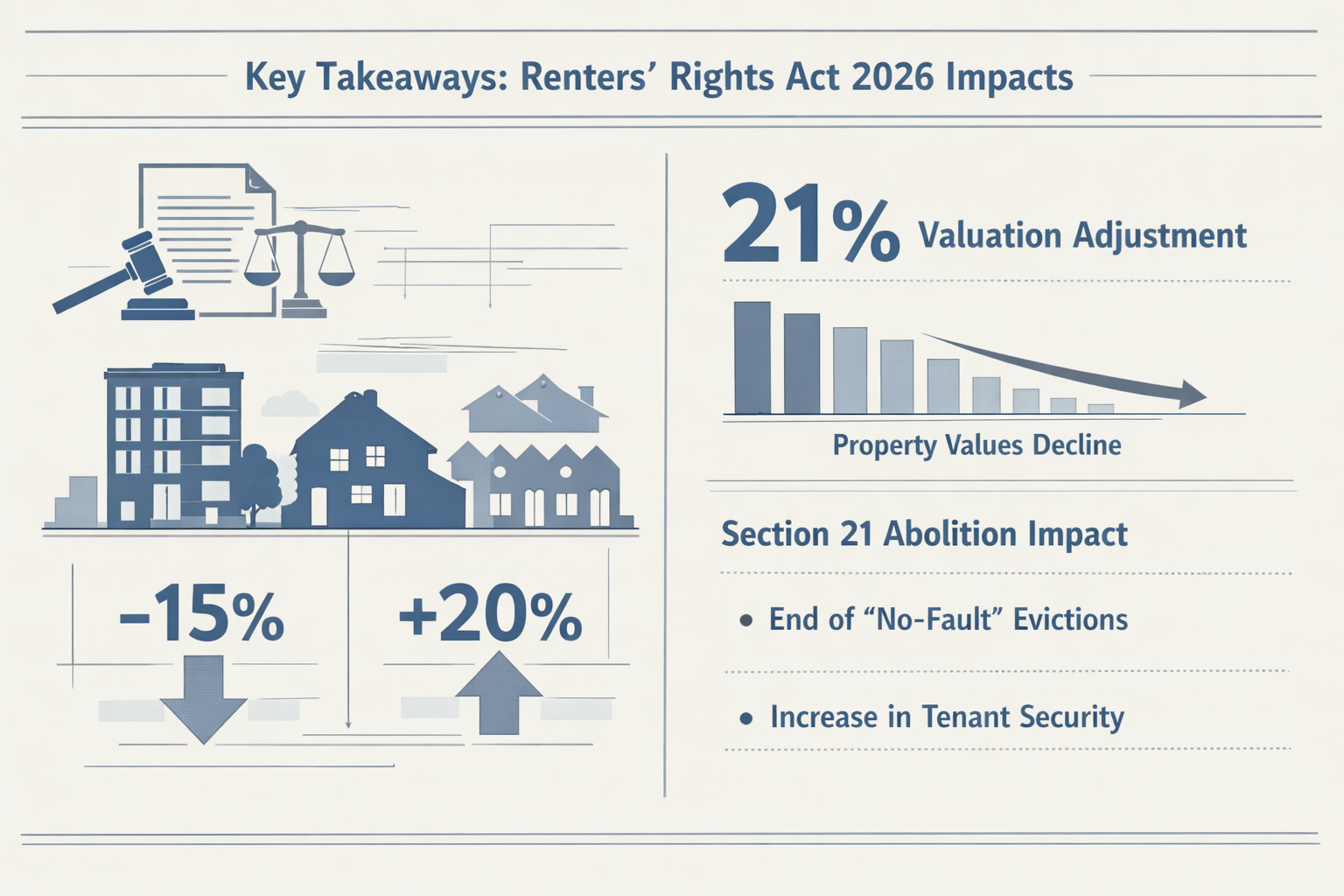

- Section 21 abolition makes vacant possession significantly harder to achieve, directly reducing the attractiveness of tenanted properties to buyers and affecting capital values.

- Ground 1A (sale) comes with a 12-month tenancy minimum, a 4-month notice period, and a 12-month re-letting ban — all of which surveyors must factor into yield and liquidity assessments.

- Rent increase restrictions (once per year, challengeable at tribunal) compress future income growth projections and affect investment valuations.

- EPC 'C' grade requirements by 2030 create measurable capital expenditure obligations that must be reflected in valuation adjustments.

- Surveyors must now apply specific discounts to tenanted properties, particularly in high-demand urban markets where landlord flexibility has been most curtailed.

Why Section 21 Abolition Changes Everything for Property Valuers

For over 30 years, Section 21 of the Housing Act 1988 gave landlords a straightforward route to recovering possession. No grounds needed. Two months' notice. Done. This flexibility meant that tenanted properties were valued close to their vacant possession equivalents — the risk of being "stuck" with a tenant was manageable and time-limited.

That calculation no longer holds.

Under the Renters' Rights Act 2026, landlords must now rely on specific statutory grounds to regain possession [1]. If a tenant refuses to leave, the landlord must pursue a court hearing. This process can take many months, introduces legal costs, and carries genuine uncertainty. For a buyer considering a tenanted property, this is a material change in risk — and risk, in valuation terms, means discount.

💬 "The abolition of Section 21 does not just affect landlords — it redefines the investment case for every tenanted property in England."

Surveyors conducting RICS building surveys or formal valuations on buy-to-let properties must now treat the tenancy status of a property as a primary valuation variable, not a secondary consideration.

Understanding the New Legal Framework: What Surveyors Need to Know

The End of No-Fault Eviction

Section 21 notices — which allowed landlords to end an Assured Shorthold Tenancy without giving a reason — have been abolished [1]. All tenancies now operate under a single system of periodic tenancies, with possession only recoverable through specific grounds set out in the Act.

This matters enormously for valuation because:

- Vacant possession is no longer a given. A landlord who wants to sell cannot simply serve notice and expect the property to be empty in two months.

- Court proceedings introduce time and cost risk. Even where valid grounds exist, enforcement is not guaranteed or swift.

- Buyer pools shrink. Owner-occupier buyers — who typically pay the highest prices — are far less willing to purchase a property with an entrenched tenant and no clear exit route.

Ground 1A: The Sale Ground and Its Restrictions

The Act introduces Ground 1A, which allows landlords to seek possession in order to sell the property [4]. However, this ground comes with significant constraints that surveyors must understand:

| Restriction | Detail |

|---|---|

| Minimum tenancy before use | 12 months from tenancy start |

| Notice period required | 4 months |

| Re-letting ban after use | 12 months |

| Tenant challenge rights | Tenant can dispute at tribunal |

The 12-month re-letting ban is particularly significant. If a landlord uses Ground 1A to sell and the sale falls through, they cannot simply re-let the property for a full year [4]. This creates a liquidity trap that reduces the attractiveness of the asset and must be reflected in any professional valuation.

Rent Increase Restrictions

Under the new framework, landlords can raise rent only once per year, using a Section 13 notice, with a minimum of two months' notice to the tenant [3]. Tenants retain the right to challenge any proposed increase at a tribunal, which can cap or reject the increase entirely.

For investment valuations — particularly those based on income capitalisation methods — this has a direct effect on projected rental income growth. Surveyors must now apply more conservative rental growth assumptions when modelling future income streams.

No rental bidding wars are permitted either. Agents and landlords cannot accept offers above the advertised asking rent, removing a mechanism that previously allowed landlords in high-demand areas to achieve above-market rents [3].

How Surveyors Should Adjust Valuations: A Practical Framework for Valuing Rental Properties Under the Renters' Rights Act 2026

1. Tenancy Status Discount

The most immediate adjustment is a discount applied to properties with sitting tenants. Pre-2026, this discount was typically modest — often 5–10% — because Section 21 provided a clear and relatively quick exit route. Post-abolition, surveyors should consider:

- Properties with long-term tenants: Discounts of 10–20% below vacant possession value may now be appropriate, depending on the tenant's track record, the local rental market, and the strength of any grounds available to the landlord.

- Properties with recent tenancies (under 12 months): These carry additional risk because Ground 1A cannot yet be used, and the landlord has very limited options for recovery.

- Properties in high-demand urban areas (such as those covered by chartered surveyors in London or chartered surveyors in Surrey): The gap between tenanted and vacant values may be wider because owner-occupier demand — and therefore the vacant possession premium — is higher in these markets.

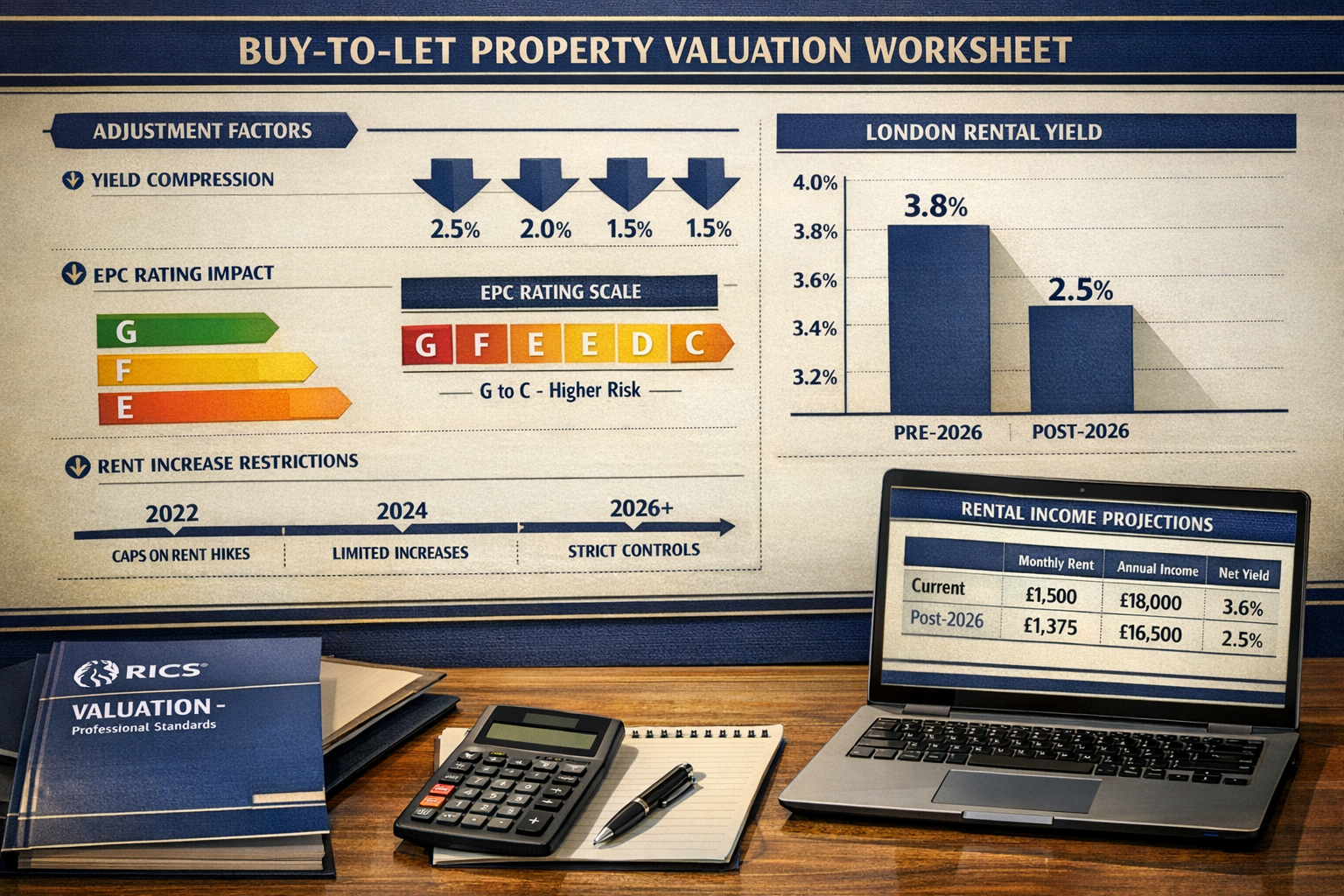

2. Yield-Based Adjustments

For investment buyers, the valuation is driven by yield. Under the new regime, surveyors must reassess both the income and the risk side of the yield equation:

Income adjustments:

- Apply conservative rental growth assumptions (e.g., CPI or below) given tribunal challenge rights

- Stress-test income against void periods that may be longer if Ground 1A restrictions apply

- Remove any above-asking-rent premium from comparable rental evidence

Risk adjustments:

- Increase the capitalisation rate (i.e., apply a higher yield) to reflect reduced landlord flexibility

- Factor in potential legal costs if possession proceedings become necessary

- Account for the possibility of extended void periods during any court process

📌 Key point for valuers: A property that previously yielded 5% on a straightforward tenancy may now need to be assessed at a 5.5–6% yield to reflect the additional risk — which translates directly into a lower capital value.

3. EPC Capital Expenditure Allowances

The Act also accelerates EPC requirements. Properties must achieve a minimum 'C' rating by 2030, with assessments beginning in 2026 [1]. For properties currently rated D, E, F, or G, surveyors must:

- Obtain or review the current EPC rating

- Estimate the cost of works required to reach a 'C' rating

- Apply this as a deduction from the gross valuation figure

For older properties — particularly Victorian terraces and pre-war stock common in areas served by chartered surveyors in Hampshire or chartered surveyors in Buckinghamshire — these costs can be substantial. Solid wall insulation, for example, can run to £10,000–£20,000 or more per property.

A homebuyer survey or full building survey should now routinely flag EPC status as a material valuation consideration for any investment property.

4. Liquidity Risk Premium

One of the less-discussed but highly material effects of the new Act is reduced liquidity. A tenanted property under the old regime could be sold to a wide range of buyers — owner-occupiers willing to wait out a Section 21 notice, investors comfortable with the short-term risk, and developers who could clear the property quickly.

Under the new regime, the buyer pool narrows significantly:

- ✅ Investors willing to hold long-term with the sitting tenant

- ✅ Investors who can identify a valid possession ground

- ❌ Owner-occupiers (in most cases)

- ❌ Developers requiring vacant possession

- ❌ Short-term flippers

This narrowing of the buyer pool is a classic liquidity discount scenario. Surveyors should reflect this in their assessments, particularly for properties where the tenant is well-established and no immediate possession ground is available.

Regional Considerations and Market-Specific Adjustments

The impact of Section 21 abolition is not uniform across England. Markets where owner-occupier demand is strongest — and therefore where the vacant possession premium is highest — will see the largest valuation adjustments for tenanted properties.

High-impact markets include:

- Prime London boroughs (where chartered surveyors in Chelsea and chartered surveyors in Clapham regularly advise on high-value buy-to-let assets)

- Commuter belt towns in Surrey, Hampshire, and Hertfordshire

- University towns with high tenant turnover and strong owner-occupier demand

Lower-impact markets include areas where the gap between tenanted and vacant possession values was already small — typically lower-value markets where investor buyers dominate and owner-occupier demand is weaker.

Surveyors must use local comparable evidence carefully. Pre-2026 sales of tenanted properties cannot be used as direct comparables without adjustment, because they reflected a different risk environment. Fresh evidence from post-Act transactions — where available — should be weighted more heavily.

For complex investment portfolios or multi-unit blocks, a commercial property surveyor with specific experience in the residential investment sector may be the most appropriate professional to instruct.

Valuing Rental Properties Under the Renters' Rights Act 2026: Common Valuation Mistakes to Avoid

Even experienced valuers can fall into traps when navigating new legislation. Here are the most common errors to watch for:

❌ Using pre-2026 comparable evidence without adjustment — Sales that completed before May 2026 reflected a different legal landscape. Apply a legislative risk adjustment.

❌ Ignoring Ground 1A restrictions — Failing to account for the 12-month minimum tenancy and 12-month re-letting ban can lead to significant overvaluation [4].

❌ Applying a flat percentage discount regardless of tenancy age — A tenancy of 11 months carries far more risk than one of 5 years with a reliable tenant and a motivated landlord. Adjustments must be case-specific.

❌ Overlooking EPC obligations — Properties rated D or below face mandatory capital expenditure by 2030 [1]. This must be reflected in the valuation, not noted as a caveat.

❌ Assuming rental income will grow at historic rates — Tribunal challenge rights and the ban on above-asking-rent offers mean that rental income projections must be more conservative than in previous years [3].

Practical Steps for Surveyors and Their Clients

For surveyors instructed on rental property valuations in 2026 and beyond, the following steps are now essential:

- Confirm tenancy status and start date — Establish whether Ground 1A is available and how much notice would be required.

- Review the current EPC rating — Identify any capital expenditure gap to 'C' grade and quantify the cost.

- Analyse rental income against market evidence — Strip out any above-market rents that may not be sustainable under the new regime.

- Apply a possession risk premium — Reflect the cost, time, and uncertainty of any future possession proceedings in the capitalisation rate.

- Narrow the comparable pool — Use only post-Act comparables where possible, or apply a clear legislative adjustment to pre-Act evidence.

- Document the rationale — RICS Red Book compliance requires that all material assumptions and adjustments are clearly explained in the valuation report.

Understanding surveyor pricing is also relevant here — the additional complexity of post-Act valuations may justify higher professional fees, and clients should be made aware of this upfront.

Conclusion: Adapting to the New Normal in Buy-to-Let Valuation

The Renters' Rights Act 2026 has fundamentally altered the risk and return profile of tenanted residential property in England. For surveyors, the professional obligation is clear: valuations must reflect the new legal reality, not the assumptions of a pre-abolition market.

Valuing Rental Properties Under the Renters' Rights Act 2026: Surveyor Adjustments for Section 21 Abolition is not a niche specialism — it is now a core competency for any RICS-registered valuer working in the residential investment sector.

Actionable Next Steps ✅

- For surveyors: Update your valuation methodology notes to reflect Section 21 abolition, Ground 1A restrictions, and EPC obligations. Ensure all comparable evidence is screened for pre/post-Act status.

- For landlords considering selling: Seek a post-Act valuation from a qualified surveyor before listing. Understand whether Ground 1A is available and what the re-letting restriction means for your plans.

- For buyers of tenanted properties: Instruct a surveyor with specific experience in investment property valuation. Ensure any offer reflects the full risk profile of the tenancy, not just the headline yield.

- For all parties: Monitor tribunal decisions on rent challenges — these will quickly establish the practical limits of rent growth under the new regime and should inform income projections.

The property market adapts. Surveyors who understand these changes — and communicate them clearly to clients — will be the most valuable professionals in this new landscape.

References

[1] Selling A Rental Property In 2026 How The New Renters Rights Bill Affects You – https://www.gorvinsresidential.com/selling-a-rental-property-in-2026-how-the-new-renters-rights-bill-affects-you/

[3] Renters Rights Bill A Letting Agents Guide – https://blog.goodlord.co/renters-rights-bill-a-letting-agents-guide

[4] Renters Rights Act Everything Guide – https://www.crownluxuryhomes.com/renters-rights-act-everything-guide/