The rental market landscape is shifting dramatically in 2026, and institutional investors are taking notice. As tenant demand edges higher and landlord instructions remain firmly negative at -27% [2], co-living spaces are emerging as a compelling solution to fill critical rental gaps in urban markets. However, beneath the surface of this growing opportunity lies a complex web of valuation challenges, regulatory compliance issues, and investment risks that demand careful scrutiny. Valuing Co-Living Spaces in Tenant Demand Surge: RICS Red Flags for 2026 Institutional Investments requires a sophisticated understanding of hybrid valuation methodologies, Houses in Multiple Occupation (HMO) regulations, and stress-testing frameworks that go far beyond traditional residential property assessment.

For chartered surveyors and institutional investors navigating this emerging asset class, the stakes have never been higher. The convergence of rising rental prices, limited landlord supply, and changing tenant preferences creates both unprecedented opportunities and significant pitfalls for those unprepared to identify the red flags.

Key Takeaways

- 📊 Tenant demand remained stable at +2% in February 2026, while landlord instructions hit -27%, creating supply-demand imbalances that co-living spaces can address [2]

- 🚩 HMO compliance failures represent the most significant valuation risk for co-living investments, requiring rigorous due diligence on licensing, fire safety, and planning permissions

- 💼 Hybrid comparable analysis combining traditional residential, HMO, and purpose-built student accommodation (PBSA) data provides the most accurate valuation framework for co-living assets

- 🔍 Stress-testing occupancy scenarios between 75-95% is essential for institutional portfolios, as co-living income models are highly sensitive to vacancy rates

- ⚖️ RICS Red Book compliance demands specialized expertise when valuing co-living spaces, particularly around assumptions, comparable evidence, and risk adjustments

Understanding Co-Living Spaces in the 2026 Rental Market Context

Co-living represents a modern evolution of shared housing, designed specifically to meet the needs of urban professionals, young workers, and mobile populations seeking affordable, flexible accommodation with built-in community features. Unlike traditional house shares or flatmates arrangements, co-living developments offer professionally managed spaces with purpose-designed communal areas, all-inclusive pricing, and shorter-term flexibility.

The appeal of co-living has intensified in 2026 as the UK residential market shows early signs of recovery despite continued caution [1]. With rental prices expected to rise further and new landlord instructions remaining scarce [2], co-living fills a critical gap in the rental supply chain, particularly in high-demand urban centers like London, Manchester, Birmingham, and Bristol.

The Tenant Demand Surge Driving Co-Living Growth

Recent RICS survey data reveals compelling market dynamics:

- Tenant demand net balance: +2% in February 2026, indicating stable but persistent rental demand [2]

- Landlord instructions: -27% showing continued withdrawal of traditional rental stock from the market [2]

- Near-term rental expectations: Surveyors anticipate further price increases as supply constraints persist [2]

These conditions create an ideal environment for co-living operators and investors. The model offers several advantages:

✅ Higher rental yields through optimized space utilization

✅ Reduced void periods with shorter tenancy terms and rolling occupancy

✅ Premium pricing for all-inclusive services and community features

✅ Diversified income streams from multiple tenants per property

However, institutional investors must recognize that co-living spaces occupy a unique position between traditional residential lettings and commercial HMO operations. This hybrid nature creates specific valuation challenges that require specialist expertise from registered RICS valuers familiar with multi-tenanted residential assets.

RICS Red Flags When Valuing Co-Living Spaces in Tenant Demand Surge

The Royal Institution of Chartered Surveyors (RICS) sets rigorous standards for property valuation through the Red Book [4], but co-living spaces present unique challenges that can trip up even experienced valuers. Understanding these red flags is essential for Valuing Co-Living Spaces in Tenant Demand Surge: RICS Red Flags for 2026 Institutional Investments accurately and defensibly.

🚨 Critical Red Flag #1: HMO Licensing and Compliance Status

The single most significant risk in co-living valuations relates to Houses in Multiple Occupation (HMO) compliance. Many co-living operations require HMO licenses, but the regulatory landscape varies significantly across local authorities.

Key compliance issues to verify:

| Compliance Area | Valuation Impact | Red Flag Indicators |

|---|---|---|

| HMO Licensing | 20-35% value reduction if non-compliant | Missing mandatory license, expired certification |

| Fire Safety Standards | 15-25% value reduction | Inadequate fire doors, missing alarms, non-compliant escape routes |

| Planning Permission | 30-50% value reduction | Use class violations, unauthorized conversions |

| Building Regulations | 10-20% value reduction | Substandard room sizes, inadequate facilities |

| Article 4 Directions | Potential unmarketability | Local authority restrictions on HMO conversions |

A RICS commercial building survey can identify many of these physical compliance issues, but valuers must also verify documentary evidence of licensing and permissions. Never assume compliance – always request and verify:

- Current HMO license (if applicable)

- Planning permission documentation

- Building control completion certificates

- Fire risk assessment reports

- Gas and electrical safety certificates

🚨 Critical Red Flag #2: Inappropriate Comparable Evidence

Co-living valuations frequently fail when surveyors rely exclusively on traditional residential comparables. The income profile, management intensity, and tenant profile differ substantially from standard buy-to-let investments.

Best practice requires hybrid comparable analysis:

- Traditional residential lettings (adjusted for multi-tenancy premium)

- Established HMO properties (similar configuration and management)

- Purpose-built student accommodation (PBSA) (comparable operational model)

- Other co-living schemes (direct comparables where available)

When conducting valuation reports, surveyors should weight these different comparable categories based on the specific characteristics of the subject property. A purpose-built co-living development with 50+ units operates more like PBSA, while a converted Victorian house with 6-8 bedrooms shares more characteristics with traditional HMOs.

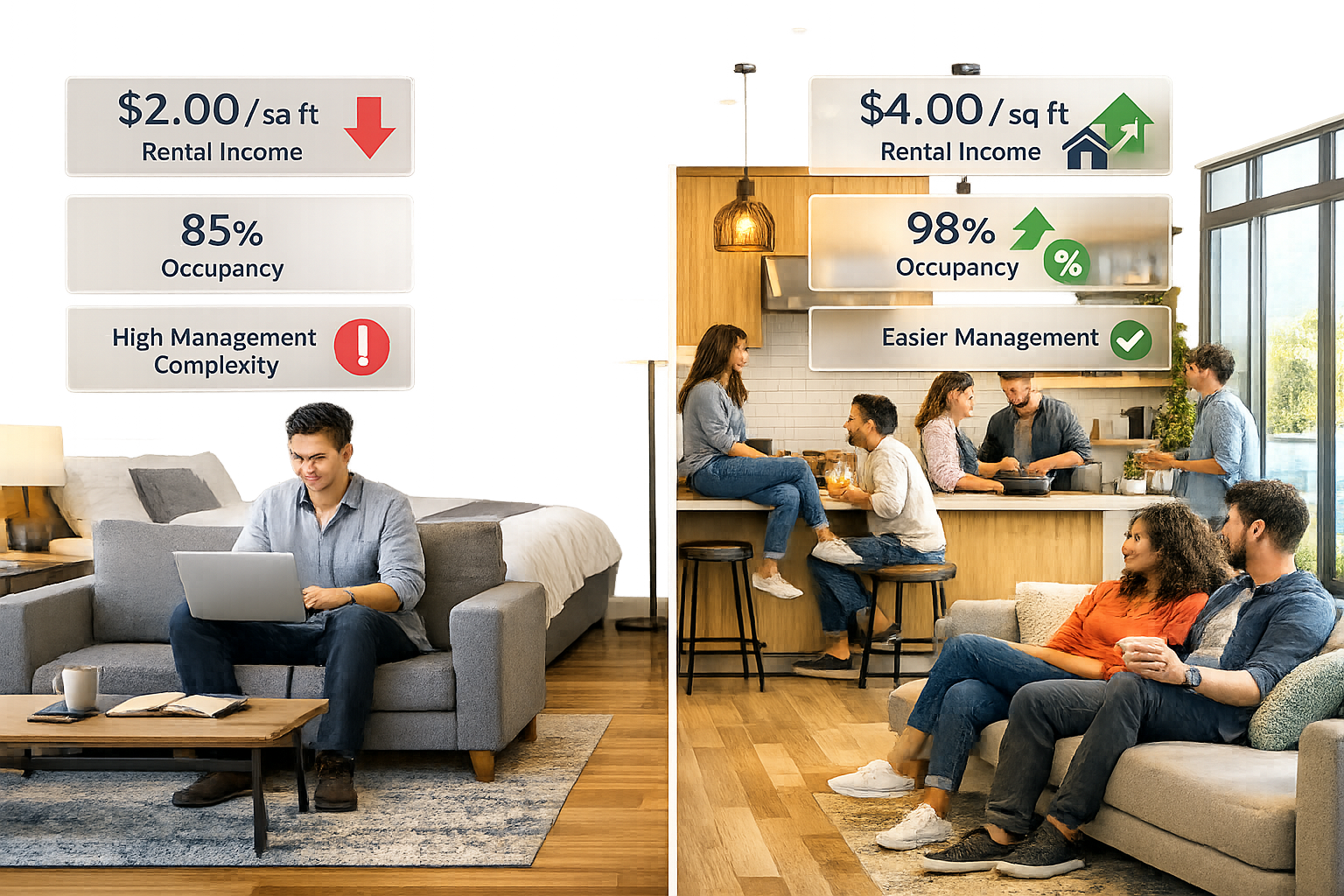

🚨 Critical Red Flag #3: Overly Optimistic Occupancy Assumptions

Co-living income projections are extremely sensitive to occupancy rates. A seemingly small variance from 95% to 85% occupancy can reduce net operating income by 15-20% after accounting for fixed costs.

Stress-testing framework for institutional portfolios:

- Base case: 90% occupancy (realistic long-term average)

- Downside case: 80% occupancy (market downturn scenario)

- Worst case: 75% occupancy (severe market stress)

Valuers should also consider seasonal occupancy patterns, particularly in university cities where co-living competes with student accommodation. Properties in business districts typically show more stable year-round occupancy than those in academic areas.

🚨 Critical Red Flag #4: Inadequate Management Cost Provisions

Co-living spaces require significantly higher management input than traditional residential lettings. Institutional investors often underestimate these costs, leading to inflated net income projections.

Typical management cost provisions:

- Traditional buy-to-let: 8-12% of gross rental income

- Standard HMO: 12-18% of gross rental income

- Co-living (converted property): 15-22% of gross rental income

- Co-living (purpose-built with amenities): 18-25% of gross rental income

These higher costs reflect intensive tenant turnover, communal area maintenance, 24/7 support services, community management, and regulatory compliance administration. A RICS specialist defect survey can identify maintenance liabilities that will impact ongoing management costs.

🚨 Critical Red Flag #5: Uncertain Exit Strategy and Liquidity

Co-living properties occupy an awkward position in the investment market. They're too specialized for most residential investors but may not meet the scale requirements of institutional commercial buyers.

Exit strategy considerations:

- Limited buyer pool for converted HMO/co-living properties

- Potential requirement to return property to single residential use

- Planning restrictions on future use

- Difficulty obtaining mortgage finance for buyers

- Market cycle sensitivity in high-demand urban areas

Valuers should apply appropriate liquidity discounts when assessing co-living assets, particularly for smaller schemes (under 20 units) or properties in secondary locations. This is similar to considerations in valuing shared ownership properties, where market liquidity impacts value.

Advanced Valuation Methodologies for Co-Living Portfolios

Institutional investors require robust, defensible valuation methodologies that comply with RICS standards while accurately reflecting the unique characteristics of co-living assets. Valuing Co-Living Spaces in Tenant Demand Surge: RICS Red Flags for 2026 Institutional Investments demands a sophisticated approach that goes beyond simple comparable analysis.

The Hybrid Comparable Method

The most reliable approach for co-living valuation combines multiple comparable datasets with appropriate adjustments:

Step 1: Establish gross rental value per room

- Analyze comparable co-living schemes (direct evidence)

- Review HMO rental rates in the locality

- Consider PBSA rental rates (where relevant)

- Assess traditional residential rents with multi-tenancy premium

Step 2: Apply adjustment factors

- Quality of communal facilities (+5% to +15%)

- All-inclusive vs. bills-separate pricing (+8% to +12%)

- Contract flexibility premium (+3% to +8%)

- Location and transport links (+5% to +20%)

- Management service quality (+5% to +10%)

Step 3: Calculate net operating income

- Gross rental income (realistic occupancy assumption)

- Less: void allowance (typically 5-10%)

- Less: management costs (15-25%)

- Less: maintenance and repairs (8-12%)

- Less: utilities and services (varies by model)

- Less: regulatory compliance costs (2-4%)

Step 4: Apply appropriate yield

- Prime co-living (purpose-built, urban): 4.5-5.5%

- Secondary co-living (converted, good location): 5.5-6.5%

- Tertiary co-living (converted, average location): 6.5-8.0%

- HMO-style co-living (smaller scale): 7.0-9.0%

This methodology aligns with RICS valuation methods while accounting for co-living-specific factors.

Stress-Testing Framework for Institutional Portfolios

Sophisticated institutional investors implement comprehensive stress-testing to understand downside risks across their co-living portfolios. This approach is particularly important given the current market context of rising tenant demand but persistent supply constraints [1][2].

Multi-scenario analysis framework:

Scenario A: Base Case (Probability: 60%)

- Occupancy: 90%

- Rental growth: +3% annually

- Operating cost inflation: +2.5% annually

- Exit yield: 5.5%

Scenario B: Market Correction (Probability: 25%)

- Occupancy: 82%

- Rental growth: +1% annually

- Operating cost inflation: +4% annually

- Exit yield: 6.5%

Scenario C: Severe Downturn (Probability: 10%)

- Occupancy: 75%

- Rental growth: -2% (year 1), flat thereafter

- Operating cost inflation: +5% annually

- Exit yield: 7.5%

Scenario D: Regulatory Shock (Probability: 5%)

- Forced compliance expenditure: £15,000-£25,000 per unit

- Temporary closure during remediation

- Occupancy recovery period: 12-18 months

- Reputational impact on portfolio

Valuation Adjustments for Regulatory Risk

Given the complex regulatory environment surrounding HMOs and co-living spaces, prudent valuers apply specific risk adjustments:

Regulatory risk matrix:

- ✅ Fully compliant with all current regulations: No adjustment

- ⚠️ Minor compliance gaps (easily remedied): -5% to -8% adjustment

- ⚠️ Moderate compliance issues: -12% to -18% adjustment

- 🚫 Major compliance failures: -25% to -40% adjustment

- 🚫 Operating without required licenses: Property may be unmarketable

These adjustments should be clearly documented in valuation reports, with specific reference to the compliance gaps identified and estimated remediation costs. This transparency is essential for institutional investors making portfolio allocation decisions.

Comparable Evidence Weighting System

When multiple comparable sources are available, professional valuers should apply a weighting system based on relevance and reliability:

| Comparable Type | Typical Weighting | Adjustment Factors |

|---|---|---|

| Direct co-living comparables (same operator) | 40-50% | Highest relevance, limited availability |

| Direct co-living comparables (different operator) | 25-35% | High relevance, adjust for operator quality |

| Purpose-built student accommodation | 15-25% | Similar operational model, adjust for tenant profile |

| Established HMO properties | 10-20% | Similar physical format, adjust for management |

| Traditional residential (adjusted) | 5-10% | Baseline reference, significant adjustments needed |

This weighted approach provides more defensible valuations than relying on any single comparable source, particularly important when presenting to institutional investment committees.

The Income Capitalization Approach

For stabilized co-living portfolios with established operating histories, the income capitalization approach offers a reliable valuation method:

Formula: Value = Net Operating Income (NOI) / Capitalization Rate

Key considerations:

- NOI calculation must reflect actual operating performance over minimum 12-24 months

- Capitalization rates should reflect co-living-specific risks (typically 50-150 basis points above traditional residential)

- Growth assumptions must be conservative and market-evidenced

- Terminal value calculations should consider exit strategy limitations

This approach is particularly valuable for larger portfolios (50+ units) where individual property variations average out across the portfolio. For smaller schemes or development projects, the comparable method typically provides more reliable results.

Practical Guidance for Surveyors and Institutional Investors

Successfully navigating the co-living investment landscape requires practical expertise beyond theoretical valuation knowledge. Here are actionable strategies for both surveyors and institutional investors.

For Chartered Surveyors: Due Diligence Checklist

When instructed to value co-living spaces, surveyors should implement a comprehensive due diligence process:

Pre-inspection documentation review:

- Current HMO license and conditions

- Planning permission and use class documentation

- Building regulations approval certificates

- Fire risk assessment (dated within 12 months)

- Gas safety certificates (annual)

- Electrical installation condition report (5-yearly)

- Energy Performance Certificates for each lettable unit

- Tenancy agreements and occupancy records (12+ months)

- Operating cost breakdown (detailed)

- Management agreements and service contracts

Physical inspection focus areas:

- Fire safety provisions (doors, alarms, escape routes, signage)

- Room sizes and compliance with minimum standards

- Kitchen and bathroom facilities (number and condition)

- Communal area quality and maintenance

- Building fabric condition and deferred maintenance

- Accessibility and disabled facilities

- Storage provisions and waste management

- Security systems and access control

Market analysis requirements:

- Comparable co-living schemes within 1-mile radius

- HMO rental evidence from local letting agents

- PBSA rental rates (if relevant to location)

- Occupancy trends and seasonal patterns

- Local authority HMO licensing policy and Article 4 directions

- Planning policy regarding co-living and HMOs

- Transport links and local amenities assessment

This thorough approach ensures compliance with RICS Red Book standards [4] and provides institutional clients with the comprehensive analysis they require for investment decisions. For complex properties, engaging commercial property surveyors with multi-tenanted residential experience is advisable.

For Institutional Investors: Risk Mitigation Strategies

Institutional investors can implement several strategies to mitigate the specific risks associated with co-living investments:

1. Portfolio Diversification

- Spread investments across multiple locations (minimum 3-5 cities)

- Mix property types (purpose-built and converted)

- Vary unit counts (avoid concentration in single large schemes)

- Diversify tenant demographics (professionals, students, key workers)

2. Operator Selection and Management

- Partner with experienced co-living operators with 3+ year track records

- Implement performance-based management agreements

- Require regular compliance auditing and reporting

- Establish clear remediation protocols for compliance failures

3. Acquisition Due Diligence

- Engage RICS-qualified valuers with co-living experience

- Conduct comprehensive legal due diligence on licenses and permissions

- Obtain independent building surveys focusing on compliance

- Stress-test financial models across multiple scenarios

- Verify comparable evidence independently

4. Active Asset Management

- Quarterly compliance reviews and audits

- Monthly occupancy and financial performance monitoring

- Annual market rent reviews and benchmarking

- Proactive maintenance and capital expenditure planning

- Regular tenant satisfaction surveys and feedback loops

5. Exit Strategy Planning

- Maintain properties to institutional standards

- Document all compliance and licensing rigorously

- Build relationships with potential acquirers

- Consider conversion options for alternative uses

- Monitor market liquidity and timing for disposals

Understanding Local Market Dynamics

Co-living performance varies dramatically by location. Institutional investors should prioritize markets with:

✅ Strong employment growth in sectors attracting young professionals

✅ Limited traditional rental supply (negative landlord instructions)

✅ Supportive planning policies for co-living and HMO development

✅ Established co-living presence indicating proven demand

✅ Excellent transport connectivity to employment centers

✅ Amenity-rich neighborhoods supporting the co-living lifestyle

According to recent RICS data, tenant demand has remained stable at +2% [2], but this masks significant regional variations. London, Manchester, and Birmingham show stronger co-living demand than smaller cities or suburban locations.

Financial Modeling Best Practices

Robust financial models are essential for Valuing Co-Living Spaces in Tenant Demand Surge: RICS Red Flags for 2026 Institutional Investments. Key modeling principles include:

Income assumptions:

- Use actual achieved rents, not asking prices

- Apply realistic occupancy rates based on operator track record

- Include seasonal variations where relevant

- Model tenant turnover costs explicitly

- Account for rent-free periods and incentives

Operating cost assumptions:

- Use operator-specific cost data where available

- Include all utilities, services, and amenities

- Model management fees realistically (15-25%)

- Provide for compliance and regulatory costs

- Include adequate maintenance and replacement reserves

Capital expenditure planning:

- Plan for 5-7 year refurbishment cycles

- Budget for regulatory compliance upgrades

- Include technology and security system updates

- Provide for communal area refreshment

- Model furniture and equipment replacement

Risk adjustments:

- Apply appropriate yield premiums for co-living (50-150 bps)

- Include liquidity discounts for smaller schemes

- Adjust for regulatory uncertainty

- Consider management transition risks

- Account for market cycle sensitivity

These modeling practices align with institutional investment standards and provide the transparency required for investment committee approvals.

Regulatory Landscape and Future Outlook for 2026

The regulatory environment for co-living and HMOs continues to evolve, creating both challenges and opportunities for institutional investors. Understanding these dynamics is crucial for accurate valuation and risk assessment.

Current Regulatory Framework

National regulations:

- Housing Act 2004 (HMO licensing requirements)

- Building Regulations (safety and habitability standards)

- Fire Safety Order 2005 (fire risk management)

- Energy Efficiency Regulations (minimum EPC ratings)

- Electrical Safety Standards (5-year inspection cycle)

Local authority powers:

- Mandatory HMO licensing (5+ occupants, 2+ households)

- Additional HMO licensing schemes (local discretion)

- Selective licensing schemes (broader rental controls)

- Article 4 directions (restricting HMO conversions)

- Planning use class requirements (C4 vs. Sui Generis)

The complexity of this regulatory landscape means that compliance status can vary dramatically between properties, even within the same local authority area. This creates significant valuation challenges and requires specialist knowledge.

Emerging Regulatory Trends

Several regulatory developments are likely to impact co-living valuations in 2026 and beyond:

1. Stricter fire safety requirements following building safety reforms

2. Enhanced energy efficiency standards (minimum EPC C by 2028 for new tenancies)

3. Expanded HMO licensing schemes in high-demand urban areas

4. Specific co-living planning use classes (potential new category)

5. Tenant rights enhancements affecting management costs and flexibility

Institutional investors should model the potential impact of these regulatory changes on both capital values and operating costs. Properties requiring significant compliance expenditure may see value reductions of 15-25% if remediation costs are substantial.

Market Outlook for Co-Living Investments

The fundamentals supporting co-living demand remain strong in 2026:

Positive drivers:

- Persistent rental supply shortage (landlord instructions at -27%) [2]

- Stable tenant demand (+2% net balance) [2]

- Expected rental price increases [2]

- Affordability advantages versus traditional rentals

- Lifestyle preferences of younger demographics

- Flexibility requirements in post-pandemic work environment

Challenges and headwinds:

- Regulatory complexity and compliance costs

- Limited comparable evidence for valuation

- Uncertain exit liquidity for investors

- Potential oversupply in some urban markets

- Economic uncertainty affecting tenant affordability

- Interest rate impacts on investment yields

The RICS January 2026 survey shows early signs of market recovery despite continued caution [1], suggesting that well-positioned co-living assets in strong locations should continue to perform. However, investors must be selective and rigorous in their due diligence.

Valuation Standards Evolution

RICS continues to refine valuation standards to address emerging asset classes like co-living. Surveyors should stay current with:

- Updated Red Book guidance on alternative residential assets

- Practice statements on HMO and co-living valuation

- Comparable evidence databases and benchmarking

- Professional development courses on specialist valuations

- Market intelligence reports on co-living sector performance

The RICS valuation standards [4] provide the foundational framework, but practical experience with co-living assets is essential for accurate valuations. Surveyors should consider specialist training and mentoring in this emerging sector.

Conclusion

Valuing Co-Living Spaces in Tenant Demand Surge: RICS Red Flags for 2026 Institutional Investments represents both a significant opportunity and a complex challenge for the real estate investment community. As tenant demand remains stable at +2% while landlord instructions plummet to -27% [2], co-living spaces offer an attractive solution to rental supply shortages in high-demand urban markets.

However, institutional investors and chartered surveyors must approach this asset class with appropriate caution and expertise. The five critical red flags—HMO compliance failures, inappropriate comparable evidence, overly optimistic occupancy assumptions, inadequate management cost provisions, and uncertain exit strategies—can each significantly impact valuations and investment returns.

Key Success Factors

Successful co-living investment requires:

🎯 Rigorous due diligence on compliance, licensing, and regulatory status

🎯 Hybrid valuation methodologies combining multiple comparable sources

🎯 Comprehensive stress-testing across multiple market scenarios

🎯 Experienced operator partnerships with proven track records

🎯 Active asset management focusing on compliance and performance

🎯 Realistic financial modeling with conservative assumptions

Actionable Next Steps

For Institutional Investors:

- Engage specialist surveyors with co-living valuation experience, such as registered RICS valuers familiar with multi-tenanted residential assets

- Conduct comprehensive due diligence on any prospective acquisitions, including legal, technical, and market analysis

- Implement robust stress-testing frameworks to understand downside risks

- Develop clear investment criteria focusing on location, compliance, and operator quality

- Build portfolio diversification across multiple markets and property types

For Chartered Surveyors:

- Enhance technical knowledge of HMO regulations and co-living operational models

- Build comparable evidence databases specific to co-living assets in your region

- Develop stress-testing templates for client reporting

- Establish professional networks with co-living operators and local authorities

- Pursue continuing professional development in specialist residential valuation

For Property Developers:

- Prioritize compliance from the design stage through to operation

- Document everything to support future valuations and disposals

- Engage early with planning authorities and licensing teams

- Design for flexibility to enable alternative uses if market conditions change

- Build quality to institutional standards from day one

The co-living sector will continue to evolve throughout 2026 and beyond, driven by persistent rental supply shortages and changing tenant preferences. Those who approach this market with appropriate expertise, rigorous analysis, and realistic expectations will find attractive investment opportunities. Those who underestimate the complexity and risks will likely face disappointing returns and potential losses.

The rental market fundamentals remain supportive, with RICS data showing stable demand and rising prices expected [1][2]. However, success in co-living investment depends on navigating the regulatory landscape, applying appropriate valuation methodologies, and maintaining institutional-quality standards throughout the investment lifecycle.

By understanding and addressing the RICS red flags outlined in this article, institutional investors can confidently participate in the co-living sector while managing risks appropriately. The key is combining financial discipline with operational excellence and regulatory compliance—a challenging but achievable combination for sophisticated investors working with experienced professional advisors.

References

[1] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution

[2] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[4] Valuation Standards – https://www.rics.org/profession-standards/rics-standards-and-guidance/sector-standards/valuation-standards