The South West property market finds itself at a crossroads in early 2026. While pockets of the UK housing sector show resilience and even growth, the South West region continues to trail behind national averages—a trend that has significant implications for property valuations, buyer confidence, and surveyor methodologies. Recent RICS (Royal Institution of Chartered Surveyors) residential market surveys reveal a complex picture: modest price growth expectations tempered by renewed economic uncertainty, yet accompanied by tentative improvements in buyer enquiries that suggest the worst may be behind us.

Understanding Valuation Surveys for South West Recovery Lag: RICS Adjustments for Modest Price Growth and Buyer Enquiry Uptick in Q1 2026 requires examining both the regional disparities emerging across the UK property landscape and the practical implications for homeowners, buyers, and property professionals navigating this cautious recovery phase.

Key Takeaways

- 📉 Regional divergence intensifies: The South West lags significantly behind Northern England, with price expectations more negative than the national headline average in Q1 2026

- 📊 Sentiment reversal in February: Price expectations fell sharply to -18% in February from -6% in January, reflecting renewed concerns over inflation and interest rates

- 🏠 Buyer enquiries remain subdued: New buyer enquiries dropped to -26% net balance in February, though 12-month sales expectations show resilience at +17%

- 🔍 Valuation methodology adjustments: Chartered surveyors are adapting risk assessment frameworks to account for elevated stock levels and cautious market sentiment

- 💡 Long-term optimism persists: Despite near-term weakness, +33% of respondents expect prices to edge higher over the next 12 months, requiring nuanced valuation approaches

Understanding the South West Recovery Lag in Q1 2026

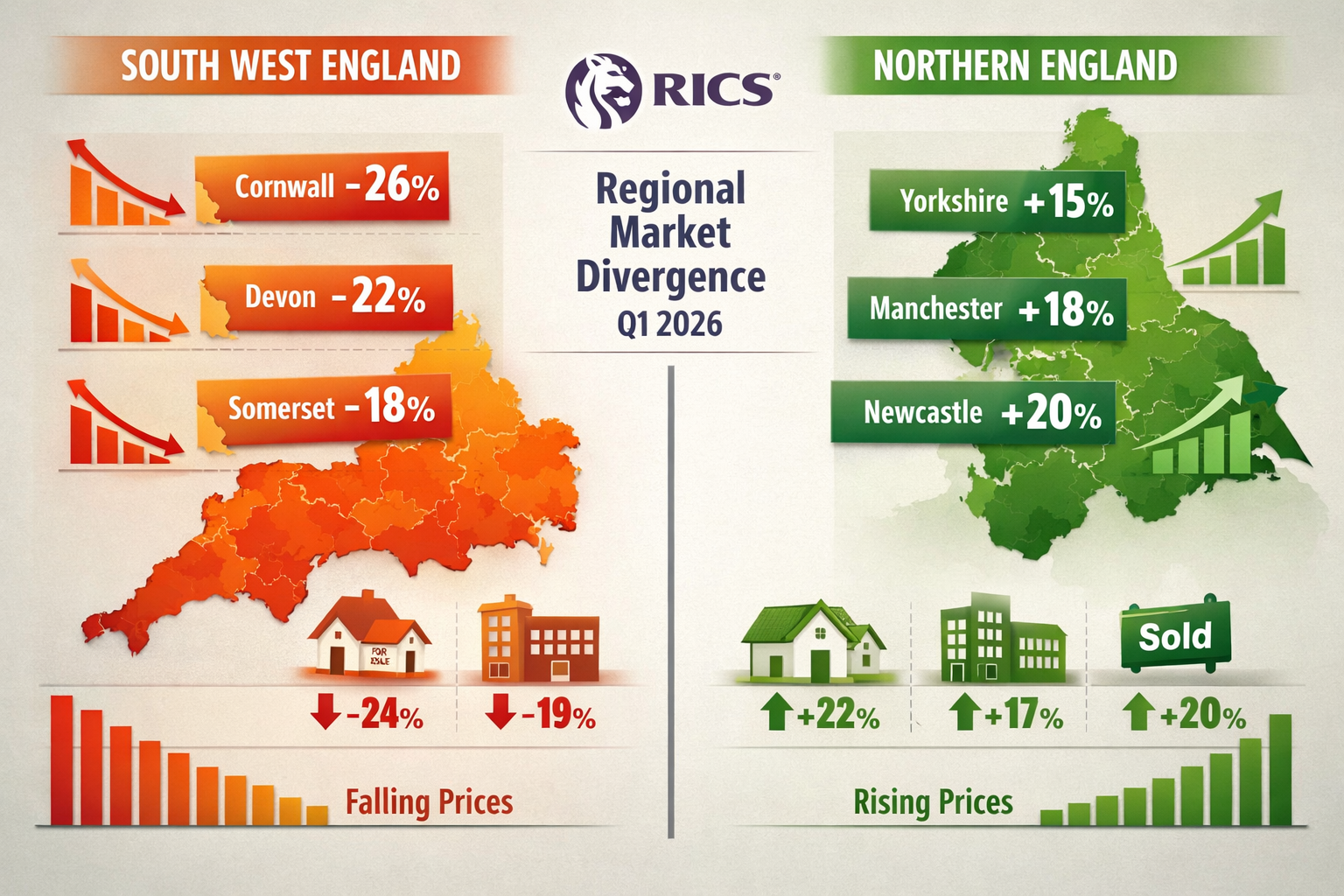

The South West property market recovery has consistently underperformed compared to other UK regions throughout the first quarter of 2026. According to RICS data, the South West—alongside London, the South East, and East Anglia—recorded price expectation net balances "more negative than the headline average" [1]. This regional weakness stands in stark contrast to the performance of Northern England, the North West, Northern Ireland, and Scotland, where prices have maintained an upward trajectory.

What's Driving the South West Slowdown?

Several interconnected factors explain why the South West continues to lag:

Economic uncertainty has hit harder in regions with higher average property values. The South West's traditionally premium market positioning means buyers face larger mortgage commitments precisely when interest rate volatility creates hesitation. The price expectations balance plummeted from -6% in January to -18% in February 2026, reflecting this renewed caution [3].

Stock levels remain elevated across the region, fundamentally shifting negotiating power toward buyers. RICS surveys indicate that inventory per surveyor branch sits at historically high levels, creating a buyer's market that suppresses price growth [2]. This oversupply situation requires careful consideration during property valuation processes.

Buyer demand weakened further in February, with new buyer enquiries falling to a -26% net balance from -15% in January [3]. This decline suggests that the early-year optimism seen in January—when +35% of participants anticipated increased sales activity—proved short-lived [1].

The agreed sales metric posted a net balance of -12% in February, demonstrating continued difficulty in converting viewings into completed transactions [3]. For property professionals conducting RICS building surveys, this sluggish transaction environment necessitates more conservative valuation approaches.

RICS Valuation Adjustments for Modest Price Growth Expectations

The modest price growth anticipated for the South West in 2026 requires chartered surveyors to recalibrate their valuation methodologies. Traditional approaches must now incorporate heightened risk factors and market-specific adjustments that reflect the region's lagging recovery trajectory.

Incorporating Regional Market Weakness

When conducting Level 2 Homebuyer Surveys in the South West, surveyors must now account for:

- Extended marketing periods: Properties are taking longer to sell, affecting comparable sales data and market value assessments

- Increased price negotiation: Buyers are achieving greater discounts from asking prices, requiring downward adjustments to initial valuations

- Stock competition: The elevated inventory levels mean individual properties face more direct competition, impacting value

Valuation factors have become more complex in 2026. While a net balance of +33% of respondents still expect prices to edge higher over 12 months [3], this optimism must be balanced against near-term weakness. Surveyors are increasingly adopting scenario-based valuation ranges rather than single-point estimates, providing clients with best-case, most-likely, and worst-case valuations that reflect market uncertainty.

Risk Assessment Framework Adjustments

The RICS valuation standards emphasize the importance of market conditions in determining property values. In Q1 2026, this means:

- Greater weight on recent comparables: Sales from the past 3 months receive priority over older data, given rapidly shifting sentiment

- Downward adjustments for market position: Properties in oversupplied micro-markets require specific negative adjustments

- Enhanced due diligence: RICS Building Surveys Level 3 become more critical as buyers seek detailed condition reports to justify negotiating positions

The dramatic sentiment reversal in London—where 12-month price expectations dropped from +56% in January to just +7% in February [3]—serves as a cautionary tale for South West valuers. Rapid shifts in market psychology can quickly render valuations outdated, necessitating more frequent revaluations and conservative assumptions.

Practical Valuation Methodology Changes

Chartered surveyors in the South West are implementing several practical adjustments:

| Valuation Element | Traditional Approach | Q1 2026 Adjustment |

|---|---|---|

| Comparable timeframe | 6-12 months | 3-6 months maximum |

| Market conditions adjustment | ±5% | ±10-15% |

| Marketing period assumption | 3-4 months | 5-7 months |

| Price negotiation buffer | 2-3% | 5-8% |

| Revaluation frequency | Annual | Quarterly or semi-annual |

These adjustments ensure that valuations reflect current market realities rather than outdated assumptions. For those seeking chartered surveyors in South West London and surrounding areas, understanding these methodology shifts is essential for informed decision-making.

Buyer Enquiry Uptick: Interpreting Mixed Signals in Q1 2026

Despite the overall negative sentiment, Valuation Surveys for South West Recovery Lag: RICS Adjustments for Modest Price Growth and Buyer Enquiry Uptick in Q1 2026 must account for nuanced positive developments. The resilience in 12-month sales expectations—with +17% of respondents anticipating increased activity [3]—suggests that market participants see current weakness as temporary rather than structural.

The January Optimism Peak

January 2026 represented a high-water mark for market confidence. A net balance of +35% of participants anticipated increased sales activity over the year ahead—the strongest reading since December 2024 [1]. This early-year optimism reflected:

- 💰 Hopes for interest rate stabilization

- 📈 Pent-up demand from 2025's subdued market

- 🏡 Seasonal factors as buyers traditionally re-enter the market after the holiday period

- 💼 Employment stability in key South West sectors

However, this optimism proved fragile. By February, renewed inflation concerns and geopolitical uncertainty had dampened sentiment significantly [3].

Understanding the Buyer Psychology Shift

The buyer enquiry patterns reveal important insights for valuation professionals:

Cautious engagement characterizes the current market. Buyers are conducting more extensive research, requesting more detailed surveys, and taking longer to commit. The price of valuation services has become a more significant consideration as buyers seek to minimize risk through comprehensive due diligence.

Negotiating leverage has shifted decisively toward buyers. With stock levels elevated and seller urgency increasing, buyers can afford to be selective. This dynamic requires valuers to consider not just the intrinsic property value but also the realistic transaction price achievable in current conditions.

Quality over quantity defines buyer behavior. While overall enquiry numbers remain negative, serious buyers are conducting more thorough investigations before making offers. This trend increases demand for different types of survey comparison information as buyers seek to understand which survey level best suits their needs.

Regional Contrasts: Northern Strength vs Southern Weakness

The stark contrast between Northern England's price growth and the South West's stagnation reflects fundamental market structure differences:

Northern markets benefit from:

- More affordable entry-level pricing

- Stronger first-time buyer activity

- Less exposure to interest rate sensitivity

- Tighter supply-demand balance in key cities

South West markets struggle with:

- Higher absolute prices creating affordability barriers

- Greater reliance on discretionary second-home buyers

- Oversupply in popular coastal and rural locations

- Demographic shifts as remote work flexibility normalizes

These regional dynamics require location-specific valuation adjustments. A property in Cornwall faces different market pressures than a comparable property in Manchester, necessitating distinct valuation methodologies despite similar physical characteristics.

Implications for Property Professionals and Homeowners

The Valuation Surveys for South West Recovery Lag: RICS Adjustments for Modest Price Growth and Buyer Enquiry Uptick in Q1 2026 landscape creates specific challenges and opportunities for different market participants.

For Sellers: Realistic Pricing is Critical

Homeowners considering selling in the South West must recognize that aspirational pricing strategies will fail in the current market. Key recommendations include:

✅ Obtain professional valuation: Engage local chartered surveyors familiar with micro-market conditions rather than relying on online estimates

✅ Price competitively from launch: Properties priced at or slightly below market value generate more enquiries and sell faster than those requiring multiple reductions

✅ Prepare comprehensive information: Buyers expect detailed property information, including recent surveys, energy performance certificates, and maintenance records

✅ Consider timing strategically: Monitor RICS monthly data for signs of sentiment improvement before listing

✅ Be prepared to negotiate: Build flexibility into your pricing strategy to accommodate the buyer's market dynamics

For Buyers: Enhanced Due Diligence Opportunities

The current market conditions favor thorough buyer investigation:

🔍 Invest in comprehensive surveys: The buyer's market justifies the cost of detailed RICS specialist defect surveys to identify issues for negotiation

🔍 Use survey findings strategically: Defects identified in surveys provide legitimate grounds for price renegotiation in the current environment

🔍 Take time with decisions: Reduced competition means less pressure to make rushed offers without proper investigation

🔍 Leverage market data: Reference RICS survey data in negotiations to justify offers below asking prices

🔍 Consider future value: Focus on properties with strong fundamentals that will appreciate when market conditions improve

For Chartered Surveyors: Adapting Professional Practice

Valuation professionals must evolve their practices to serve clients effectively in this uncertain environment:

Enhanced market commentary: Valuation reports should include detailed discussion of market conditions, regional trends, and confidence levels in the assessed value. Generic boilerplate language no longer suffices when market volatility is high.

Scenario analysis: Provide clients with value ranges reflecting different market trajectory assumptions. A property might be worth £450,000 in a stable market, £425,000 if weakness continues, and £475,000 if conditions improve—all legitimate valuations depending on assumptions.

Increased communication: Regular client updates about changing market conditions help manage expectations and build trust. Monthly RICS data releases provide natural touchpoints for client communication.

Professional development: Staying current with RICS guidance on valuation in uncertain markets ensures compliance with professional standards and best practices.

Technology integration: Utilize data analytics tools to track micro-market trends and identify comparable sales more efficiently, improving valuation accuracy.

Looking Ahead: What the Rest of 2026 May Hold

While near-term indicators remain mixed, several factors could influence the South West property market trajectory through the remainder of 2026:

Potential Positive Catalysts

Interest rate stabilization: If inflation pressures ease and the Bank of England signals a pause or reduction in rates, buyer confidence could recover quickly. The +33% net balance expecting price growth over 12 months [3] suggests latent optimism waiting for the right triggers.

Stock absorption: Elevated inventory levels will eventually normalize as sellers withdraw properties or accept market prices. This supply-side adjustment could stabilize pricing even without demand increases.

Seasonal factors: Spring and summer traditionally bring increased market activity. If the February weakness represents a seasonal low point, Q2 and Q3 could show improvement.

Economic resilience: The UK economy's ability to navigate current challenges without recession would support housing market stability, particularly in the South West's discretionary buyer segments.

Remaining Risk Factors

Geopolitical uncertainty: International tensions continue to create economic volatility that dampens consumer confidence and major purchase decisions.

Inflation persistence: If inflation proves more stubborn than anticipated, interest rates may remain elevated longer, prolonging affordability challenges.

Regional divergence widening: The gap between Northern growth and Southern weakness could widen further, creating a two-speed housing market with different valuation dynamics.

New vendor instructions remaining flat: The +1% net balance for new instructions in January [1] indicates sellers remain reluctant to enter the market, potentially constraining transaction volumes even if buyer demand improves.

Conclusion

The Valuation Surveys for South West Recovery Lag: RICS Adjustments for Modest Price Growth and Buyer Enquiry Uptick in Q1 2026 present a nuanced picture of a regional property market in transition. While the South West continues to underperform national averages, with price expectations and buyer enquiries remaining in negative territory, the market is not in freefall. Instead, it reflects a cautious recalibration following years of rapid growth, complicated by economic uncertainty and regional oversupply.

For property professionals, the key takeaway is the necessity of adapted valuation methodologies that account for heightened market volatility, regional disparities, and shifting buyer-seller dynamics. Generic approaches will produce unreliable results; instead, surveyors must employ conservative assumptions, recent comparables, and scenario-based analyses that acknowledge current uncertainties.

Homeowners and buyers should recognize that current conditions, while challenging, also create opportunities. Sellers who price realistically and present properties professionally can still achieve successful transactions. Buyers who conduct thorough due diligence through comprehensive surveys can negotiate favorable terms and acquire properties with strong long-term fundamentals.

The resilience in 12-month expectations—with significant net balances still anticipating price growth and increased sales activity—suggests that market participants view current weakness as temporary. However, the path to recovery will likely be gradual rather than dramatic, requiring patience and realistic expectations from all parties.

Actionable Next Steps

For property sellers:

- Obtain a professional RICS valuation before listing

- Research recent comparable sales in your immediate area

- Prepare property documentation and maintenance records

- Consider timing your sale strategically based on market data

For property buyers:

- Commission comprehensive surveys on properties of interest

- Use survey findings to negotiate effectively

- Monitor RICS monthly data for market trend insights

- Focus on properties with strong fundamentals for long-term value

For property professionals:

- Review and update valuation methodologies quarterly

- Enhance market commentary in valuation reports

- Maintain regular client communication about market changes

- Invest in continuing professional development on uncertain market valuation

The South West property market of 2026 demands informed, strategic decision-making based on current data rather than historical assumptions. By understanding the regional recovery lag, adapting valuation approaches, and interpreting mixed buyer enquiry signals accurately, market participants can navigate this challenging environment successfully and position themselves for the recovery that longer-term indicators suggest lies ahead.

References

[1] UK Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[2] UK Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[3] UK Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026