The landscape of high-value property ownership in the UK is undergoing a dramatic transformation. As new tax measures targeting properties valued over £2 million take effect between 2026 and 2028, chartered surveyors face unprecedented challenges in delivering accurate valuations for wealthy clients. The Valuation Impacts of 2026 Budget Taxes on £2M+ Properties: Surveyor Strategies for High-End Clients represent a critical area of professional expertise that will shape transactional behavior and investment decisions across the luxury property market for years to come.

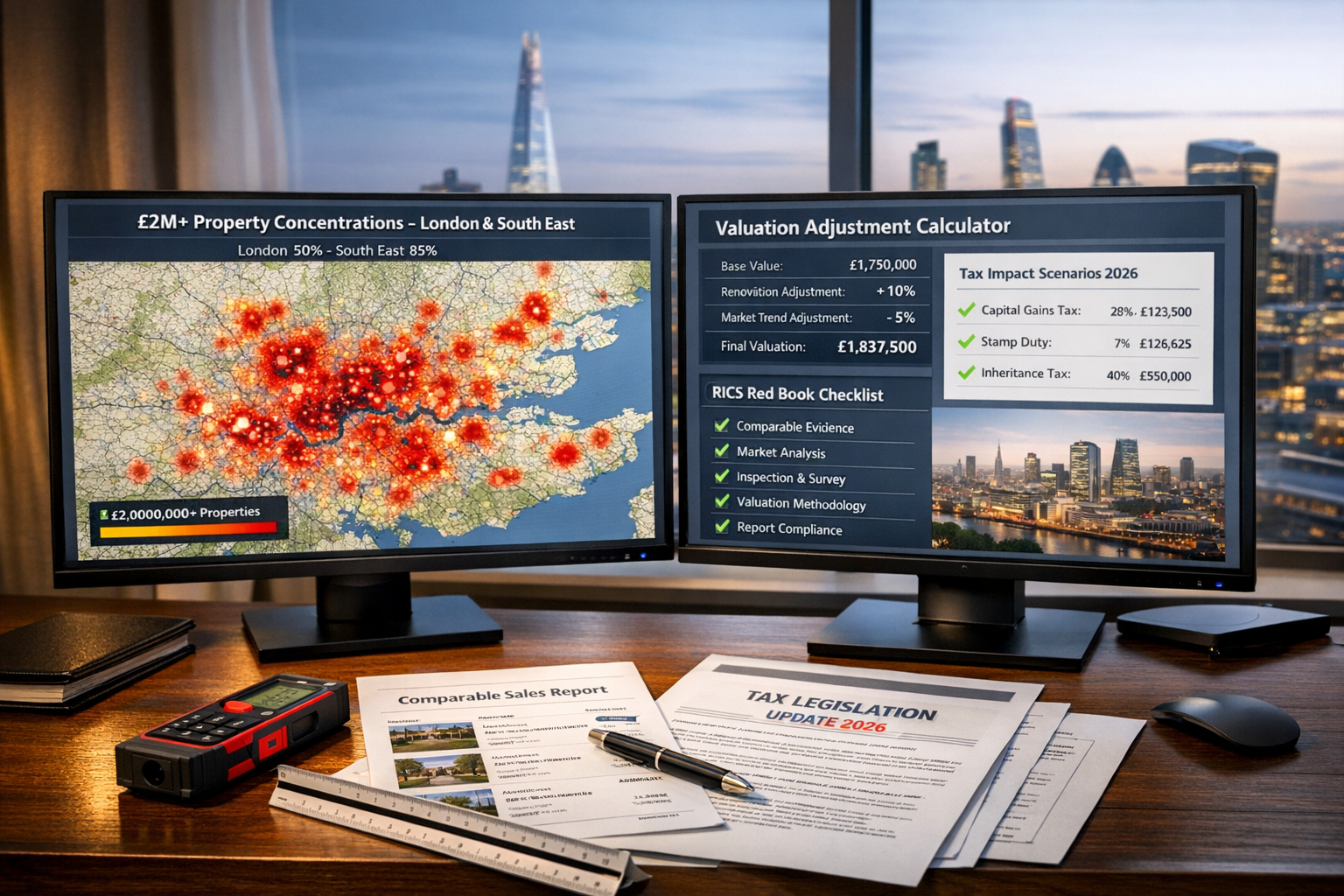

With over 100,000 households expected to be affected by the forthcoming mansion tax[2], and 50% of all properties valued over £2 million concentrated in London alone[2], surveyors must adapt their methodologies to account for complex tax implications that fundamentally alter net ownership costs and investment returns.

Key Takeaways

- 🏛️ New mansion tax from April 2028 will add £2,500-£7,500 annually to properties over £2 million, directly impacting valuations and buyer behavior

- 📊 Inheritance tax relief caps at £2.5 million per person from April 2026 create strategic valuation thresholds for estate planning

- 💷 Tax rate increases across dividends, property income, and capital gains compound the financial burden on high-net-worth property owners

- 📉 Market behavior shifts already evident, with 83% of offers on near-£2M properties coming in below the threshold in February 2026

- 🎯 RICS-aligned adjustment techniques are essential for surveyors to accurately reflect tax-adjusted market values in formal reports

Understanding the 2026-2028 Tax Framework for High-Value Properties

The UK government has introduced a comprehensive suite of tax measures specifically targeting properties and assets valued above £2 million. These changes fundamentally alter the economics of luxury property ownership and require surveyors to understand their cascading effects on market valuations.

The Mansion Tax Structure

From April 2028, properties in England valued over £2 million will face annual charges ranging from £2,500 to £7,500, depending on property value[2]. This tax will be added to council tax bills and payable by the property owner rather than occupiers or tenants.

The tiered structure creates distinct valuation bands:

| Property Value | Annual Mansion Tax | Effective Annual Cost Increase |

|---|---|---|

| £2M – £3M | £2,500 | 0.125% – 0.083% of value |

| £3M – £5M | £5,000 | 0.167% – 0.100% of value |

| Over £5M | £7,500 | 0.150%+ of value |

This represents a significant ongoing cost that reduces net returns for investors and increases the total cost of ownership for residential occupiers. Surveyors conducting capital gains tax valuation work must factor these recurring charges into their market value assessments.

Inheritance Tax Relief Restrictions

Perhaps the most significant change for high-net-worth families is the capping of Agricultural Property Relief (APR) and Business Property Relief (BPR) at £2.5 million per person for 100% relief from 6 April 2026[1]. Above this threshold, only 50% relief applies, resulting in an effective 20% inheritance tax charge on excess amounts.

Couples can strategically transfer unused allowances to pass up to £5 million tax-free, with excess amounts payable interest-free over 10 years[3]. This creates critical valuation thresholds at £2.5 million and £5 million that surveyors must consider when preparing probate valuation reports.

Property Income and Dividend Tax Increases

From April 2027, property income tax rates will rise by 2% across all brackets—to 22% (basic rate), 42% (higher rate), and 47% (additional rate)—estimated to raise £500 million annually[2]. This directly impacts landlords holding high-value residential properties.

Additionally, from April 2026, dividend tax rates increase by 2 percentage points: basic rate to 10.75%, higher rate to 35.75%, and additional rate remains at 39.35%[1][3]. Many high-net-worth property owners structure their holdings through corporate vehicles and receive dividend income, making this change particularly relevant.

Valuation Impacts of 2026 Budget Taxes on £2M+ Properties: Market Behavior Changes

The psychological and practical impacts of the £2 million threshold have already manifested in measurable market behavior changes. Understanding these patterns is essential for surveyors developing accurate comparable evidence and market value opinions.

Strategic Purchasing Below Threshold

In February 2026, 83% of property offers on homes priced within 10% of £2 million came in below the £2M mark, compared to just 64% a year earlier[2]. This represents a dramatic shift in transactional patterns among high-net-worth buyers actively seeking to avoid crossing the tax threshold.

This clustering effect creates several challenges for surveyors:

- Distorted comparable evidence near the £2 million threshold

- Artificial price compression for properties naturally valued between £1.9M-£2.1M

- Valuation gaps where properties slightly above £2M struggle to find buyers

- Negotiation leverage shifts favoring buyers as sellers face limited demand above threshold

When conducting commercial property valuations or high-end residential appraisals, chartered surveyors must carefully analyze whether comparable transactions reflect genuine market value or tax-avoidance positioning.

Geographic Concentration of Impact

Approximately 50% of all properties in England valued over £2 million are in London, and 85% are in the South East[2]. This geographic concentration creates regional market dynamics that surveyors must understand:

London hotspots such as Chelsea, Kensington, Mayfair, and Hampstead will see the most significant impacts. Chartered surveyors in Chelsea and chartered surveyors in Central London are already adapting their methodologies to account for tax-driven market shifts.

Outer London and Home Counties areas including Richmond, Esher, Weybridge, and Guildford also contain substantial concentrations of affected properties. Professionals such as chartered surveyors in Richmond, chartered surveyors in Esher, and chartered surveyors in Guildford must develop specialized expertise in tax-adjusted valuations.

Capital Gains Tax Implications

CGT rates have increased from 14% to 18% where Business Asset Disposal Relief or Investors' Relief applies[1][3]. For property investors disposing of high-value assets, this represents a significant additional cost that reduces net proceeds and influences pricing decisions.

Surveyors preparing valuations for potential sales must consider how increased CGT liability affects seller motivation and pricing flexibility, particularly for properties held in corporate structures or as business assets.

Valuation Impacts of 2026 Budget Taxes on £2M+ Properties: RICS-Aligned Adjustment Techniques

Chartered surveyors must employ rigorous, defensible methodologies when adjusting valuations to reflect tax impacts. The RICS Red Book provides the framework, but practical application requires nuanced judgment and clear documentation.

Capitalization of Recurring Tax Costs

The annual mansion tax represents a permanent reduction in net ownership benefits. Surveyors can capitalize this recurring cost using appropriate yield rates to calculate the impact on capital value.

Example calculation:

- Property natural value: £2.5 million

- Annual mansion tax: £2,500

- Appropriate capitalization rate: 4% (reflecting long-term gilt yields plus risk premium)

- Capitalized tax burden: £2,500 ÷ 0.04 = £62,500

- Tax-adjusted market value: £2,500,000 – £62,500 = £2,437,500

This approach recognizes that rational purchasers will discount the purchase price to reflect the permanent annual cost. The appropriate capitalization rate should reflect:

- Current interest rate environment

- Property-specific risk factors

- Market liquidity and demand depth

- Purchaser financing costs

Threshold Proximity Adjustments

Properties valued close to the £2 million threshold require special consideration. The clustering effect creates artificial price compression that surveyors must analyze carefully.

Adjustment framework:

- Properties £1.8M-£2.0M: Likely to benefit from increased demand from threshold-avoiding buyers; may support slight premium over pre-tax comparable evidence

- Properties £2.0M-£2.2M: Face significant downward pressure as buyers negotiate to stay below threshold; require material negative adjustment

- Properties £2.2M-£3.0M: Experience "no man's land" effect where buyers perceive limited value in paying premium over threshold without substantial additional benefits

Surveyors must document their reasoning clearly, referencing specific comparable transactions and market evidence. Understanding valuation factors becomes even more critical in this distorted market environment.

Investment Property Yield Adjustments

For rental properties valued over £2 million, surveyors must adjust capitalization rates to reflect:

- Reduced net rental income from April 2027 property income tax increases (2% across all bands)

- Annual mansion tax burden reducing net returns

- Increased CGT liability on eventual disposal (18% vs. previous 14%)

Example investment property analysis:

- Gross rental income: £120,000 per annum

- Property value: £2.4 million

- Gross yield: 5.0%

Pre-tax net yield calculation:

- Rental income after higher-rate tax (42%): £69,600

- Less mansion tax: £2,500

- Net income: £67,100

- Net yield: 2.80%

Post-tax net yield calculation (2027+):

- Rental income after higher-rate tax (44% including 2% increase): £67,200

- Less mansion tax: £2,500

- Net income: £64,700

- Net yield: 2.70%

This 10-basis-point yield compression suggests a capital value reduction of approximately 2-3% for investment properties, depending on market conditions and alternative investment returns.

Estate Planning Valuation Strategies

For probate valuation and estate planning purposes, surveyors must consider the £2.5 million and £5 million inheritance tax relief thresholds.

Strategic considerations:

- Property portfolio segmentation: Valuing individual properties within estates to optimize relief utilization

- Timing of valuations: Market value dates can significantly impact tax liability given the April 2026 implementation

- Spousal transfer planning: Couples can effectively double the £2.5M threshold to £5M through strategic planning

- 10-year payment terms: The interest-free payment option for excess amounts affects present value calculations

Surveyors should work closely with tax advisors and solicitors to ensure valuations support optimal estate planning structures while maintaining RICS compliance and professional independence.

Surveyor Strategies for High-End Clients: Practical Implementation

Professional surveyors serving high-net-worth clients must adapt their service delivery, communication, and technical approaches to address the complex tax environment.

Enhanced Client Communication

Wealthy clients expect surveyors to understand not just property values but the broader financial context. Effective communication strategies include:

✅ Tax impact summaries alongside valuation figures

✅ Scenario modeling showing values at different tax thresholds

✅ Comparable analysis highlighting tax-driven market distortions

✅ Timeline planning for transactions relative to tax implementation dates

✅ Referral coordination with tax advisors, solicitors, and wealth managers

Specialized Valuation Reports

Standard valuation templates may not adequately address tax-adjusted market values. Enhanced reports should include:

Executive Summary Section:

- Clear statement of tax-adjusted market value

- Comparison to pre-tax market value

- Key tax assumptions and implementation dates

Market Context Analysis:

- Discussion of threshold clustering effects

- Geographic market dynamics

- Transaction volume and pricing trends near £2M threshold

Methodology Disclosure:

- Detailed explanation of capitalization approaches

- Yield adjustment calculations

- Comparable evidence selection rationale

- Sensitivity analysis showing value ranges under different assumptions

When preparing ATED valuation reports or other specialist tax-related valuations, surveyors should explicitly address how 2026-2028 tax changes affect the specific valuation purpose.

Technology and Data Analytics

Leading surveyors are leveraging technology to analyze tax impacts more effectively:

- Automated tax calculators integrated into valuation software

- Market data analytics tracking threshold clustering patterns

- Comparable transaction databases with tax-adjusted pricing filters

- Client portals providing interactive scenario modeling

Understanding the price of valuation services should reflect the additional complexity and expertise required for tax-adjusted high-value property assessments.

Regional Expertise Development

Given the geographic concentration of affected properties, surveyors should develop deep regional expertise. This includes:

- Local market intelligence networks with estate agents, solicitors, and wealth advisors

- Submarket analysis within high-value areas (e.g., specific London boroughs or Home Counties towns)

- Historical transaction databases tracking pricing patterns over multiple market cycles

- Relationship development with high-net-worth client communities

Firms operating across multiple regions—such as chartered surveyors in London, chartered surveyors in Berkshire, and chartered surveyors in Buckinghamshire—should ensure consistent methodologies while recognizing local market nuances.

Continuing Professional Development

The rapidly evolving tax landscape requires ongoing education. Surveyors should pursue:

- Tax legislation updates through RICS and professional tax bodies

- Case study analysis of complex valuation scenarios

- Peer review processes to validate methodologies

- Cross-disciplinary learning with tax advisors and financial planners

- Expert witness training for potential dispute resolution roles

Council Tax Revaluation and Implementation Challenges

A critical practical concern is whether the infrastructure exists to implement the mansion tax effectively. Paula Higgins, CEO of HomeOwners Alliance, has raised concerns about whether "the revaluation needed for this mansion tax can be delivered cleanly and on time"[2].

Valuation Accuracy Concerns

The last comprehensive council tax revaluation in England occurred in 1991, creating a 35-year gap. Implementing a tax based on current market values requires:

- Mass property revaluation of potentially millions of properties

- Appeals infrastructure to handle disputes

- Valuation methodology consistency across regions and property types

- Regular revaluation cycles to maintain accuracy

Surveyors may find themselves involved in appeals processes, requiring expertise in both market valuation and administrative law procedures. Those with expert witness experience will be particularly valuable.

Scotland's Divergent Approach

Scotland is introducing new council tax bands for properties above £1 million and £2 million from April 2028[3], creating divergent tax regimes across the UK. Surveyors operating in both jurisdictions must understand:

- Different threshold levels and band structures

- Separate implementation timelines

- Cross-border valuation implications for properties near the England-Scotland border

- Client relocation considerations driven by tax differentials

Strategic Planning for Property Transactions

High-net-worth clients require sophisticated advice on timing and structuring property transactions to optimize tax outcomes.

Pre-2028 Transaction Timing

For sellers of properties valued over £2 million, completing transactions before April 2028 allows purchasers to avoid immediate mansion tax liability. This creates:

- Potential pricing premiums for properties transacting in 2026-2027

- Compressed transaction timelines as buyers rush to complete before implementation

- Negotiation leverage shifting between buyers and sellers based on timing

Surveyors should provide clear guidance on how transaction timing affects market value and negotiation dynamics.

Purchase Structuring Options

Wealthy buyers are exploring various structures to minimize tax exposure:

Corporate ownership: Holding property through corporate vehicles may offer tax planning opportunities but triggers different tax regimes (ATED, SDLT surcharges)

Portfolio segmentation: Purchasing multiple properties below £2M rather than single high-value properties

Mixed-use properties: Structuring properties with commercial elements to potentially reduce residential valuation

Leasehold vs. freehold: Different ownership structures may have varying tax implications

Surveyors must understand these structures and provide appropriate valuations for each scenario. Those with experience in freehold valuation and commercial property work will find their expertise increasingly valuable.

Renovation and Development Considerations

For properties close to the £2 million threshold, owners face difficult decisions about renovations and improvements:

- Value enhancement projects that push properties over the threshold may not be economically rational

- Deferred maintenance may become more common as owners avoid triggering higher tax bands

- Development feasibility calculations must incorporate tax step-changes at thresholds

Surveyors conducting reinstatement cost valuations or development appraisals must factor these considerations into their advice.

Future-Proofing Valuation Practices

The 2026-2028 tax changes represent just one phase in an evolving regulatory landscape. Forward-thinking surveyors should prepare for ongoing changes.

Scenario Planning and Sensitivity Analysis

Valuation reports should include sensitivity analysis showing how values might change under different scenarios:

- Further tax increases or threshold adjustments

- Market correction scenarios affecting base property values

- Interest rate changes affecting capitalization rates

- Regulatory changes to tax relief provisions

This approach provides clients with a range of potential outcomes rather than single-point estimates, supporting more informed decision-making.

Building Multidisciplinary Networks

The complexity of tax-adjusted valuations requires collaboration across professions. Successful surveyors will build strong networks with:

- Tax advisors specializing in high-net-worth clients

- Estate planning solicitors handling complex inheritance structures

- Wealth managers coordinating overall financial strategies

- Specialist accountants with property tax expertise

- Independent financial advisors serving affluent clients

These relationships enable surveyors to provide holistic advice while maintaining appropriate professional boundaries.

Advocacy and Industry Leadership

Professional bodies including RICS play a crucial role in ensuring valuation methodologies keep pace with tax changes. Individual surveyors can contribute through:

- Participating in working groups developing guidance on tax-adjusted valuations

- Publishing case studies sharing practical approaches to complex scenarios

- Engaging with policymakers to highlight implementation challenges

- Mentoring junior professionals to build expertise across the profession

Conclusion

The Valuation Impacts of 2026 Budget Taxes on £2M+ Properties: Surveyor Strategies for High-End Clients represent a fundamental shift in how chartered surveyors approach high-value property assessments. The combination of mansion tax charges from April 2028, inheritance tax relief caps from April 2026, and multiple rate increases across property income, dividends, and capital gains creates a complex web of financial considerations that directly affect market values.

Surveyors must move beyond traditional comparable analysis to incorporate sophisticated tax capitalization techniques, threshold proximity adjustments, and investment yield recalculations. The evidence is clear: buyer behavior has already shifted dramatically, with 83% of offers on near-£2M properties now coming in below the threshold[2]. This market distortion will only intensify as implementation dates approach.

Actionable next steps for surveyors serving high-end clients:

- Enhance technical capabilities by developing robust methodologies for capitalizing recurring tax costs and adjusting for threshold effects

- Strengthen client communication by providing clear tax impact summaries alongside traditional valuation figures

- Build multidisciplinary networks with tax advisors, solicitors, and wealth managers to deliver comprehensive advice

- Invest in regional expertise particularly in London and the South East where 85% of affected properties are concentrated[2]

- Pursue continuing education on evolving tax legislation and valuation techniques through RICS and specialist programs

- Develop specialized report templates that explicitly address tax-adjusted market values with clear methodology disclosure

The surveyors who successfully navigate this new landscape will differentiate themselves through technical excellence, clear communication, and genuine understanding of their clients' broader financial objectives. As over 100,000 households face these new tax burdens[2], demand for expert guidance will only grow.

For professional valuation services that incorporate comprehensive tax impact analysis, consider consulting with experienced chartered surveyors who understand the nuances of high-value property taxation and can provide RICS-compliant reports that support informed decision-making in this complex environment.

References

[1] Uk Tax Landscape Key Changes For 2026 – https://taxscape.deloitte.com/article/uk-tax-landscape–key-changes-for-2026.aspx

[2] New Property Tax – https://hoa.org.uk/news/new-property-tax/

[3] Whats Changing In The 2026 27 Tax Year And Why It Matters – https://amberriver.com/tax-planning/whats-changing-in-the-2026-27-tax-year-and-why-it-matters/