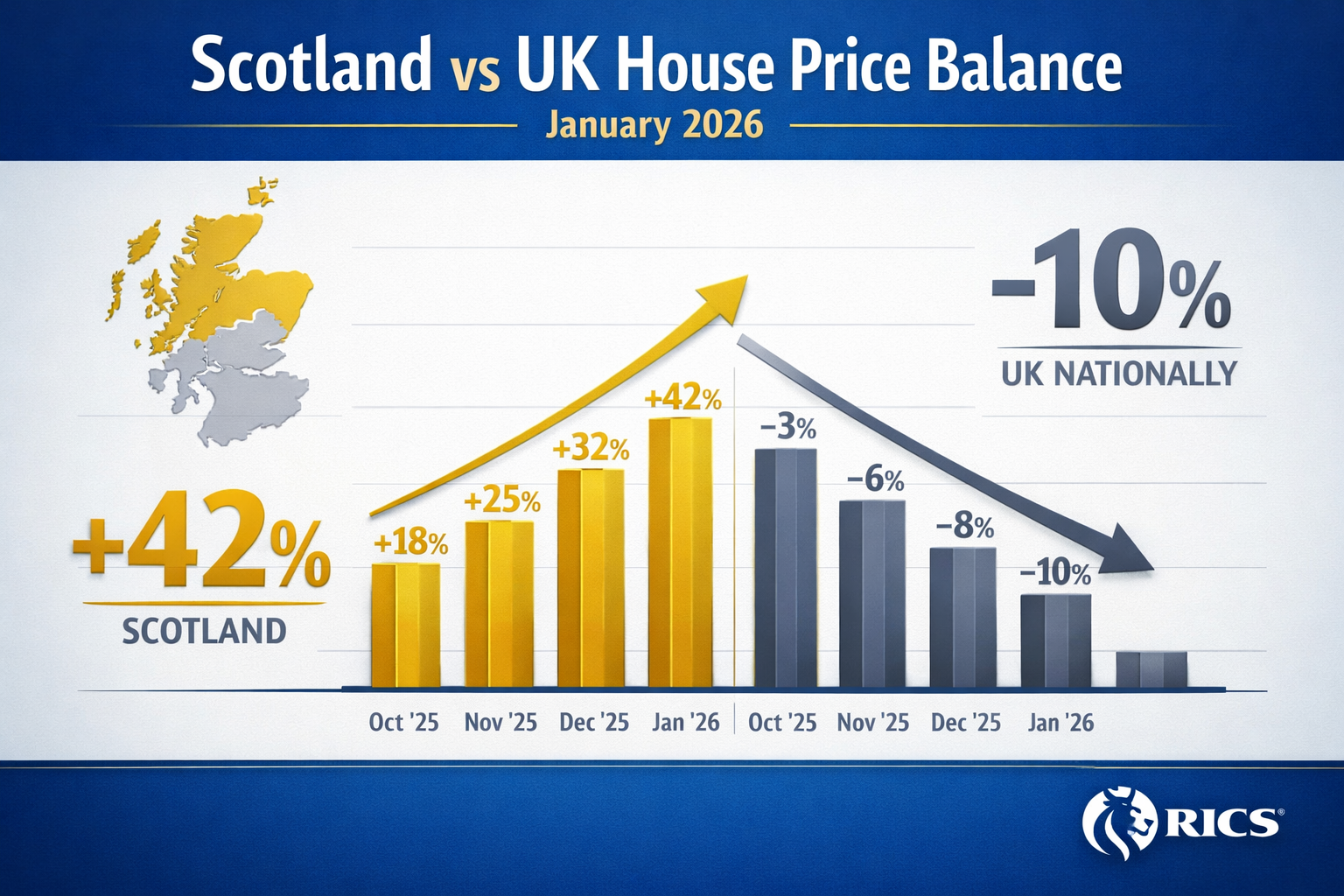

Scotland's property market has emerged as the unexpected champion of the UK's 2026 housing recovery, with RICS surveyors reporting a remarkable +42% net balance in house price growth during January—a stark contrast to the national figure of -10%. This dramatic regional divergence demands immediate attention from property professionals, as traditional valuation methodologies struggle to keep pace with Scotland's accelerating market dynamics. The Valuation Adjustments for Scotland's 2026 House Price Leadership: RICS Strategies Outpacing National Recovery represent a fundamental shift in how chartered surveyors must approach property assessment in a market that's defying broader UK trends.

As buyer enquiries surge and sales expectations reach their highest levels in over a year, registered RICS valuers face the challenge of accurately pricing properties in a rapidly appreciating environment while maintaining professional standards and protecting client interests. 🏴

Key Takeaways

- Scotland's house price balance reached +42% in January 2026, representing the strongest regional performance in nearly a year and significantly outpacing the UK national average of -10%[1]

- Buyer enquiries increased by a net balance of +21% among Scottish surveyors, signaling renewed purchaser confidence while most UK regions experienced declining interest[1]

- Forward sales expectations remain exceptionally strong, with 46% of Scottish respondents anticipating higher sales volumes in Q1 2026 and 34% expecting continued growth through Q2[2]

- Property listings surged by +27% in January 2026, marking a meaningful uplift that addresses previous supply constraints and supports sustainable price growth[1]

- Long-term price forecasts show 62% of Scottish surveyors expect higher values in 12 months, requiring valuation adjustments that account for sustained regional outperformance[1]

Understanding Scotland's 2026 Market Leadership Position

The RICS Data Reveals Unprecedented Regional Divergence

The January 2026 RICS Residential Market Survey unveiled a housing market story that few analysts predicted: Scotland has decisively separated itself from the broader UK property malaise. While England, Wales, and Northern Ireland grappled with falling buyer interest and stagnant prices, Scottish surveyors reported metrics that suggested a fundamentally different economic reality.

The +42% net balance for house prices in Scotland represents more than just a statistical anomaly—it signals a structural shift in regional property dynamics that demands new valuation approaches. This figure means that 42% more surveyors reported rising prices than falling ones, a margin that hasn't been seen in the UK as a whole since the post-pandemic boom of 2021-2022[1].

| Key Metric | Scotland (Jan 2026) | UK National (Jan 2026) | Difference |

|---|---|---|---|

| House Price Balance | +42% | -10% | +52 percentage points |

| Buyer Enquiries | +21% | Declining | Significant outperformance |

| New Instructions | +27% | Modest growth | Strong supply increase |

| 3-Month Sales Forecast | +46% | Cautious | Exceptional optimism |

Economic Factors Driving Scottish Outperformance

Several interconnected factors explain why Scotland has become the UK's 2026 property market leader:

Affordability advantages continue to attract buyers from higher-priced southern markets. The average Scottish property price remains substantially below London and Southeast England levels, creating opportunities for both first-time buyers and investors seeking better value propositions.

Employment resilience in key Scottish cities has supported housing demand. Edinburgh's financial services sector and Glasgow's diversified economy have weathered recent economic headwinds better than many UK regions, maintaining wage growth that supports mortgage affordability[4].

Supply-demand rebalancing has occurred at an opportune moment. The +27% increase in new instructions to sell in January 2026 arrived precisely when buyer interest was accelerating, creating a healthy market dynamic rather than the supply gluts or shortages that plague other regions[1].

Interest rate expectations have shifted favorably. Scottish buyers appear more confident that the Bank of England's monetary policy trajectory will support mortgage affordability throughout 2026, encouraging purchase decisions that were deferred in 2025[2].

Valuation Adjustments for Scotland's 2026 House Price Leadership: Methodological Implications

Adapting Comparative Market Analysis for Rapid Appreciation

Traditional methods of valuation rely heavily on recent comparable sales, but Scotland's accelerating market creates significant challenges for this approach. When prices are rising at +42% net balance, comparable transactions from even three months ago may substantially undervalue current market conditions.

RICS-qualified professionals must now implement several critical adjustments:

Time-adjusted comparables require more aggressive modification factors. Where a surveyor might typically apply a 0.5-1% monthly adjustment for modest appreciation, Scotland's 2026 market may justify 1.5-2.5% monthly adjustments when using sales from late 2025 as comparables[3].

Forward-looking valuation components must be carefully integrated. With 62% of Scottish surveyors expecting higher prices in 12 months, registered RICS valuers conducting mortgage valuations must balance current market evidence with reasonable expectations of continued appreciation—without creating inflated valuations that expose lenders to risk[1].

Geographic micro-market analysis becomes essential. Scotland's outperformance isn't uniform across all property types and locations. Edinburgh's New Town Georgian properties may be appreciating at different rates than Glasgow's West End tenements or Aberdeen's suburban developments, requiring granular local market knowledge.

Risk-Adjusted Valuation Frameworks for Regional Outperformance

The Valuation Adjustments for Scotland's 2026 House Price Leadership: RICS Strategies Outpacing National Recovery must acknowledge that rapid regional appreciation carries inherent risks that professional valuers have a duty to consider.

Sustainability analysis should form part of every valuation report. Surveyors must assess whether Scotland's price growth is supported by fundamental economic factors (employment, wages, demographics) or whether it represents speculative momentum that could reverse if broader UK conditions deteriorate[5].

Scenario-based valuation ranges provide clients with more complete information. Rather than a single point estimate, valuers might present a range that accounts for:

- Base case: Continued Scottish outperformance at current trajectory

- Moderate case: Convergence toward UK national average over 12-24 months

- Adverse case: Sharp correction if economic conditions deteriorate

Liquidity considerations must be explicitly addressed. A property valued at £350,000 in a rapidly appreciating market may be accurate today, but if market conditions shift, the actual achievable sale price could differ significantly. Valuation reports should clearly state assumptions about market liquidity and transaction timelines.

Specialized Valuation Contexts Requiring Enhanced Scrutiny

Certain valuation scenarios demand particular attention in Scotland's 2026 market environment:

Mortgage lending valuations must balance optimism with prudence. While lenders want to capture legitimate market appreciation, they also need protection against potential corrections. RICS standards require valuers to provide market value rather than investment value, meaning the price a willing buyer would pay to a willing seller in an arm's-length transaction—not the highest possible price in a heated market[3].

Help to Buy and shared equity schemes present unique challenges. Government-backed programs often use valuations to determine equity shares, and rapid appreciation can create significant financial implications for both buyers and government. Accurate Help to Buy valuations must reflect true market conditions while adhering to scheme-specific guidelines.

Probate and tax valuations require particular care. Capital gains tax valuations and inheritance tax assessments must be defensible to HMRC, which may scrutinize valuations in rapidly appreciating markets to ensure taxpayers aren't understating gains or estate values.

Leasehold and freehold valuations become more complex when underlying property values are rising rapidly. Lease extension valuations and freehold valuations must account for changing property values while applying statutory formulas that may not fully capture market dynamics.

RICS Professional Standards and Scottish Market Adaptation

Red Book Compliance in Outperforming Markets

The RICS Valuation – Global Standards (the "Red Book") provides the framework that all chartered surveyors must follow, but applying these standards in Scotland's 2026 market requires thoughtful interpretation and enhanced professional judgment.

Basis of value clarity becomes paramount. The Red Book defines market value as "the estimated amount for which an asset should exchange on the valuation date between a willing buyer and a willing seller in an arm's length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion"[3].

In Scotland's current environment, determining what constitutes "proper marketing" and whether buyers are acting "prudently" requires careful analysis. Are buyers paying premium prices because of genuine market strength, or because of fear of missing out (FOMO) that may not represent sustainable value?

Assumptions and special assumptions must be explicitly stated and justified. If a valuer assumes that Scotland's outperformance will continue, this assumption should be clearly documented with supporting evidence. Conversely, if a valuer assumes convergence toward UK national trends, this too requires justification[3].

Departure provisions may occasionally be necessary. In exceptional circumstances where strict Red Book compliance would produce a misleading result, valuers can depart from specific requirements—but only with explicit client agreement, clear documentation, and compelling justification.

Quality Assurance and Peer Review Considerations

Given the high-stakes nature of valuations in rapidly appreciating markets, enhanced quality assurance processes become essential:

✅ Peer review protocols should be implemented for valuations above certain thresholds or for particularly complex properties. A second RICS-qualified surveyor reviewing methodology and conclusions can identify potential biases or errors.

✅ Market evidence databases must be continuously updated. Firms operating in Scotland should maintain comprehensive databases of comparable transactions, updated weekly or even daily during periods of rapid change.

✅ Client communication standards should emphasize market volatility and valuation uncertainty. Clients need to understand that valuations are point-in-time assessments and that market conditions can change rapidly.

✅ Professional indemnity insurance considerations require attention. Valuers should ensure their coverage adequately protects against claims arising from valuations in volatile markets and consider whether policy terms require notification of heightened risk environments.

Strategic Implications for Property Professionals and Stakeholders

For Buyers and Sellers: Navigating the Scottish Advantage

Buyers entering Scotland's market in 2026 face a challenging environment where competition is intensifying and prices are rising. However, the improved supply position (with new instructions up 27%) suggests that patient buyers who work with knowledgeable professionals can still find opportunities[1].

Key buyer strategies include:

- Pre-approval and financial readiness: In a market where 46% of surveyors expect rising sales in the coming quarter, buyers with mortgage approval and available funds have significant advantages[2]

- Professional survey investment: Given rapid appreciation, comprehensive RICS building surveys become even more valuable to ensure purchase prices reflect actual property condition

- Long-term perspective: With 62% of surveyors expecting higher prices in 12 months, buyers should focus on long-term suitability rather than attempting to time short-term market movements[1]

Sellers benefit from Scotland's leadership position but must still price realistically. Overpricing based on optimistic projections can result in extended marketing periods and eventual price reductions that undermine negotiating position.

Effective seller approaches include:

- Professional valuation: Obtaining a formal valuation from registered RICS valuers provides objective pricing guidance based on current market evidence

- Timing considerations: With new instructions rising sharply, sellers who list promptly can capture demand before supply increases further

- Property presentation: In a strengthening market, well-presented properties command premium prices and sell more quickly

For Lenders and Financial Institutions: Risk Management in Regional Divergence

Mortgage lenders must carefully calibrate their approach to Scotland's outperforming market. While strong price growth supports loan-to-value ratios and reduces default risk in the short term, rapid appreciation can also signal potential correction risk.

Prudent lending strategies include:

📊 Enhanced valuation scrutiny: Lenders should ensure their valuation panels include surveyors with current, granular knowledge of Scottish micro-markets and should review valuation reports for adequate consideration of market sustainability.

📊 Stress testing: Mortgage affordability assessments should incorporate scenarios where Scottish price growth moderates or reverses, ensuring borrowers can sustain payments through various market conditions.

📊 Portfolio concentration monitoring: Lenders with significant Scottish exposure should monitor geographic concentration risk and consider whether rapid regional appreciation creates portfolio imbalances.

📊 Product innovation: Scotland's strong market may support specialized mortgage products that recognize regional stability while maintaining prudent underwriting standards.

For Investors and Portfolio Managers: Capitalizing on Regional Strength

Property investors viewing Scotland's 2026 performance may see compelling opportunities, but successful investment requires sophisticated analysis that goes beyond headline price growth figures.

Investment considerations include:

💰 Yield analysis: While capital appreciation is strong, investors must also assess rental yields and whether they remain competitive with other investment classes and regions.

💰 Tenant demand fundamentals: Price growth should be supported by underlying rental demand driven by employment, demographics, and housing supply constraints.

💰 Exit strategy planning: Even in strong markets, investors need clear exit strategies and should consider whether future buyers will have access to mortgage finance at sustainable rates.

💰 Professional property management: As rental regulations evolve across the UK, professional management becomes increasingly important to ensure compliance and protect investment returns.

Future Outlook: Sustaining Scotland's 2026 Leadership

Monitoring Indicators for Continued Outperformance

The Valuation Adjustments for Scotland's 2026 House Price Leadership: RICS Strategies Outpacing National Recovery must remain dynamic, adapting as market conditions evolve. Several key indicators will signal whether Scotland's leadership position is sustainable:

Buyer enquiry trends: The +21% January figure represents strong momentum, but sustained outperformance requires this metric to remain positive in coming months[1].

Mortgage approval rates: Scotland's strength depends partly on buyers' ability to secure financing. If UK-wide lending standards tighten or interest rates rise unexpectedly, Scotland's advantage could diminish.

Supply-demand balance: The +27% increase in new instructions is positive if matched by demand, but if supply continues rising while buyer interest plateaus, price growth could moderate[1].

Broader economic indicators: Scottish employment rates, wage growth, and business confidence must continue supporting housing demand. Any deterioration in these fundamentals would challenge the property market's trajectory.

UK-wide policy changes: Government decisions on stamp duty, mortgage regulations, or housing policy could affect Scotland differently than other regions, either enhancing or diminishing its relative advantage.

Long-Term Valuation Strategy Development

Professional surveyors and valuation firms operating in Scotland should develop long-term strategies that position them to serve clients effectively regardless of how market conditions evolve:

🏆 Continuous professional development: Staying current with market trends, valuation methodology innovations, and RICS guidance updates ensures professional competence in dynamic markets.

🏆 Technology integration: Valuation software, market data analytics, and digital reporting tools can enhance accuracy and efficiency while providing clients with more comprehensive insights.

🏆 Client education programs: Helping clients understand valuation processes, market dynamics, and the limitations of property valuations builds trust and manages expectations.

🏆 Market research capabilities: Firms that invest in proprietary market research and maintain comprehensive transaction databases gain competitive advantages in providing accurate, defensible valuations.

🏆 Professional network development: Collaboration with other property professionals—estate agents, mortgage brokers, solicitors—provides valuable market intelligence and referral opportunities.

Conclusion

The Valuation Adjustments for Scotland's 2026 House Price Leadership: RICS Strategies Outpacing National Recovery represent both an opportunity and a challenge for property professionals across the United Kingdom. Scotland's remarkable +42% house price balance, combined with surging buyer enquiries (+21%), rising property listings (+27%), and exceptional forward sales expectations (+46%), has created a regional market dynamic that demands sophisticated, adaptive valuation approaches[1][2].

RICS-qualified surveyors must balance optimism about Scotland's genuine economic strengths with prudent risk assessment that protects clients and maintains professional standards. Traditional valuation methodologies require thoughtful adaptation—incorporating time-adjusted comparables, scenario-based analysis, and enhanced market sustainability assessment—while remaining firmly grounded in Red Book compliance and professional ethics.

For buyers, sellers, lenders, and investors, Scotland's 2026 leadership position offers opportunities but requires careful navigation. Professional guidance from registered RICS valuers becomes invaluable in a market where regional divergence has created complexity that generalized advice cannot adequately address.

Actionable Next Steps

For property professionals:

- Review and update valuation methodologies to ensure they adequately address rapid regional appreciation

- Enhance market research capabilities and comparable sales databases with Scotland-specific data

- Implement peer review processes for high-value or complex valuations

- Communicate clearly with clients about market volatility and valuation uncertainty

For property buyers and sellers:

- Engage qualified RICS surveyors for professional valuations and surveys before making purchase or pricing decisions

- Maintain realistic expectations about market sustainability and avoid decisions driven solely by fear of missing out

- Focus on long-term property suitability rather than short-term market timing

- Ensure financial preparedness and mortgage pre-approval before entering competitive bidding situations

For lenders and investors:

- Conduct thorough due diligence on Scottish market fundamentals and sustainability indicators

- Implement stress testing that accounts for potential market corrections or regional convergence

- Monitor portfolio concentration risk and geographic diversification

- Stay informed about evolving RICS guidance and valuation best practices

Scotland's 2026 house price leadership demonstrates that regional property markets can diverge significantly from national trends, creating both opportunities and risks that demand professional expertise, careful analysis, and adaptive strategies. By implementing the valuation adjustments and strategic approaches outlined in this analysis, property professionals and stakeholders can navigate Scotland's dynamic market environment with confidence and competence. 🏴📈

References

[1] Scottish Housing Market 2026 Rics Survey – https://www.simpsonmarwick.com/journal/scottish-housing-market-2026-rics-survey

[2] Scottish Surveyors Optimistic About 2026 Housing Market – https://projectscot.com/2026/01/scottish-surveyors-optimistic-about-2026-housing-market/

[3] Uk Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[4] House Price Forecast – https://hoa.org.uk/advice/guides-for-homeowners/i-am-buying/house-price-forecast/

[5] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution