The 2026 budget reforms have sent shockwaves through the high-value property market. Properties valued over £2 million now face significant new tax implications that demand precise valuation methodologies and robust expert witness testimony. For property professionals, understanding how to build defensible valuation adjustment cases has never been more critical. Valuation Adjustments for High-Value Property Tax Changes: Building Expert Witness Cases Post-Budget 2026 represents a fundamental shift in how expert witnesses approach property disputes, requiring enhanced documentation strategies and sophisticated analytical frameworks.

Key Takeaways

- 🏛️ New tax thresholds for properties over £2 million require specialized valuation adjustment methodologies to defend against challenges

- 📊 Expert witnesses must document comparable sales adjustments, market conditions, and property-specific factors with unprecedented detail

- ⚖️ Legal defensibility depends on following RICS standards while incorporating 2026 budget-specific considerations

- 📈 Market volatility post-budget demands real-time data analysis and transparent adjustment calculations

- 🔍 Documentation quality directly impacts tribunal outcomes, making systematic evidence gathering essential

Understanding the 2026 Budget Impact on High-Value Properties

The 2026 budget introduced substantial changes affecting properties in the premium market segment. While UK-specific reforms focus on properties exceeding £2 million, parallel developments in international markets provide valuable context for understanding valuation challenges.

Key Legislative Changes

The budget reforms establish new valuation thresholds that trigger enhanced scrutiny from tax authorities. Properties in the high-value bracket now require more sophisticated justification for assessed values, particularly when adjustments reduce tax liability.

International precedents offer instructive examples. In Ohio, House Bill 335 caps property tax growth related to inside millage to inflation rates, with county budget commissions required to adjust tax rates limiting revenue increases to cumulative inflation over three years[2]. This approach demonstrates how jurisdictions balance revenue needs with taxpayer protection.

Similarly, Salt Lake County implemented a property tax increase of approximately 14.65% in 2026, though this affected only the county's portion of total bills[3]. These regional variations highlight the importance of understanding local market dynamics when preparing valuation adjustments.

Valuation Implications for Expert Witnesses

Expert witnesses must now account for:

- Enhanced documentation requirements for properties above threshold values

- Increased scrutiny of adjustment methodologies by tax authorities

- Market volatility stemming from policy uncertainty

- Comparable sales selection in rapidly changing markets

- Adjustment transparency to withstand tribunal examination

Professional valuation services require updated protocols that address these new challenges while maintaining RICS compliance.

Building Robust Valuation Adjustment Frameworks

Creating defensible valuation adjustments for high-value properties demands systematic approaches that withstand rigorous cross-examination. Expert witnesses must establish clear methodologies before engaging with specific cases.

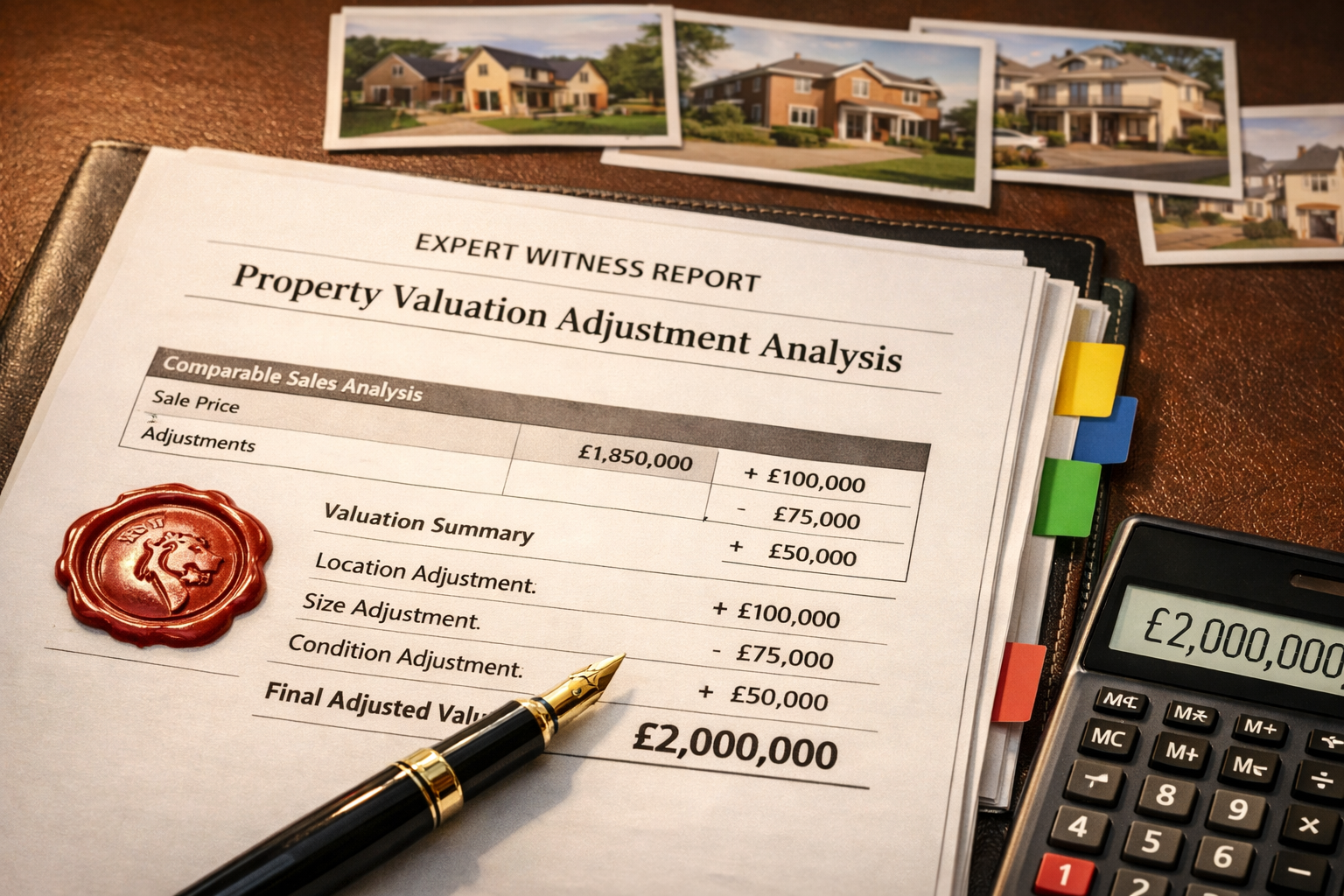

The Comparable Sales Method: Enhanced Standards

The comparable sales approach remains foundational, but 2026 standards require enhanced adjustment documentation:

| Adjustment Category | Documentation Required | Typical Range |

|---|---|---|

| Location Premium | Geographic analysis, amenity mapping | ±5-15% |

| Property Size | Square footage comparison, usable space | ±10-20% |

| Condition Variance | Survey reports, maintenance records | ±5-25% |

| Market Timing | Transaction date analysis, trend data | ±3-10% |

| Unique Features | Specialist assessments, cost analysis | ±5-30% |

Each adjustment must be supported by empirical evidence rather than professional judgment alone. This shift reflects tribunal expectations for quantifiable justification.

Market Conditions Analysis

Understanding broader market dynamics provides essential context for individual property valuations. Expert witnesses should incorporate:

- Transaction volume trends in the relevant market segment

- Days on market statistics for comparable properties

- Price per square foot movements over relevant periods

- Economic indicators affecting high-value property demand

- Regulatory changes impacting market sentiment

The capital gains tax valuation process offers parallel methodologies applicable to tax-related disputes.

Property-Specific Adjustment Factors

Beyond market-wide considerations, individual property characteristics require careful analysis:

Physical Characteristics:

- Architectural significance and design quality

- Construction materials and build quality

- Energy efficiency and sustainability features

- Technology integration and smart home capabilities

- Outdoor space and landscaping quality

Legal and Title Considerations:

- Leasehold vs. freehold status

- Restrictive covenants affecting use

- Rights of way or easements

- Planning permissions and development potential

- Listed building restrictions

For leasehold properties, specialized lease extension valuation expertise becomes crucial in establishing accurate baseline values.

Documentation Strategies for Valuation Adjustments in Expert Witness Cases Post-Budget 2026

The success of any expert witness case hinges on documentation quality. Post-2026 reforms demand systematic evidence gathering that anticipates challenges from opposing counsel and tribunal members.

Creating the Evidence Portfolio

A comprehensive evidence portfolio should include:

Primary Documentation:

- Complete property survey reports

- Title documentation and legal searches

- Historical transaction records

- Planning permission history

- Building control certificates

- Energy performance certificates

Professional building surveys provide foundational documentation that supports valuation conclusions.

Market Evidence:

- Comparable sales database with detailed property cards

- Market analysis reports from recognized sources

- Local authority planning data

- Land Registry price paid data

- Estate agent marketing materials

- Auction results for similar properties

Adjustment Calculations:

- Detailed spreadsheets showing adjustment derivation

- Sensitivity analysis demonstrating adjustment ranges

- Peer review documentation

- Professional standards compliance checklist

The Comparable Sales Database

Expert witnesses must maintain robust comparable sales databases with:

- Minimum 10-15 comparable transactions

- Transaction dates within 12-18 months

- Geographic proximity (preferably within 1-2 miles)

- Similar property characteristics

- Verified sale prices and terms

- Detailed property descriptions

- Photographs and floor plans where available

Each comparable should include adjustment justifications explaining why specific modifications were applied.

Adjustment Transparency Requirements

Post-2026 standards emphasize transparent methodology. Expert witnesses should:

- Document the adjustment rationale for each comparable

- Quantify adjustments using market-derived data where possible

- Provide ranges rather than point estimates for uncertain factors

- Acknowledge limitations in available data

- Cross-reference multiple valuation approaches

This transparency builds credibility and demonstrates professional integrity under cross-examination.

Technology Integration

Modern valuation practices increasingly incorporate technology:

- Geographic Information Systems (GIS) for location analysis

- Automated Valuation Models (AVMs) as supporting evidence

- Digital measurement tools for property dimensions

- Database management systems for comparable tracking

- Visualization software for presenting complex data

While technology enhances efficiency, expert witnesses must understand underlying methodologies and not rely blindly on automated outputs.

Preparing for Tribunal and Court Proceedings

Expert witness testimony represents the culmination of valuation work. Preparation determines whether carefully constructed adjustments withstand scrutiny.

Pre-Hearing Preparation

Effective preparation involves:

Report Refinement:

- Multiple internal reviews for consistency

- Peer review by qualified colleagues

- Compliance check against RICS standards

- Anticipation of likely challenges

- Preparation of supplementary materials

Cross-Examination Readiness:

- Review of opposing expert reports

- Identification of methodology differences

- Preparation of rebuttal evidence

- Mock cross-examination practice

- Clarification of technical terminology

Presenting Adjustment Evidence

Clear presentation enhances credibility:

- Visual aids showing comparable locations and properties

- Tables summarizing adjustment calculations

- Charts illustrating market trends

- Photographs documenting property conditions

- Maps demonstrating geographic relationships

The goal is making complex valuation concepts accessible to non-specialist tribunal members while maintaining technical rigor.

Common Challenges and Responses

Expert witnesses frequently face these challenges:

Challenge: "Your adjustments appear arbitrary."

Response: Reference documented market evidence supporting each adjustment percentage, demonstrating systematic derivation.

Challenge: "Why didn't you use this comparable sale?"

Response: Explain specific disqualifying factors (timing, condition, location) with reference to professional standards.

Challenge: "Isn't this just your opinion?"

Response: Distinguish between professional judgment (applied to ambiguous factors) and empirical evidence (market-derived data).

Challenge: "Your valuation differs significantly from the tax assessment."

Response: Explain methodological differences, data sources, and valuation date considerations.

Maintaining Professional Standards

Throughout proceedings, expert witnesses must:

- Remain impartial regardless of who commissioned the report

- Acknowledge uncertainties rather than overstating confidence

- Admit limitations in available evidence

- Defer to specialists on matters outside expertise

- Update opinions if new evidence emerges

These principles align with RICS professional conduct requirements and enhance tribunal confidence in testimony.

International Perspectives on Property Tax Valuation

While UK reforms drive immediate concerns, international developments provide valuable context for understanding emerging trends.

United States Property Tax Reforms

Several U.S. jurisdictions implemented significant changes affecting 2026 tax years:

Ohio Reforms:

The state enacted comprehensive property tax reform through multiple bills. House Bill 335 specifically caps property tax growth to inflation rates, with county budget commissions required to adjust tax rates limiting revenue increases[2]. Additionally, the Owner-Occupancy Credit expands with scheduled increases: 5.70% (2026), 8.92% (2027), 12.15% (2028), and 15.38% (2029 and beyond)[2].

The Homestead Exemption for Tax Year 2026 provides $28,000 exemption for standard homesteads and $56,000 for enhanced exemptions[2]. These mechanisms demonstrate how jurisdictions balance tax revenue needs with affordability concerns.

Texas Developments:

Austin City Council approved amended budgets affecting property tax rates, while Travis County implemented taxpayer statement requirements enhancing transparency[5][6]. These reforms emphasize communication and justification of tax assessments.

Federal Opportunity Zone Changes:

The One, Big, Beautiful Bill Act (signed July 4, 2025) reduced the substantial improvement threshold from 100% to 50% for rural properties[1]. This change affects valuation methodologies for rural real estate investments, potentially creating new dispute areas.

Lessons for UK Expert Witnesses

International reforms suggest several trends:

- Increased transparency requirements in valuation methodologies

- Inflation-linked mechanisms constraining tax growth

- Enhanced taxpayer protections requiring stronger justification for assessments

- Technology adoption in valuation and assessment processes

UK expert witnesses should monitor these developments as potential indicators of future domestic policy directions.

Specialized Considerations for Different Property Types

High-value properties encompass diverse categories requiring tailored approaches.

Residential Properties

Premium residential properties present unique challenges:

- Subjective value elements (views, prestige, design aesthetics)

- Limited comparable sales in exclusive markets

- Renovation and improvement value quantification

- Historic or architectural significance premiums

Comprehensive RICS building surveys provide essential condition documentation supporting adjustment decisions.

Commercial Properties

Commercial valuations involve additional complexity:

- Income capitalization approaches alongside comparable sales

- Tenant quality and lease terms affecting value

- Market rent analysis and yield considerations

- Specialized use properties with limited comparables

Commercial valuation expertise becomes essential for mixed-use or investment properties.

Rural and Agricultural Properties

Rural high-value properties require specialized knowledge:

- Agricultural land classification and productivity

- Development potential and planning constraints

- Environmental designations affecting use

- Access and infrastructure considerations

- Sporting rights and amenity value

The reduced substantial improvement threshold for rural Qualified Opportunity Zones (50% rather than 100%)[1] demonstrates how policy changes create new valuation considerations.

Heritage and Listed Properties

Protected properties demand particular expertise:

- Conservation requirements affecting alteration costs

- Maintenance obligations impacting value

- Grant availability for restoration work

- Market limitations due to regulatory constraints

- Specialist buyer pool considerations

These factors often justify significant adjustments from standard comparable sales.

Technology and Data Analytics in Modern Valuation Practice

Contemporary expert witness work increasingly incorporates sophisticated analytical tools.

Data Sources and Verification

Reliable data forms the foundation of defensible valuations:

Primary Sources:

- Land Registry official copies and price paid data

- Local authority planning and building control records

- RICS Comparable Evidence Database

- Professional valuation databases (e.g., CoStar, EGi)

- Direct market participant surveys

Verification Protocols:

- Cross-referencing multiple data sources

- Confirming transaction terms (arm's length, special conditions)

- Validating property characteristics through site visits

- Checking data currency and relevance

Analytical Tools

Modern practice employs various analytical approaches:

Statistical Analysis:

- Regression analysis identifying value drivers

- Time series analysis for trend identification

- Spatial analysis for location premium quantification

- Sensitivity analysis testing assumption impacts

Visualization:

- Heat mapping for geographic value patterns

- Scatter plots showing comparable relationships

- Time series charts illustrating market movements

- Adjustment waterfall charts showing cumulative effects

Modeling:

- Hedonic pricing models incorporating multiple variables

- Automated Valuation Models (AVMs) as supporting evidence

- Monte Carlo simulation for uncertainty quantification

- Scenario analysis for alternative assumptions

Technology Limitations

Despite technological advances, expert witnesses must recognize limitations:

- Model accuracy depends on data quality and quantity

- Unique property characteristics may not fit standard models

- Market disruptions can invalidate historical relationships

- Human judgment remains essential for unusual situations

Technology should augment rather than replace professional expertise.

Professional Development and Continuing Education

The evolving landscape demands ongoing professional development.

Essential Knowledge Areas

Expert witnesses should maintain current knowledge in:

- Valuation standards (RICS Red Book, IVS)

- Tax legislation affecting property values

- Case law establishing precedents

- Market trends in relevant property sectors

- Technology applications in valuation practice

Professional Qualifications

Relevant credentials enhance credibility:

- RICS qualification (MRICS or FRICS)

- Expert witness training and accreditation

- Specialist designations for property types

- Continuing Professional Development (CPD) compliance

Peer Review and Quality Control

Maintaining quality standards requires:

- Internal review processes before report finalization

- Peer review by qualified colleagues

- Professional indemnity insurance with adequate coverage

- Complaints procedures and quality monitoring

- Regular methodology audits

Conclusion: Building Defensible Cases in the Post-2026 Landscape

Valuation Adjustments for High-Value Property Tax Changes: Building Expert Witness Cases Post-Budget 2026 demands unprecedented rigor in methodology, documentation, and presentation. The new tax landscape for properties over £2 million has fundamentally altered expectations for expert witness work, requiring enhanced transparency and empirical support for every adjustment.

Key Success Factors

Expert witnesses who excel in this environment will:

✅ Develop systematic documentation protocols capturing all relevant evidence

✅ Maintain comprehensive comparable sales databases with detailed adjustment justifications

✅ Embrace technology while retaining professional judgment

✅ Stay current with legislative changes and market developments

✅ Prioritize transparency in methodology and limitations

✅ Invest in continuing education and professional development

Actionable Next Steps

For property professionals preparing for expert witness roles:

- Review and update valuation methodologies to reflect 2026 standards

- Establish robust data collection systems for comparable evidence

- Invest in technology tools supporting analysis and presentation

- Undertake expert witness training if not already qualified

- Build relationships with legal professionals handling property tax disputes

- Document existing cases to establish track record and refine approaches

- Join professional networks sharing best practices and emerging issues

The complexity of post-2026 property tax valuations creates both challenges and opportunities. Expert witnesses who master the enhanced documentation requirements, embrace transparent methodologies, and maintain unwavering professional standards will find themselves in high demand as property owners navigate the new tax landscape.

Success in this field requires balancing technical expertise with communication skills, analytical rigor with practical judgment, and confidence with humility. By focusing on these fundamentals while adapting to evolving requirements, expert witnesses can build compelling cases that withstand the most rigorous scrutiny and serve the interests of justice in property tax disputes.

References

[1] One Big Beautiful Bill Provisions – https://www.irs.gov/newsroom/one-big-beautiful-bill-provisions

[2] Update On Real Property Tax Reform Recent Legislation And Proposed Ohio Constitutional Amendment – https://www.squirepattonboggs.com/insights/publications/update-on-real-property-tax-reform-recent-legislation-and-proposed-ohio-constitutional-amendment/

[3] 2026 Budget Tax Increase – https://www.saltlakecounty.gov/mayor/2026-budget-tax-increase/

[5] Austin City Council Approves Amended Fiscal Year 2025 2026 Budget – https://www.austintexas.gov/communications/news/austin-city-council-approves-amended-fiscal-year-2025-2026-budget

[6] Tc Taxpayer Statement – https://www.traviscountytx.gov/planning-budget/tc-taxpayer-statement