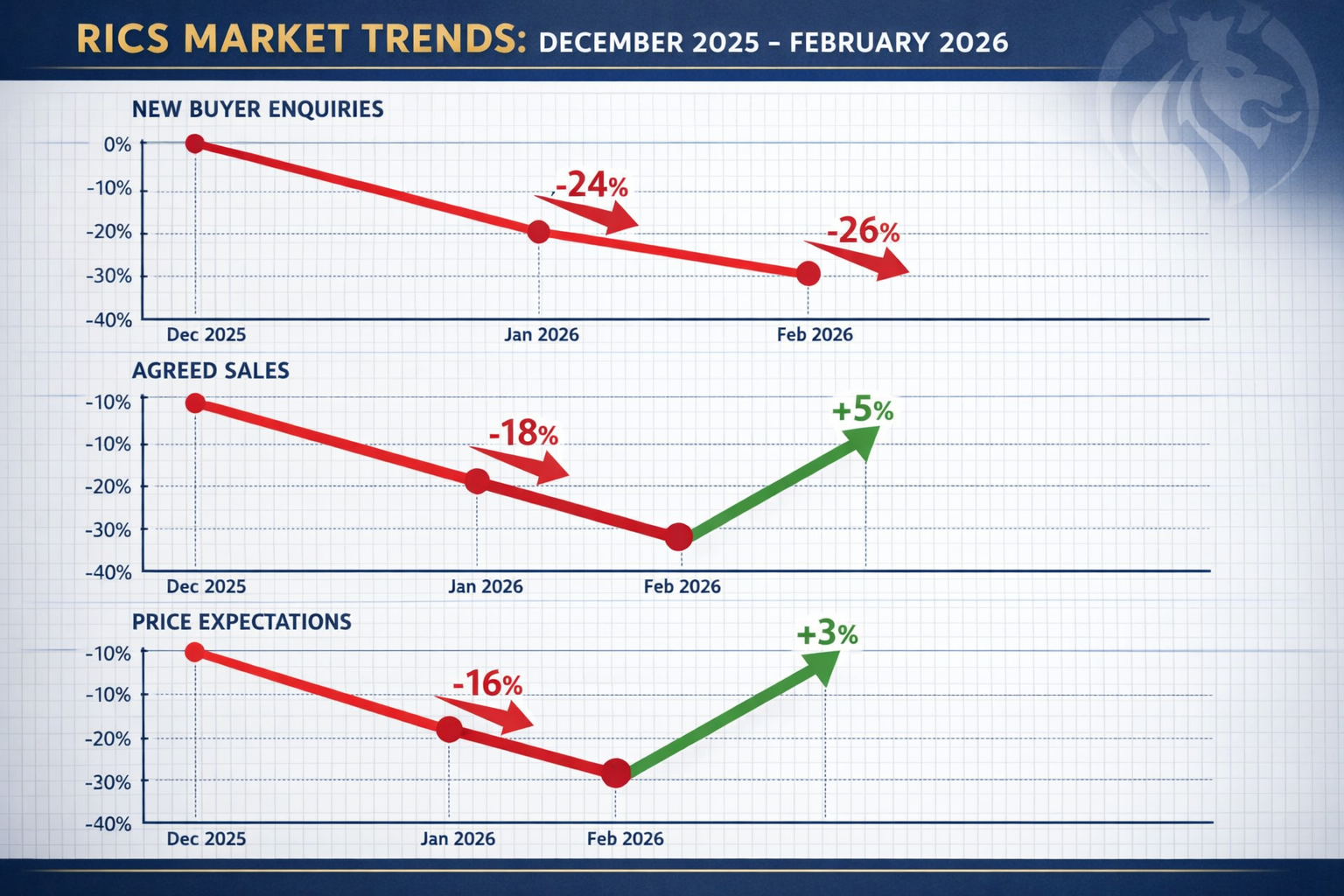

The first quarter of 2026 has delivered a complex narrative for property surveyors across the UK. While January's cautious optimism suggested a recovery in buyer sentiment—with new buyer enquiries improving to -15% from December's -21%—February's sharp reversal to -26% has created both challenges and opportunities for surveying professionals. The Surveyor Demand Surge in Q1 2026: Capitalizing on RICS-Reported New Buyer Enquiry Recovery represents a pivotal moment for firms prepared to adapt their strategies, scale operations efficiently, and position themselves for the longer-term market rebound that RICS data continues to forecast [1][2].

Despite short-term volatility driven by macroeconomic uncertainty, the underlying fundamentals point toward sustained demand for professional surveying services. With 17% of surveyors expecting sales activity to rise over the next 12 months and 33% anticipating price increases over the same period, forward-thinking firms have a narrow window to optimize their operations and capture market share [2].

Key Takeaways

- 📉 New buyer enquiries fell to -26% in February 2026, reversing January's improvement of -15%, driven by renewed macroeconomic and geopolitical uncertainty

- 📊 Long-term outlook remains positive: +17% of surveyors expect sales activity to increase over 12 months, with +33% forecasting price rises

- 🏘️ Regional divergence creates opportunities: Northern England shows strong price growth while London's expectations have cooled dramatically from +56% to +7%

- ⏱️ Operational efficiency is critical: Surveyors must streamline processes and manage survey timelines effectively to meet fluctuating demand

- 🎯 Strategic positioning matters: Firms that invest in capacity, technology, and regional expertise now will capture disproportionate market share during the recovery

Understanding the Q1 2026 Market Dynamics: What the RICS Data Reveals

The January Recovery That Wasn't

January 2026 brought a brief moment of relief to the UK property market. The RICS UK Residential Market Survey recorded a net balance of -15% for new buyer enquiries, representing a meaningful improvement from December 2025's reading of -21% [1]. This six-percentage-point gain sparked cautious optimism among property professionals, with many interpreting the data as evidence that the market had weathered the worst of 2025's challenges.

However, this optimism proved premature. By February, the net balance for new buyer enquiries had plummeted to -26%, an 11-percentage-point deterioration that caught many industry observers off guard [2]. This sharp reversal highlighted the fragility of buyer confidence in early 2026 and underscored the ongoing impact of external economic pressures.

February's Reality Check: Macroeconomic Headwinds Intensify

The February decline wasn't an isolated metric. Multiple indicators pointed to weakening market conditions:

| Metric | January 2026 | February 2026 | Change |

|---|---|---|---|

| New Buyer Enquiries | -15% | -26% | ↓ 11 points |

| Agreed Sales | -10% | -12% | ↓ 2 points |

| Near-Term Price Expectations (3 months) | -6% | -18% | ↓ 12 points |

| Near-Term Sales Expectations (3 months) | +4% | -2% | ↓ 6 points |

The RICS report explicitly attributed the February weakness to "renewed geopolitical and macroeconomic uncertainty" [2]. Concerns over inflation persistence, interest rate trajectories, and global economic instability weighed heavily on buyer sentiment, causing many prospective purchasers to pause their property searches.

The Silver Lining: Long-Term Expectations Remain Resilient

Despite the near-term turbulence, the Surveyor Demand Surge in Q1 2026: Capitalizing on RICS-Reported New Buyer Enquiry Recovery narrative remains valid when examining longer-term forecasts. RICS members maintain a notably more optimistic 12-month outlook:

- ✅ +17% net balance expect sales activity to rise over the next 12 months

- ✅ +33% net balance anticipate prices to edge higher over the same period [2]

This divergence between short-term caution and long-term confidence creates a strategic opportunity for surveyors. Firms that can navigate the Q1 volatility while building capacity for the anticipated recovery will be positioned to capture significant market share as conditions improve.

Surveyor Demand Surge in Q1 2026: Operational Strategies for Market Volatility

Scaling Operations to Meet Fluctuating Demand

The volatile Q1 2026 market conditions demand operational flexibility. Surveying firms must balance the need to maintain service quality with the reality of unpredictable enquiry volumes. Several strategies have proven effective:

1. Flexible Staffing Models 🔄

Rather than committing to permanent headcount increases, leading firms are adopting hybrid staffing approaches:

- Associate surveyor networks: Building relationships with qualified RICS-accredited professionals who can take on assignments during demand spikes

- Regional partnerships: Collaborating with local chartered surveyors in high-demand areas to share workload

- Cross-training initiatives: Ensuring team members can handle multiple survey types, from Level 2 Homebuyer surveys to specialist defect surveys

2. Technology Investment for Efficiency 💻

Digital transformation is no longer optional for competitive surveying practices:

- Automated scheduling systems that optimize surveyor routes and minimize travel time

- Digital reporting platforms that reduce report turnaround times by 30-40%

- Client communication portals that provide real-time updates on survey progress

- Drone survey capabilities for large or complex properties, reducing on-site time requirements

3. Timeline Management and Client Expectations ⏰

Understanding how long a homebuyer's survey takes is crucial for managing client expectations during volatile periods. Best practices include:

- Transparent communication: Providing realistic timelines at the point of booking

- Priority service options: Offering expedited surveys for time-sensitive transactions

- Proactive updates: Contacting clients before they need to chase for information

- Capacity planning: Maintaining 15-20% buffer capacity to accommodate urgent requests

Regional Positioning: Where to Focus Resources in 2026

The Surveyor Demand Surge in Q1 2026: Capitalizing on RICS-Reported New Buyer Enquiry Recovery is not geographically uniform. RICS data reveals pronounced regional divergence that smart firms are exploiting:

Northern England: The Standout Performer 🌟

Northern regions emerged as the clear winner in Q1 2026, with prices moving higher while other areas stagnated or declined [4]. Surveying firms should consider:

- Expanding capacity in key Northern markets

- Developing expertise in regional property types and construction methods

- Building relationships with Northern estate agents and mortgage brokers

- Marketing services that highlight local market knowledge

London: Cooling Expectations Require Recalibration 🏙️

London's 12-month price expectations collapsed from +56% to just +7% between measurement periods [4][5]. This dramatic shift suggests:

- Increased price sensitivity among London buyers

- Greater demand for detailed building surveys to justify valuations

- Opportunities in specialist services like commercial property surveys as investors seek value

- Need for registered RICS valuers who can provide defensible valuations in uncertain markets

Southeast and Home Counties: Steady Demand 🏡

Areas like Guildford, Berkshire, and Hampshire continue to show relatively stable demand patterns, making them reliable revenue sources during volatile periods.

Surveyor Demand Surge in Q1 2026: Service Mix Optimization and Revenue Diversification

Adapting Survey Offerings to Market Conditions

The Q1 2026 market volatility has created distinct demand patterns across different survey types. Successful firms are adjusting their service mix accordingly:

High-Demand Services in Q1 2026 📈

- Detailed Building Surveys: With price uncertainty, buyers increasingly opt for comprehensive building surveys rather than basic valuations

- Specific Defect Reports: Targeted specific defect reports allow buyers to investigate concerns without commissioning full surveys

- Pre-Purchase Valuations: Buyers want independent confirmation that asking prices align with market realities

- Commercial Surveys: Business property transactions continue despite residential market weakness, creating opportunities for commercial property surveyors

Emerging Opportunities 🌱

- Rental Property Surveys: With tenant demand at +2% in February and landlord instructions severely depressed at -27%, rental investors need professional guidance [2]

- Dilapidations Work: Commercial schedule of dilapidations services remain steady regardless of residential market conditions

- Specialist Services: Damp surveys, boundary surveys, and monitoring surveys provide counter-cyclical revenue streams

Pricing Strategy in Uncertain Markets

Understanding surveyor pricing and structural survey costs is essential for competitive positioning in Q1 2026. Strategic considerations include:

Value-Based Pricing 💰

Rather than competing solely on price, leading firms emphasize:

- Expertise and qualifications: RICS accreditation, specialist certifications, years of experience

- Turnaround time: Faster service justifies premium pricing

- Report quality: Comprehensive, clearly written reports with photographic evidence

- Post-survey support: Availability to answer questions and attend negotiations

Tiered Service Offerings 📊

Creating clear service tiers helps clients self-select based on their needs and budgets:

- Essential: Basic compliance with RICS standards at competitive pricing

- Comprehensive: Enhanced reporting, additional photography, thermal imaging

- Premium: Same-day or next-day service, dedicated surveyor contact, unlimited follow-up consultations

Package Deals 🎁

Bundling services creates value while increasing average transaction value:

- Survey + valuation combinations

- Multi-property discounts for portfolio investors

- Survey + party wall assessment packages for renovation projects

Marketing and Client Acquisition During the Recovery

The Surveyor Demand Surge in Q1 2026: Capitalizing on RICS-Reported New Buyer Enquiry Recovery requires proactive marketing to capture market share:

Digital Presence Optimization 🌐

- SEO-focused content: Educational articles addressing common buyer concerns in 2026

- Local landing pages: Dedicated pages for high-demand areas like North London, Central London, and emerging markets

- Video content: Virtual office tours, surveyor introductions, sample survey walkthroughs

- Client testimonials: Social proof from recent transactions builds trust

Strategic Partnerships 🤝

- Estate agent relationships: Regular communication and co-marketing initiatives

- Mortgage broker networks: Preferred surveyor arrangements and referral agreements

- Solicitor connections: Professional referrals from conveyancing practices

- Property investment groups: Becoming the go-to surveyor for local investor networks

Thought Leadership 📚

- RICS data interpretation: Publishing analysis of monthly survey results

- Market commentary: Regular updates on regional trends and outlook

- Educational webinars: Free sessions on survey types, property issues, and market conditions

- Professional networking: Active participation in industry events and associations

Future-Proofing Your Surveying Practice: Preparing for the 12-Month Recovery

Building Capacity for the Anticipated Upturn

With +17% of surveyors expecting sales activity to rise over the next 12 months [2], firms must prepare for increased demand without overcommitting resources during the uncertain Q1 and Q2 2026 period.

Phased Capacity Building 📅

Smart firms are adopting a staged approach:

- Q1-Q2 2026: Focus on efficiency improvements and flexible staffing

- Q3 2026: Begin selective hiring based on sustained demand signals

- Q4 2026: Full capacity expansion if recovery materializes as forecast

Training and Development 🎓

Investing in team capabilities now pays dividends when demand surges:

- RICS qualification support: Helping AssocRICS members achieve full MRICS status

- Specialist certifications: Thermal imaging, drone operation, heritage property expertise

- Technology training: Ensuring all team members can leverage digital tools effectively

- Customer service excellence: Differentiating through superior client experience

Monitoring Market Indicators for Strategic Decisions

Successful navigation of the Surveyor Demand Surge in Q1 2026: Capitalizing on RICS-Reported New Buyer Enquiry Recovery requires continuous market monitoring:

Key Metrics to Track Monthly 📊

- RICS new buyer enquiry balance: Leading indicator of future survey demand

- Agreed sales balance: Confirms conversion of enquiries to transactions

- Regional price expectations: Identifies geographic opportunities

- New instructions balance: Supply-side indicator affecting market dynamics

- Near-term vs. long-term expectations: Gauges timing of recovery

Internal Performance Metrics 📈

- Enquiry-to-booking conversion rate: Measures sales effectiveness

- Average turnaround time: Operational efficiency indicator

- Client satisfaction scores: Quality and service level tracking

- Revenue per surveyor: Productivity and pricing effectiveness

- Repeat and referral business percentage: Long-term relationship building success

Risk Management in Volatile Markets

The February 2026 reversal demonstrates that market conditions can deteriorate rapidly. Prudent firms are implementing risk mitigation strategies:

Financial Resilience 💪

- Cash reserve maintenance: 3-6 months of operating expenses

- Variable cost structure: Minimizing fixed commitments where possible

- Diversified revenue streams: Reducing dependence on any single service or region

- Flexible lease arrangements: Avoiding long-term property commitments

Professional Liability Considerations ⚖️

Volatile markets increase valuation disputes and professional liability claims:

- Enhanced professional indemnity insurance: Ensuring adequate coverage

- Rigorous quality control: Multiple review stages for all reports

- Clear limitation of liability: Transparent terms of engagement

- Comprehensive documentation: Detailed notes and photographic evidence

Client Credit Risk 💳

Economic uncertainty increases payment default risk:

- Payment terms: Requiring deposits or full payment before report release

- Credit checks: For commercial clients and high-value surveys

- Clear cancellation policies: Protecting revenue from last-minute cancellations

Conclusion: Seizing the Q1 2026 Opportunity

The Surveyor Demand Surge in Q1 2026: Capitalizing on RICS-Reported New Buyer Enquiry Recovery presents a nuanced opportunity for property surveying professionals. While February's sharp decline in new buyer enquiries to -26% has created near-term headwinds, the underlying fundamentals remain supportive of a sustained recovery throughout 2026 and beyond.

The key to success lies in strategic positioning rather than reactive scrambling. Firms that invest now in operational efficiency, regional expertise, service diversification, and technology capabilities will capture disproportionate market share when the anticipated 12-month recovery materializes. With +33% of surveyors expecting price increases and +17% forecasting higher sales activity over the coming year, the medium-term outlook justifies confidence and measured investment.

Actionable Next Steps for Surveying Professionals

✅ Immediate Actions (Next 30 Days)

- Review current capacity and identify operational bottlenecks

- Analyze regional performance and consider resource reallocation toward Northern markets

- Implement or upgrade digital scheduling and reporting systems

- Strengthen relationships with estate agents and mortgage brokers in target markets

✅ Short-Term Priorities (Q2 2026)

- Develop flexible staffing arrangements with associate surveyors

- Create tiered service offerings with clear value differentiation

- Launch targeted marketing campaigns in high-opportunity regions

- Establish monthly RICS data review process for strategic decision-making

✅ Medium-Term Investments (Q3-Q4 2026)

- Build capacity through selective hiring based on sustained demand signals

- Invest in team training and specialist certifications

- Expand service offerings into counter-cyclical areas like commercial and rental property surveys

- Strengthen financial resilience through cash reserves and diversified revenue streams

The surveying professionals who thrive in 2026 will be those who recognize that market volatility creates opportunity for the prepared. By combining operational excellence, strategic positioning, and measured capacity building, forward-thinking firms can transform the Q1 2026 market dynamics into a platform for sustained growth and market leadership.

Understanding different types of surveys and choosing the right property survey for each client's circumstances will remain fundamental to delivering value in this evolving market. The firms that master this balance while maintaining the highest professional standards will emerge as the clear winners from the 2026 market cycle.

References

[1] UK Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[2] UK Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[3] UK Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[4] RICS Residential Market Survey Q1 2026 Building Survey Implications For Northern England Price Surges – https://nottinghillsurveyors.com/blog/rics-residential-market-survey-q1-2026-building-survey-implications-for-northern-england-price-surges-2

[5] Valuation Adjustments For Widening Regional Disparities RICS January 2026 Survey Insights For Surveyors – https://nottinghillsurveyors.com/blog/valuation-adjustments-for-widening-regional-disparities-rics-january-2026-survey-insights-for-surveyors