When house prices hit their lowest point in October 2025, few anticipated the wave of disputes that would follow. Now, in 2026, as the property market shows tentative signs of stabilization, mortgage valuation disputes have surged dramatically. Lenders and borrowers find themselves locked in disagreements over property values, with neither party certain whether current prices represent genuine recovery or merely a temporary plateau. This uncertainty has thrust expert witnesses into the spotlight, where their testimony can determine whether a mortgage proceeds, a refinancing succeeds, or a legal dispute concludes favorably. Understanding Mortgage Valuation Disputes in Early Recovery: Expert Witness Evidence Standards Amid Stabilizing House Prices has become essential for anyone navigating today's complex property landscape.

Key Takeaways

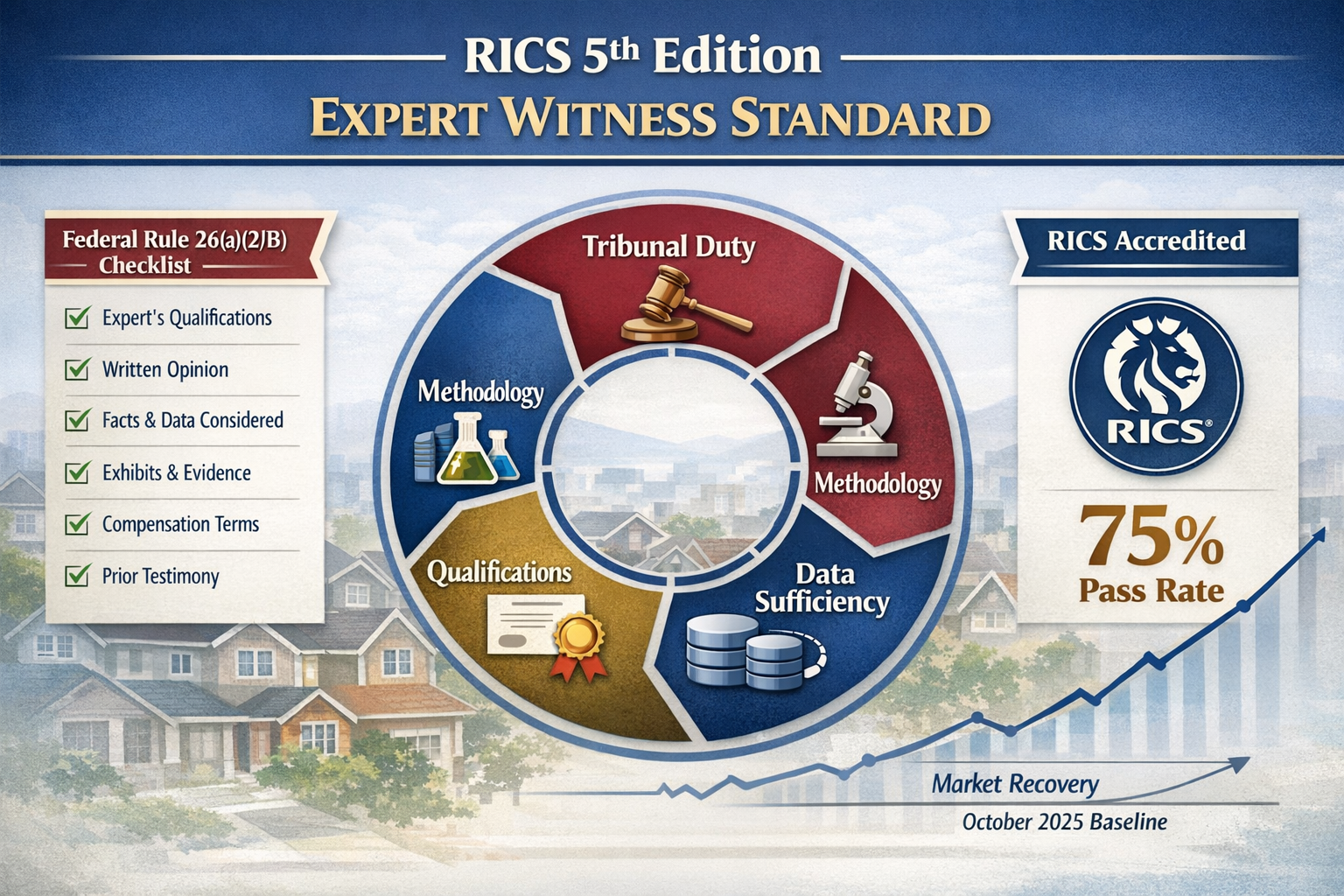

- Expert witness testimony in mortgage valuation disputes must meet strict federal standards under Rule 702, requiring sufficient data, reliable methodology, and proper application to case facts

- The RICS 5th Edition Expert Witness Standard launched in 2026 reinforces that expert witnesses owe their primary duty to the tribunal, not the instructing party

- Federal Rule 26(a)(2)(B) mandates comprehensive expert report disclosures including complete opinion statements, data sources, qualifications, and compensation details

- Market ambiguity following October 2025 price lows creates heightened scrutiny of comparable sales data and valuation methodologies

- Rigorous RICS accreditation maintains approximately 75% pass rates, ensuring only qualified professionals provide expert testimony in property disputes

Understanding the Current Market Context for Valuation Disputes

The property market's trajectory since late 2025 has created unprecedented challenges for valuers and mortgage professionals. After reaching their nadir in October 2025, house prices have exhibited what economists describe as "stabilization with uncertainty"—neither falling dramatically nor rising with confidence. This ambiguous momentum has become fertile ground for disputes between mortgage lenders seeking conservative valuations and borrowers hoping for higher assessments that support their financing needs.

Why Stabilizing Markets Generate More Disputes

When markets trend clearly upward or downward, valuations tend to align more consistently. However, during periods of stabilization, several factors contribute to increased disputes:

- 📊 Comparable sales data becomes less reliable when recent transactions occurred during different market phases

- 🏠 Property-specific features gain disproportionate weight when broader market trends offer little guidance

- 💷 Lender risk appetite varies significantly, leading to different valuation approaches across institutions

- ⚖️ Buyer expectations formed during previous market conditions clash with current realities

These factors have made expert witness testimony increasingly critical in resolving mortgage valuation disputes. Registered RICS valuers find themselves called upon not just to provide valuations, but to defend their methodologies in formal dispute resolution proceedings.

Expert Witness Evidence Standards: The Legal Framework

Federal Rule 702: The Admissibility Threshold

In federal court proceedings involving mortgage valuation disputes, expert testimony must satisfy four distinct criteria established under Rule 702. These requirements ensure that only qualified, reliable evidence reaches the tribunal:

- Helpfulness Standard: The expert's specialized knowledge must genuinely assist the court in understanding evidence or determining facts

- Sufficient Factual Basis: Testimony must rest on adequate facts or data relevant to the case

- Reliable Principles and Methods: The expert must employ principles and methods that meet professional standards of reliability

- Proper Application: The expert must have reliably applied these principles and methods to the specific case facts[1]

The burden of proof operates under a "preponderance of the evidence" standard, meaning the expert's conclusions need only be "more likely than not" to be accurate—a threshold that becomes particularly significant when market conditions remain ambiguous[1].

Federal Rule 26(a)(2)(B): Comprehensive Disclosure Requirements

Before expert witnesses can testify in mortgage valuation disputes, they must satisfy extensive disclosure requirements under Federal Rule 26(a)(2)(B). These mandates ensure transparency and allow opposing parties to properly evaluate expert credentials and methodologies:

| Disclosure Requirement | Purpose | Relevance to Valuation Disputes |

|---|---|---|

| Complete opinion statements | Transparency of conclusions | Reveals valuation figures and reasoning |

| Basis for each opinion | Methodological clarity | Exposes comparable selection criteria |

| Facts and data considered | Evidence foundation | Shows market data sources used |

| Relevant exhibits | Supporting documentation | Includes comparable sales evidence |

| Witness qualifications | Credibility assessment | Demonstrates valuation expertise |

| Publications (10 years) | Professional standing | Establishes thought leadership |

| Prior testimony (4 years) | Track record | Reveals consistency and experience |

| Compensation details | Bias evaluation | Addresses potential conflicts of interest |

These requirements create a comprehensive record that courts can evaluate when determining whether to admit expert testimony in mortgage valuation disputes during early recovery[1]. For property professionals seeking to understand how these standards apply to different property types, commercial valuation processes offer instructive parallels.

RICS 5th Edition Expert Witness Standard: Global Best Practices

The Royal Institution of Chartered Surveyors launched a global consultation on its updated expert witness standard in 2026, marking the first major revision since 2014. This RICS 5th Edition reinforces fundamental principles that govern expert witness conduct in property disputes[2].

Primary Duty to the Tribunal

The cornerstone principle of the updated standard emphasizes that expert witnesses owe their primary duty to the tribunal, not to the client who instructs them. This principle becomes particularly challenging in mortgage valuation disputes where:

- Lenders instruct valuers expecting conservative assessments

- Borrowers seek experts who will support higher valuations

- Commercial pressures may conflict with professional obligations

- Market ambiguity creates room for legitimate differences in opinion

The RICS standard explicitly addresses these tensions, requiring experts to maintain independence regardless of who pays their fees[2]. This duty extends beyond courtroom testimony to include all written reports and preliminary opinions provided during dispute resolution.

Rigorous Accreditation Standards

The RICS Expert Witness Accreditation Service maintains exceptionally high standards, with pass rates hovering around 75% in 2026[3]. This selectivity ensures that only properly qualified professionals provide expert testimony in property disputes. The accreditation process evaluates:

- ✅ Technical valuation competence

- ✅ Understanding of legal procedures and evidence rules

- ✅ Ability to communicate complex concepts clearly

- ✅ Commitment to independence and objectivity

- ✅ Knowledge of current market conditions and data sources

For those involved in disputes requiring expert input, working with properly accredited professionals becomes essential. Choosing the right property survey professional with appropriate credentials can prevent disputes from escalating unnecessarily.

Challenges in Presenting Valuation Evidence During Market Stabilization

The Comparable Sales Conundrum

During periods of clear market trends, selecting appropriate comparable sales follows relatively straightforward principles. However, the current stabilization phase creates significant methodological challenges:

Time-Based Adjustments: When did the comparable transaction occur relative to the October 2025 market low? Sales from different phases of recovery may require substantial adjustments, but determining the appropriate adjustment percentage becomes highly subjective when overall market direction remains uncertain.

Geographic Variations: Different neighborhoods and property types have recovered at varying rates. An expert witness must justify why particular comparables from specific locations provide reliable guidance for the subject property.

Transaction Circumstances: Forced sales, family transactions, and other non-arm's-length deals always require careful evaluation, but during uncertain markets, distinguishing distressed sales from genuine market indicators becomes more complex.

Data Sufficiency in Ambiguous Markets

The Rule 702 requirement for "sufficient facts or data" takes on heightened importance when market conditions remain unclear. Expert witnesses in mortgage valuation disputes must demonstrate that their conclusions rest on adequate evidence despite market ambiguity. This often requires:

- 📈 Multiple valuation approaches: Comparing income, cost, and sales comparison methods to triangulate value

- 🔍 Extended comparable search periods: Casting a wider net to capture sufficient transaction data

- 📊 Statistical analysis: Employing regression analysis or other quantitative methods to identify genuine trends

- 🏘️ Micro-market segmentation: Analyzing specific property types and locations rather than relying on broad market indices

Experts who fail to demonstrate data sufficiency risk having their testimony excluded entirely, regardless of their qualifications or experience. For complex properties requiring specialized analysis, structural surveys may provide additional data points that strengthen valuation conclusions.

Methodology Transparency and Reliability

The requirement for "reliable principles and methods" demands that expert witnesses clearly articulate their valuation approach and justify why it suits the current market conditions. In 2026's stabilizing market, several methodological considerations have gained prominence:

Adjustment Methodology: How does the expert adjust comparable sales for differences in property characteristics, location, and timing? The mathematical formulas and professional judgment underlying these adjustments must withstand scrutiny.

Market Trend Analysis: What evidence supports the expert's conclusions about whether prices are rising, falling, or genuinely stable? Reliance on outdated market reports or insufficient transaction data may undermine credibility.

Risk Assessment: How does the valuation account for continued market uncertainty? Conservative approaches may favor lenders, while optimistic projections may support borrowers, but both must rest on defensible reasoning.

Addressing Bias and Independence

Perhaps no challenge looms larger in mortgage valuation disputes during early recovery than demonstrating genuine independence. The Federal Rule 26(a)(2)(B) compensation disclosure requirement exists precisely because financial incentives can influence expert opinions, consciously or unconsciously.

Expert witnesses must navigate several potential bias concerns:

- 💰 Fee structures that create incentives to favor the instructing party

- 🔄 Repeat business relationships that may influence opinions

- 📝 Advocacy pressure from legal teams seeking favorable testimony

- 🎯 Confirmation bias when experts selectively emphasize data supporting predetermined conclusions

The RICS standard's emphasis on primary duty to the tribunal directly addresses these concerns, but experts must actively demonstrate their independence through balanced analysis and transparent methodology[2]. Those seeking expert assistance should prioritize professionals who maintain clear boundaries between advocacy and objective analysis, similar to the independence required in party wall disputes.

Practical Implications for Lenders, Borrowers, and Property Professionals

For Mortgage Lenders

Lenders navigating mortgage valuation disputes in early recovery should implement several protective measures:

Early Expert Engagement: Involve qualified expert witnesses early in the valuation process, particularly for properties where disputes seem likely. This proactive approach allows experts to gather comprehensive data before positions harden.

Documentation Standards: Maintain detailed records of valuation instructions, data sources, and methodological decisions. These records become crucial if disputes escalate to formal proceedings requiring expert testimony.

Credential Verification: Ensure that valuers possess appropriate RICS accreditation and expert witness credentials. The 75% pass rate for RICS accreditation demonstrates that not all competent valuers qualify as expert witnesses[3].

For Borrowers and Property Buyers

Borrowers facing unfavorable valuations should understand their options and the evidentiary standards that govern disputes:

Independent Valuation: Commissioning an independent desktop house valuation or full survey from a different RICS-accredited professional can provide a second opinion and identify potential grounds for challenging the lender's assessment.

Evidence Gathering: Collect your own comparable sales data, recent listings, and market reports. While this evidence won't carry the same weight as expert testimony, it can support your position and help your expert witness build a stronger case.

Understanding Limitations: Recognize that expert witnesses owe their primary duty to the tribunal, not to you. Even an expert you instruct may reach conclusions that don't fully support your desired outcome if the evidence doesn't justify it[2].

For Property Professionals and Surveyors

Surveyors and valuers who may serve as expert witnesses should prepare themselves for the heightened scrutiny that accompanies mortgage valuation disputes amid stabilizing house prices:

Continuous Professional Development: Stay current with market conditions, valuation methodologies, and legal standards. The 2026 update to RICS expert witness standards reflects evolving best practices that all professionals should understand[2].

Methodological Rigor: Document your valuation approach thoroughly, maintain comprehensive files of comparable sales and market data, and be prepared to justify every adjustment and assumption.

Independence Protocols: Establish clear policies that protect your independence, including transparent fee structures, written engagement terms that specify your duty to the tribunal, and procedures for managing conflicts of interest.

Common Pitfalls in Expert Witness Testimony

Even experienced professionals can stumble when providing expert witness testimony in mortgage valuation disputes. Understanding common pitfalls helps avoid them:

Over-Reliance on Automated Valuation Models

While technology plays an increasing role in property valuation, expert witnesses who rely too heavily on automated valuation models (AVMs) without sufficient manual verification risk having their testimony challenged. AVMs often struggle during market transitions, and courts expect experts to exercise independent professional judgment rather than simply endorsing computer-generated figures.

Insufficient Geographic Knowledge

Expert witnesses must demonstrate genuine familiarity with the specific local market where the subject property sits. An expert with impressive credentials but limited knowledge of local conditions may find their testimony less persuasive than a less-credentialed professional with deep local expertise.

Advocacy Creep

The line between expert witness and advocate can blur, particularly when legal teams pressure experts to strengthen their conclusions. Maintaining objectivity requires constant vigilance and willingness to acknowledge limitations in the available evidence.

Inadequate Disclosure

Failing to fully comply with Federal Rule 26(a)(2)(B) disclosure requirements can result in testimony being excluded entirely. Complete, transparent disclosure protects both the expert's credibility and the admissibility of their evidence[1].

Future Trends in Mortgage Valuation Dispute Resolution

As the property market continues its uncertain recovery through 2026 and beyond, several trends are likely to shape how mortgage valuation disputes are resolved:

Enhanced Data Analytics

Expect increased use of sophisticated statistical methods, machine learning algorithms, and big data analysis in expert witness testimony. These tools can help identify genuine market trends amid noisy data, but experts must be able to explain their methodologies in accessible terms.

Standardized Adjustment Protocols

Industry bodies may develop more standardized approaches to adjusting comparable sales during transitional market periods. While professional judgment will always play a role, greater standardization could reduce the scope for legitimate disagreement.

Alternative Dispute Resolution

The cost and complexity of formal litigation may drive more parties toward mediation and arbitration. These alternative forums often allow more flexible approaches to expert evidence while maintaining rigorous standards for reliability and independence.

Regulatory Evolution

The 2026 update to RICS expert witness standards likely represents just one step in an ongoing evolution of professional requirements. Expect continued refinement of standards governing expert witness conduct, disclosure, and methodology[2].

Conclusion

Mortgage Valuation Disputes in Early Recovery: Expert Witness Evidence Standards Amid Stabilizing House Prices represents one of the most challenging areas of property practice in 2026. The confluence of ambiguous market conditions, rigorous legal standards, and heightened stakes for all parties creates an environment where expert witness testimony has never been more critical—or more scrutinized.

The legal framework governing expert evidence—from Federal Rule 702's admissibility requirements to Federal Rule 26(a)(2)(B)'s comprehensive disclosure mandates—ensures that only qualified, independent professionals providing reliable testimony can influence dispute outcomes[1]. The RICS 5th Edition Expert Witness Standard reinforces these principles while emphasizing the expert's primary duty to the tribunal rather than the instructing party[2].

For lenders, borrowers, and property professionals navigating this complex landscape, several action steps can improve outcomes:

Actionable Next Steps

- Verify Credentials: Ensure any expert witness possesses current RICS accreditation and demonstrated expertise in the relevant property type and market

- Document Thoroughly: Maintain comprehensive records of valuation data, methodologies, and decisions from the outset

- Engage Early: Involve expert witnesses before positions harden, allowing them to gather evidence and provide objective guidance

- Prioritize Independence: Select experts based on their professional reputation and commitment to objectivity, not their likelihood of supporting your preferred outcome

- Understand Standards: Familiarize yourself with the legal and professional standards governing expert evidence in your jurisdiction

- Consider Alternatives: Explore mediation or arbitration as potentially more efficient forums for resolving valuation disputes

The stabilizing property market of 2026 may eventually give way to clearer trends, but until then, the quality of expert witness evidence will continue to determine outcomes in mortgage valuation disputes. By understanding the rigorous standards that govern this evidence and selecting truly qualified professionals to provide it, parties can navigate these disputes more effectively and reach resolutions that reflect genuine property values rather than advocacy positions.

Whether you're a lender protecting your security, a borrower seeking fair treatment, or a property professional providing expert services, mastering the principles outlined in this article will prove essential in the months and years ahead. The market may be uncertain, but the standards for expert evidence remain clear—and those who meet them will find themselves well-positioned to resolve even the most complex valuation disputes.

References

[1] Litigation Leu Wilson Smith Dont Get Struck Financial Expert – https://quickreadbuzz.com/2026/02/04/litigation-leu-wilson-smith-dont-get-struck-financial-expert/

[2] Rics Launches Global Consultation On Updated Expert Witness Standard – https://www.rics.org/news-insights/rics-launches-global-consultation-on-updated-expert-witness-standard

[3] Expert Witness Challenges In 2026 Interest Rate Volatility Disputes Rics Data Driven Preparation – https://nottinghillsurveyors.com/blog/expert-witness-challenges-in-2026-interest-rate-volatility-disputes-rics-data-driven-preparation