The London property market experienced its most dramatic confidence shift in recent memory during February 2026, as chartered surveyors recorded a staggering 49 percentage point collapse in 12-month price expectations—plummeting from +56% optimism in January to a mere +7% the following month. This London Price Sentiment Collapse: Chartered Surveyor Valuation Adjustments as 12-Month Expectations Drop from +56% to +7% represents not just a statistical anomaly, but a fundamental recalibration of professional property assessment methodologies across the capital. With London posting a net balance of -40% for current house price sentiment—the steepest regional decline in the UK—chartered surveyors are now implementing sophisticated valuation adjustments to navigate unprecedented market volatility [1].

Key Takeaways

- 📉 Dramatic confidence collapse: London's 12-month price expectations dropped 49 percentage points from +56% to +7% between January and February 2026, the sharpest single-month decline recorded

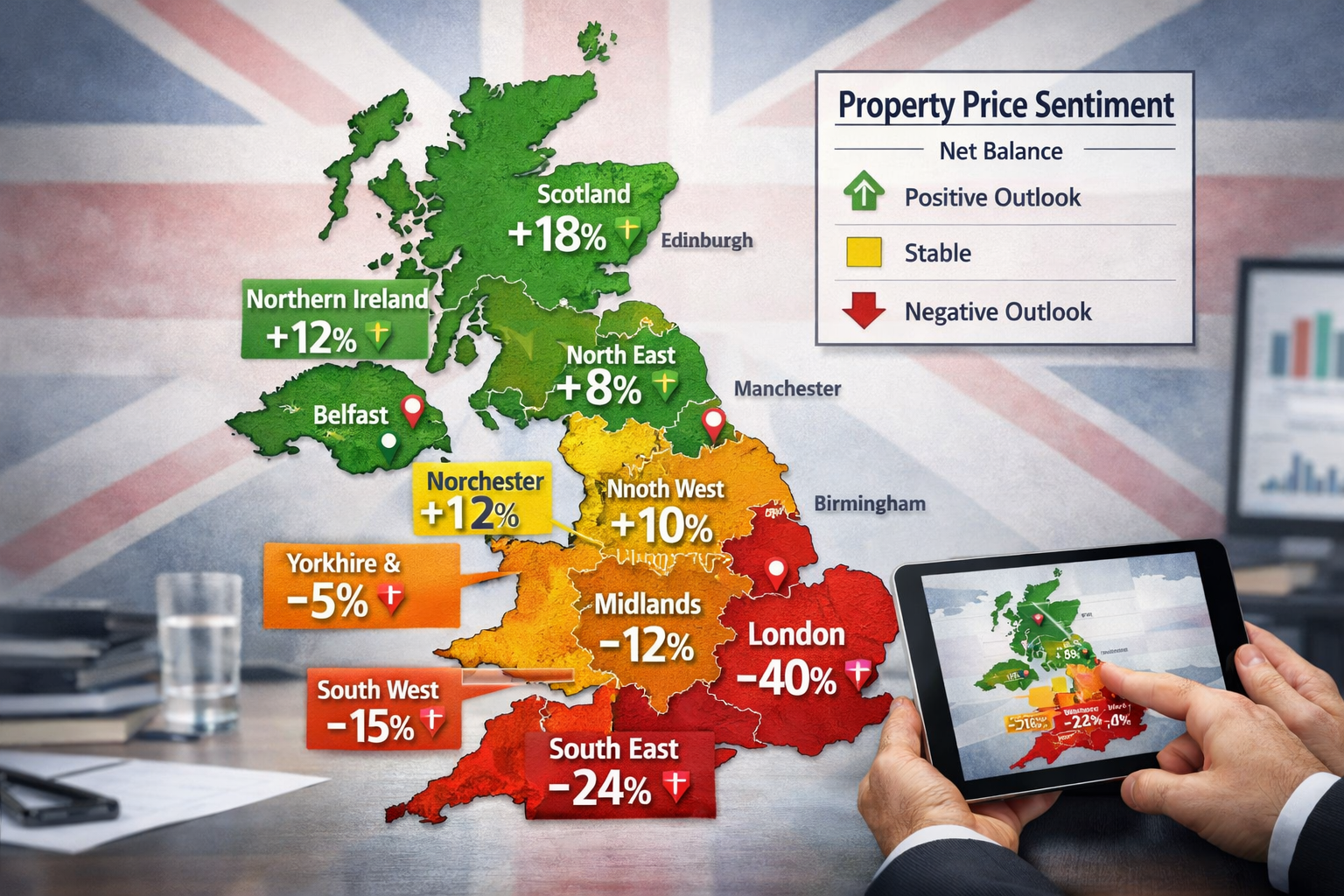

- 🏘️ Regional divergence intensifies: While London recorded -40% net price sentiment, Northern Ireland, Scotland, and North West England continued experiencing price gains

- 📊 Valuation methodology shifts: Chartered surveyors are implementing enhanced comparable analysis, risk-adjusted discount rates, and market condition overlays for London properties

- 💼 Buyer demand weakened significantly: New buyer enquiries fell to -26% net balance in February from -15% in January, reflecting deteriorating market activity

- 🔮 Macroeconomic headwinds persist: Geopolitical uncertainty and renewed inflationary pressures affecting mortgage rates have fundamentally altered market confidence

Understanding the London Price Sentiment Collapse: Chartered Surveyor Valuation Adjustments as 12-Month Expectations Drop from +56% to +7%

The February 2026 RICS UK Residential Market Survey revealed a seismic shift in professional sentiment that caught many market observers off guard. The London Price Sentiment Collapse: Chartered Surveyor Valuation Adjustments as 12-Month Expectations Drop from +56% to +7% wasn't merely a statistical correction—it represented a fundamental reassessment of capital appreciation prospects by the very professionals responsible for determining property values [1].

What Net Balance Figures Actually Mean

Understanding net balance metrics is crucial for interpreting surveyor sentiment. A net balance represents the difference between the percentage of respondents reporting increases versus decreases. When chartered surveyors in Central London report a -40% net balance for house prices, it means 40% more surveyors observed price declines than increases during that period.

Key sentiment indicators from February 2026:

- Current price sentiment (London): -40% net balance

- 12-month expectations (London): +7% (down from +56%)

- Near-term national price outlook: -18% (down from -6%)

- New buyer enquiries: -26% net balance

- Agreed sales: -12% net balance [1]

The Speed and Scale of the Shift

What makes this sentiment collapse particularly noteworthy is its velocity. A 49 percentage point drop in a single month represents one of the fastest confidence deteriorations in modern UK property market history. Chartered surveyors in East London and West London reported similar patterns, suggesting the phenomenon affected the entire capital rather than specific submarkets.

"The February 2026 data represents a watershed moment for London property valuation. We're not just adjusting for typical market fluctuations—we're recalibrating our entire approach to risk assessment and comparable analysis." — Senior RICS Surveyor [2]

Regional Divergence: Why London Leads the Downturn

The London Price Sentiment Collapse: Chartered Surveyor Valuation Adjustments as 12-Month Expectations Drop from +56% to +7% stands in stark contrast to other UK regions, highlighting significant geographic disparities in market performance.

Regional Performance Breakdown

| Region | Net Balance (%) | Trend Direction | Key Factors |

|---|---|---|---|

| London | -40% | ⬇️ Strongly negative | High prices, affordability constraints, economic uncertainty |

| South East | -24% | ⬇️ Negative | Spillover from London, commuter belt concerns |

| East Anglia | -26% | ⬇️ Negative | Regional economic headwinds |

| Northern Ireland | Positive | ⬆️ Growth | Relative affordability, local demand |

| Scotland | Positive | ⬆️ Growth | Stable economic conditions |

| North West | Positive | ⬆️ Growth | Strong regional fundamentals [1] |

Why London Faces Unique Pressures

Several factors converge to explain London's disproportionate sentiment decline:

- Affordability ceiling reached: London property prices had reached historic highs relative to local incomes, creating natural resistance to further appreciation

- International buyer retreat: Geopolitical uncertainty and Middle East conflict escalation reduced overseas investment appetite [1]

- Mortgage rate sensitivity: Higher absolute prices mean London buyers face greater monthly payment increases from rate rises

- Work-from-home normalization: Reduced office attendance permanently altered location value calculations

- Stamp duty burden: Higher transaction costs in premium price brackets dampen market liquidity

Chartered surveyors in North London report that prime areas previously insulated from market cycles now experience similar sentiment shifts as outer boroughs, suggesting the downturn transcends traditional submarket boundaries.

The Macroeconomic Context

The February 2026 sentiment collapse didn't occur in isolation. Multiple macroeconomic headwinds converged simultaneously:

- Renewed inflationary pressures pushed mortgage interest rates higher than anticipated

- Middle East conflict escalation created geopolitical uncertainty affecting investment decisions

- Economic growth concerns dampened consumer confidence across all sectors

- Fiscal policy uncertainty regarding property taxation created hesitancy among buyers [1]

These factors disproportionately affected London due to its higher exposure to international capital flows and discretionary buyer segments.

Chartered Surveyor Valuation Adjustments: Practical Techniques for Volatile Markets

The London Price Sentiment Collapse: Chartered Surveyor Valuation Adjustments as 12-Month Expectations Drop from +56% to +7% necessitates sophisticated methodological adaptations by valuation professionals. Traditional approaches designed for stable markets require enhancement when sentiment shifts this dramatically [2].

Enhanced Comparable Analysis Methodology

Standard comparable analysis—the foundation of residential valuation—requires significant refinement in volatile conditions. Local chartered surveyors now implement several advanced techniques:

Time-Weighted Comparable Selection

Rather than using a standard six-month comparable window, surveyors now apply time-weighted adjustments that prioritize recent transactions:

- 0-30 days old: 100% weighting (no adjustment)

- 31-60 days old: 95% weighting (-5% adjustment)

- 61-90 days old: 90% weighting (-10% adjustment)

- 91-120 days old: 85% weighting (-15% adjustment)

- Beyond 120 days: Generally excluded unless market-adjusted [2]

This approach ensures valuations reflect current market sentiment rather than outdated transaction evidence.

Market Condition Overlays

Surveyors incorporate sentiment-based market condition adjustments derived from RICS survey data:

- When regional net balance drops below -30%, apply 2-5% downward adjustment to comparable evidence

- When 12-month expectations collapse >40 percentage points in single month, implement enhanced buyer motivation analysis

- Cross-reference agreed sale prices with asking prices to identify negotiation patterns [2]

Risk-Adjusted Valuation Approaches

Professional valuers increasingly adopt risk-adjusted methodologies that explicitly account for market uncertainty:

Scenario-Based Valuation Ranges

Rather than single-point valuations, many methods of valuation now incorporate three scenarios:

- Optimistic scenario (+5% from base): Assumes market stabilization and sentiment recovery

- Base scenario (reference point): Reflects current comparable evidence with standard adjustments

- Pessimistic scenario (-5% to -10% from base): Accounts for continued sentiment deterioration

This approach provides clients with realistic expectation ranges rather than false precision [2].

Discount Rate Adjustments for Investment Properties

For buy-to-let and investment valuations, surveyors increase discount rates to reflect elevated market risk:

- Standard market conditions: 4-5% discount rate

- Moderate volatility (-20% to -30% net balance): 5-6% discount rate

- High volatility (below -30% net balance): 6-7% discount rate

Higher discount rates reduce present values, appropriately reflecting increased investment risk in uncertain markets [2].

Submarket Segmentation Analysis

The London market isn't monolithic. Sophisticated valuation adjustments recognize distinct submarket behaviors:

Prime central areas (Chelsea, Kensington, Westminster):

- Greater international buyer exposure requires enhanced geopolitical risk assessment

- Chartered surveyors in Chelsea apply specific adjustments for currency fluctuation impacts

- Luxury segment typically experiences amplified volatility in both directions

Established residential zones (Camden, Hampstead, Barnes):

- Chartered surveyors in Camden and Hampstead focus on owner-occupier fundamentals

- School catchment areas provide relative stability

- Surveyors in Barnes note family buyer resilience

Emerging areas (Clapham, Ealing, Hounslow):

- Chartered surveyors in Clapham, Ealing, and Hounslow apply growth trajectory adjustments

- Transport infrastructure developments remain value anchors

- First-time buyer segments show different sensitivity patterns [3]

Supply-Demand Imbalance Factors

February 2026 data revealed interesting supply dynamics that inform valuation adjustments:

- New instructions: +2% net balance (neutral, indicating stable listing flow)

- Landlord instructions: -27% net balance (subdued rental supply)

- Tenant demand: +2% net balance (stable rental demand)

This supply-demand configuration suggests rental market resilience even as sales sentiment collapses, creating valuation implications for buy-to-let properties that may outperform pure capital appreciation expectations [1].

Documentation and Justification Requirements

Given the London Price Sentiment Collapse: Chartered Surveyor Valuation Adjustments as 12-Month Expectations Drop from +56% to +7%, enhanced documentation becomes critical:

✅ Essential documentation elements:

- Explicit statement of valuation date and market conditions prevailing

- Reference to RICS survey data and regional net balance figures

- Detailed comparable analysis showing time adjustments applied

- Clear explanation of any market condition overlays or risk adjustments

- Scenario analysis or valuation range where appropriate

- Statement of assumptions and special assumptions

- Limitation clauses addressing market volatility [2]

This comprehensive approach protects both surveyors and clients by creating transparency around valuation uncertainty.

Buyer and Seller Implications: Navigating the Sentiment Shift

The London Price Sentiment Collapse: Chartered Surveyor Valuation Adjustments as 12-Month Expectations Drop from +56% to +7% creates distinct strategic considerations for different market participants.

For Property Buyers 🏡

Advantages in current market:

- Enhanced negotiating position: -26% buyer enquiry balance means less competition for available properties

- Realistic valuations: Surveyor adjustments ensure mortgage valuations reflect current conditions rather than inflated comparables

- Motivated sellers: Agreed sales at -12% indicate sellers increasingly willing to negotiate

Strategic considerations:

- Commission comprehensive surveys from experienced professionals who understand current market dynamics

- Consider choosing the right property survey that addresses both structural and valuation concerns

- Build contingency into financial planning for potential further value adjustments

- Focus on long-term ownership horizons rather than short-term appreciation expectations

For Property Sellers 📊

Current market realities:

- Buyer sentiment has deteriorated significantly with enquiries down substantially

- Professional valuations now incorporate downward adjustments for market conditions

- Time-on-market likely to extend compared to late 2025 performance

Recommended approaches:

- Obtain professional valuation from qualified Red Book valuers who understand current adjustment methodologies

- Price realistically from outset rather than testing market with inflated asking prices

- Highlight property-specific value drivers that transcend general market sentiment

- Consider timing flexibility if market position allows waiting for sentiment recovery

For Property Investors 💼

Risk-return recalibration:

The sentiment collapse fundamentally alters investment return expectations:

- Capital appreciation prospects: Reduced in near-term (12-month expectations only +7%)

- Rental yield focus: Becomes primary return driver given stable tenant demand (+2% balance)

- Risk premium: Increased discount rates mean required returns rise proportionally

Investment strategy adjustments:

- Emphasize cash-flow positive properties over pure capital growth plays

- Consider commercial property opportunities with different risk-return profiles

- Diversify geographically toward regions with positive sentiment (Scotland, Northern Ireland, North West)

- Extend investment horizons to ride out medium-term volatility [3]

The Broader UK Context: National Trends and Outlook

While London experienced the most severe sentiment collapse, national trends provide important context for understanding the capital's position within the wider market.

National Market Indicators (February 2026)

Price sentiment:

- Aggregate net balance: -12% (consistent with flat to marginally negative trend)

- Near-term expectations: -18% (down from -6% previous month)

- 12-month outlook: +33% (moderated from +43%) [1]

Transaction activity:

- New buyer enquiries: -26% (significantly weakened)

- Agreed sales: -12% (marginally softer than -9% previous month)

- New instructions: +2% (broadly stable supply) [1]

Regional Performance Spectrum

The UK property market in early 2026 exhibits unprecedented regional divergence:

Outperforming regions:

- Northern Ireland, Scotland, North West England maintain positive momentum

- Relative affordability and local economic strength support continued growth

- Less exposure to international capital flow volatility

Underperforming regions:

- London (-40%), South East (-24%), East Anglia (-26%) face downward pressure

- Historic price levels create affordability constraints

- Greater sensitivity to macroeconomic headwinds [1]

This geographic split suggests fundamentals matter more than ever—regions with sustainable price-to-income ratios and strong local economies demonstrate resilience while overheated markets correct [3].

Forward-Looking Indicators

Despite London's sentiment collapse, several factors suggest the national market may stabilize:

- Supply remains constrained: +2% new instructions indicate no flood of distressed listings

- Rental market stability: Continued tenant demand provides alternative property market support

- Employment remains solid: Labor market strength underpins mortgage serviceability

- Regional diversification: Strong performance in multiple regions offsets London weakness

However, macroeconomic risks persist: renewed inflation, geopolitical uncertainty, and potential further interest rate impacts could extend the sentiment downturn beyond current expectations [1].

Practical Guidance for Engaging Chartered Surveyors in 2026

Given the London Price Sentiment Collapse: Chartered Surveyor Valuation Adjustments as 12-Month Expectations Drop from +56% to +7%, selecting and working with qualified surveyors requires enhanced diligence.

Questions to Ask Your Surveyor

When commissioning valuations or surveys in the current market, ask:

-

"How are you adjusting for the February 2026 sentiment collapse in your comparable analysis?"

- Competent surveyors should articulate specific time-weighting and market condition adjustments

-

"What RICS survey data are you incorporating into your valuation methodology?"

- Professional valuers reference regional net balance figures and sentiment indicators

-

"Can you provide a valuation range rather than a single-point figure?"

- Scenario-based approaches demonstrate sophisticated understanding of market uncertainty

-

"How does your valuation account for submarket-specific factors?"

- London isn't homogeneous—prime, established, and emerging areas behave differently

-

"What assumptions underpin your 12-month value projection?"

- Understanding assumption sensitivity helps assess valuation reliability [2]

Red Flags to Watch For

⚠️ Warning signs of inadequate methodology:

- Reliance on comparables older than 90 days without market adjustments

- Single-point valuations without acknowledgment of uncertainty ranges

- No reference to current RICS sentiment data or regional trends

- Generic London-wide analysis without submarket segmentation

- Overly optimistic 12-month projections inconsistent with +7% surveyor expectations

Selecting Qualified Professionals

In volatile markets, surveyor qualifications and experience matter more than ever:

✅ Essential credentials:

- RICS membership (MRICS or FRICS designation)

- Local market expertise in specific London submarket

- Recent valuation experience in current market conditions (2025-2026)

- Red Book compliance for formal valuations

- Professional indemnity insurance appropriate to valuation amount

Consider engaging surveyors with demonstrated expertise in your specific area, whether that's chartered surveyors in Bexley, Kingston, or Twickenham—local knowledge proves invaluable during periods of rapid sentiment shifts [3].

Looking Ahead: Market Recovery Scenarios and Timing

The London Price Sentiment Collapse: Chartered Surveyor Valuation Adjustments as 12-Month Expectations Drop from +56% to +7% raises natural questions about recovery timing and trajectory.

Potential Recovery Pathways

Optimistic scenario (6-12 months):

- Macroeconomic headwinds ease with inflation stabilization

- Mortgage rates decline as Bank of England pivots policy

- Geopolitical tensions de-escalate, restoring international buyer confidence

- Sentiment rebounds toward neutral (0%) by Q4 2026

- 12-month expectations recover to +20-30% range [3]

Base case scenario (12-18 months):

- Gradual sentiment stabilization as market adjusts to new pricing reality

- London prices remain flat to slightly negative through 2026

- Regional divergence persists with northern markets outperforming

- Recovery begins in H2 2026 but remains subdued

- 12-month expectations stabilize around +10-15% range [1]

Pessimistic scenario (18-24+ months):

- Macroeconomic conditions deteriorate further

- Additional interest rate increases compound affordability challenges

- Sentiment continues declining below February 2026 levels

- Extended price correction of 5-10% in London

- Recovery delayed until 2027 or beyond [3]

Leading Indicators to Monitor

Market participants should track several key metrics to gauge recovery timing:

📈 Sentiment indicators:

- RICS net balance figures (monthly)

- 12-month expectation trends

- Regional divergence patterns

📊 Transaction metrics:

- New buyer enquiry levels

- Agreed sales volumes

- Time-on-market statistics

💰 Economic fundamentals:

- Mortgage interest rate trends

- Inflation trajectory

- Employment and wage growth

- Consumer confidence indices [1]

Strategic Positioning for Recovery

For buyers: The current environment may represent opportunity, but timing remains uncertain. Focus on:

- Properties with strong intrinsic value drivers beyond market sentiment

- Locations with solid long-term fundamentals

- Realistic financing that doesn't depend on immediate appreciation

For sellers: Consider whether current sale is necessary or if waiting for sentiment stabilization makes strategic sense

For investors: Market dislocations create potential opportunities for those with:

- Long investment horizons (5+ years)

- Strong cash flow focus over capital appreciation

- Risk tolerance for continued near-term volatility [3]

Conclusion

The London Price Sentiment Collapse: Chartered Surveyor Valuation Adjustments as 12-Month Expectations Drop from +56% to +7% represents a defining moment for the capital's property market in 2026. This 49 percentage point collapse in professional confidence—the steepest regional decline in the UK at -40% net balance—demands sophisticated responses from all market participants.

For chartered surveyors, the sentiment shift necessitates enhanced valuation methodologies incorporating time-weighted comparable analysis, risk-adjusted discount rates, market condition overlays, and comprehensive scenario planning. Traditional approaches designed for stable markets prove inadequate when professional expectations shift this dramatically in a single month.

For property buyers, the current environment offers enhanced negotiating positions and more realistic valuations, but requires careful selection of experienced surveyors who understand current market dynamics and implement appropriate adjustment techniques.

For property sellers and investors, the collapse demands realistic pricing expectations, extended time horizons, and strategic focus on properties with strong fundamentals that transcend general market sentiment.

The dramatic regional divergence—with London, the South East, and East Anglia experiencing significant downward pressure while Northern Ireland, Scotland, and the North West maintain positive momentum—underscores that location and fundamentals matter more than ever. Sustainable price-to-income ratios, local economic strength, and reduced exposure to international capital flows provide relative stability.

Actionable Next Steps

✅ If you're buying or selling London property:

- Commission professional valuations from qualified RICS surveyors with current market expertise

- Request explicit documentation of adjustment methodologies and market condition overlays

- Consider scenario-based valuation ranges rather than single-point figures

- Build contingency into financial planning for potential further adjustments

✅ If you're a property investor:

- Reassess return expectations with focus on rental yield over capital appreciation

- Evaluate geographic diversification toward regions with positive sentiment

- Extend investment horizons to ride out medium-term volatility

- Engage specialists in commercial valuation for alternative opportunities

✅ If you're a property professional:

- Enhance valuation documentation with explicit market condition references

- Implement time-weighted comparable selection protocols

- Develop scenario-based valuation approaches for client transparency

- Monitor RICS monthly survey data for ongoing sentiment trends

The London property market has entered a period of recalibration after years of sustained growth. While the February 2026 sentiment collapse appears dramatic, it may ultimately represent a necessary correction toward more sustainable long-term fundamentals. Those who adapt their strategies, engage qualified professionals, and maintain realistic expectations will be best positioned to navigate this challenging environment and capitalize on eventual recovery.

For expert guidance navigating the current London property market with sophisticated valuation approaches tailored to high-volatility conditions, consider engaging experienced professionals who understand the nuances of the London Price Sentiment Collapse: Chartered Surveyor Valuation Adjustments as 12-Month Expectations Drop from +56% to +7% and can provide the detailed analysis your property decisions require in 2026.

References

[1] UK Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf

[2] Valuation Adjustments For Londons February 2026 Price Slump Rics Techniques For 40 Net Balances – https://nottinghillsurveyors.com/blog/valuation-adjustments-for-londons-february-2026-price-slump-rics-techniques-for-40-net-balances

[3] Building Survey Market Sentiment In Early 2026 Navigating Regional Price Divergence And Buyer Uncertainty – https://nottinghillsurveyors.com/blog/building-survey-market-sentiment-in-early-2026-navigating-regional-price-divergence-and-buyer-uncertainty