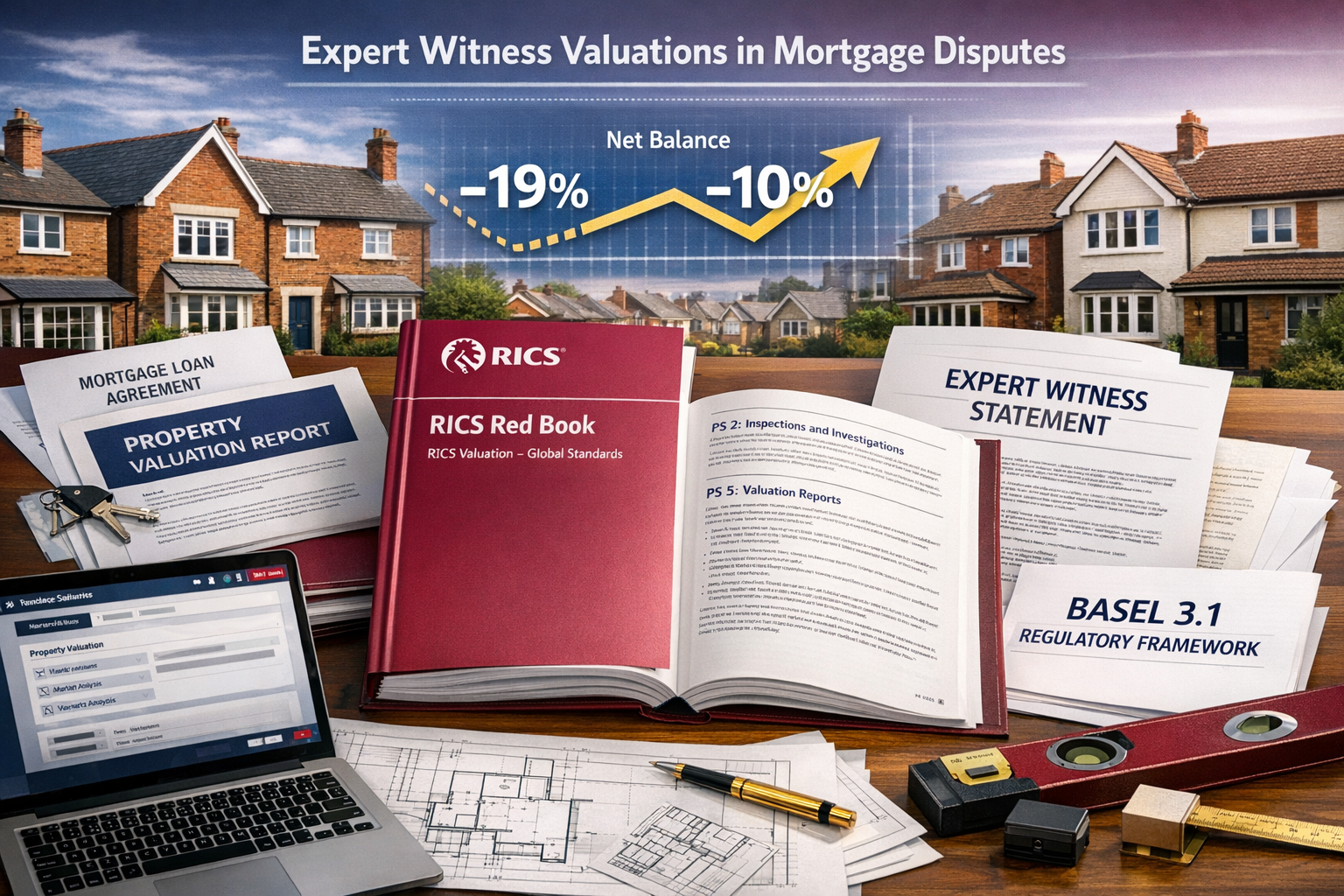

The UK property market has weathered significant turbulence over recent years, but 2026 brings a welcome shift. As property values show tentative signs of stabilization—with the latest RICS UK Residential Market Survey reporting a net balance of -10% on price growth, a marked improvement from -19%[9]—a new challenge emerges for lenders, borrowers, and property professionals alike. Expert Witness Valuations in Mortgage Disputes: Leveraging RICS Standards as Property Values Stabilize in 2026 has become increasingly critical as disagreements over property valuations intensify during this transitional period. With mortgage lenders implementing stricter Basel 3.1 requirements and borrowers questioning conservative assessments, the demand for qualified expert witnesses who can navigate complex valuation disputes has never been higher.

The convergence of regulatory change and market stabilization creates a perfect storm for valuation disputes. When property values fluctuate, even marginally, the gap between borrower expectations and lender assessments widens. This is where RICS-qualified expert witnesses become invaluable—providing independent, defensible valuations that courts and tribunals trust. For property professionals, understanding how to leverage RICS standards in dispute resolution represents both a significant opportunity and a professional obligation.

Key Takeaways

✅ Market stabilization in 2026 creates increased valuation disputes as lenders apply stricter Basel 3.1 criteria while borrowers challenge conservative assessments during recovery periods.

✅ RICS standards provide the gold standard framework for expert witness valuations, with courts placing significant weight on evidence from RICS-qualified valuers due to their independence and methodological rigor.

✅ New Basel 3.1 regulations introduce "prudently conservative valuation criteria" effective January 1, 2026, fundamentally changing how mortgage lending valuations are conducted in EU jurisdictions[4].

✅ Expert witness surveyors must master both Market Value and Mortgage Lending Value (MLV) frameworks to effectively navigate disputes in the evolving regulatory landscape.

✅ Comprehensive documentation and adherence to RICS Red Book standards significantly reduce professional risk and increase the admissibility of expert evidence in litigation, arbitration, and mediation proceedings.

Understanding the 2026 Property Market Landscape and Valuation Disputes

The Current State of Property Value Stabilization

The UK residential property market has entered a critical phase of stabilization in 2026. According to the latest RICS UK Residential Market Survey for January 2026, several key indicators have become notably less downbeat, with house prices appearing to have stabilized at a national level[9]. This represents a significant shift from the downward pressure experienced throughout 2024 and 2025.

Key market indicators for 2026 include:

- 📊 Net balance on price growth improved to -10% from -19%

- 🏠 Stabilization occurring across most UK regions

- 💰 Lender confidence gradually returning with stricter criteria

- 📈 Transaction volumes showing modest recovery

- ⚖️ Increased divergence between buyer and lender valuations

This stabilization period, while positive overall, creates particular challenges for mortgage lending. When markets are in rapid decline or growth, valuation trends are clear. However, during stabilization, micro-market variations become more pronounced, leading to legitimate disagreements about property values. A property in one postcode might genuinely be worth 5-10% more than a comparable property just streets away, creating fertile ground for disputes.

Why Valuation Disputes Are Increasing in 2026

The convergence of several factors has led to a marked increase in mortgage-related valuation disputes:

Regulatory pressure: The implementation of Basel 3.1 requirements has introduced "prudently conservative valuation criteria" that fundamentally change how lenders assess property values[4]. These new standards, which became effective January 1, 2026, require valuers to apply more conservative methodologies, often resulting in lower valuations than borrowers expect.

Market psychology: After years of price corrections, borrowers have become more sensitive to valuation outcomes. A valuation that comes in even 5% below asking price can derail a transaction or force renegotiation, leading parties to seek expert witness opinions to support their positions.

Lender risk aversion: Financial institutions remain cautious about overexposure to property risk. This conservative stance means they're more likely to challenge optimistic valuations, even in stabilizing markets.

Information asymmetry: Borrowers increasingly have access to online valuation tools and comparable sales data, leading them to question professional valuations that don't align with their research—even when the professional assessment is more accurate.

The Role of Expert Witnesses in Resolving Valuation Conflicts

When valuation disputes escalate beyond informal negotiation, they often require formal dispute resolution through litigation, arbitration, or mediation. This is where Expert Witness Valuations in Mortgage Disputes: Leveraging RICS Standards as Property Values Stabilize in 2026 becomes essential.

Courts place significant weight on expert evidence from RICS-qualified valuers who demonstrate experience, independence, and appropriate qualifications[3]. An expert witness surveyor provides independent evidence that can resolve complex disputes by applying rigorous, defensible methodologies that both parties and the court can trust.

"RICS valuations are widely accepted as expert evidence in court proceedings because of their structure and transparency. They are often admissible in property litigation and arbitration cases." [2]

The expert witness role extends beyond simply providing a number. It involves:

- Comprehensive analysis of comparable sales and market conditions

- Detailed documentation of valuation methodology and assumptions

- Independent assessment free from client influence

- Court-ready reporting that withstands cross-examination

- Professional testimony explaining complex valuation concepts to non-specialists

RICS Standards Framework for Expert Witness Valuations in Mortgage Disputes

The RICS Red Book: Foundation of Credible Valuations

The RICS Valuation – Global Standards (commonly known as the Red Book) forms the cornerstone of professional property valuation practice. For expert witnesses involved in mortgage disputes, adherence to Red Book standards is not optional—it's fundamental to credibility and admissibility of evidence.

The Red Book provides a comprehensive framework that ensures:

- ✅ Consistency in valuation approaches across different valuers

- ✅ Transparency in methodology and assumptions

- ✅ Independence from undue client influence

- ✅ Competence through mandatory professional qualifications

- ✅ Accountability via professional standards and ethics

When providing RICS building surveys and valuations for dispute resolution, expert witnesses must demonstrate strict compliance with Red Book requirements. This includes proper terms of engagement, disclosure of conflicts of interest, appropriate use of valuation bases, and comprehensive reporting standards.

Market Value vs. Mortgage Lending Value: Critical Distinctions

Understanding the distinction between Market Value and Mortgage Lending Value (MLV) is crucial for Expert Witness Valuations in Mortgage Disputes: Leveraging RICS Standards as Property Values Stabilize in 2026.

Market Value remains the cornerstone of UK lending frameworks. RICS reaffirms that valuers providing market value assessments for secured lending should continue following the RICS Valuation – Global Standards[5]. Market Value represents:

- The estimated amount for which an asset should exchange

- On the valuation date

- Between a willing buyer and willing seller

- In an arm's-length transaction

- After proper marketing

- Where parties acted knowledgeably, prudently, and without compulsion

Mortgage Lending Value (MLV), particularly relevant in EU jurisdictions implementing Basel 3.1, introduces additional conservative criteria. The new RICS Bank lending valuations and mortgage lending value, 2nd edition Professional Standard effective January 1, 2026, provides updated guidance on integrating Basel 3.1 criteria into the MLV framework[4].

| Aspect | Market Value | Mortgage Lending Value |

|---|---|---|

| Time horizon | Current market conditions | Long-term sustainable value |

| Market cycles | Reflects current cycle position | Smooths cyclical fluctuations |

| Special purchaser | May include special value | Excludes speculative elements |

| Regulatory basis | RICS Red Book | Basel 3.1 + RICS standards |

| Risk approach | Balanced assessment | Prudently conservative |

| Primary use | UK secured lending | EU regulatory compliance |

For expert witnesses, articulating these distinctions clearly is essential when disputes arise from differences between borrower expectations (often based on Market Value) and lender requirements (increasingly based on MLV or conservative Market Value interpretations).

Basel 3.1 Implementation and Prudently Conservative Criteria

The introduction of Basel 3.1 represents significant regulatory change that has major impact on how property valuations are conducted for secured lending[4]. Two major RICS publications released specifically address this implementation:

- Bank lending valuations and mortgage lending value, 2nd edition Professional Standard (Europe) – mandatory guidance for RICS members

- Bank lending valuations: Basel 3.1 prudently conservative valuation criteria adjustments, 1st edition Practice Information (Global) – interpretative guidance

The Practice Information is issued as guidance rather than instruction to reflect the variable and evolving nature of Basel 3.1 implementation across different jurisdictions[1]. This flexibility is necessary but creates potential for disputes when different valuers interpret "prudently conservative" criteria differently.

Key prudently conservative criteria include:

- 🔍 Enhanced market analysis requiring deeper comparable evidence

- 📉 Downward adjustments for market volatility and uncertainty

- ⏰ Extended marketing periods in valuation assumptions

- 🏗️ Conservative treatment of development potential

- 🔄 Stress testing against adverse market scenarios

For expert witnesses navigating mortgage disputes in 2026, understanding how these criteria should be applied—and when they may have been misapplied—is critical. A valuation that appears conservative may be entirely appropriate under Basel 3.1 standards, or it may represent overly cautious interpretation that disadvantages the borrower.

Professional Standards for Expert Witness Independence

RICS standards place particular emphasis on independence and objectivity when valuers act as expert witnesses. The duty to the court or tribunal supersedes any duty to the instructing party—a principle that distinguishes true expert evidence from advocacy.

Key independence requirements include:

Conflict disclosure: Expert witnesses must identify and disclose any potential conflicts of interest before accepting instructions. This includes previous relationships with parties, financial interests in the outcome, or any circumstance that might reasonably be perceived as affecting objectivity.

Separate instructions: When acting as an expert witness, the valuer should receive instructions directly related to the dispute resolution process, separate from any previous advisory role. Ideally, expert witnesses should not have been involved in the original transaction valuation.

Transparent methodology: All assumptions, limitations, and methodological choices must be clearly documented and justified. This transparency allows opposing experts and the court to understand and evaluate the reasoning behind the valuation conclusion.

Proportionate investigations: The extent of investigation should be appropriate to the dispute's complexity and value. For high-value mortgage disputes, this typically requires comprehensive valuation reports with extensive comparable evidence and detailed property inspection.

Practical Application: Conducting Expert Witness Valuations for Mortgage Disputes

Pre-Instruction Considerations and Conflict Checks

Before accepting instructions to provide Expert Witness Valuations in Mortgage Disputes: Leveraging RICS Standards as Property Values Stabilize in 2026, several critical preliminary steps must be completed:

Competence assessment: The expert must honestly evaluate whether they possess the necessary expertise for the specific property type, location, and dispute context. RICS standards apply to all property types—commercial, residential, industrial, and special-purpose—but expertise in one sector doesn't automatically transfer to another[2].

Conflict identification: Comprehensive conflict checks should examine:

- Previous instructions involving the same property

- Relationships with any party to the dispute

- Financial interests in the outcome

- Professional relationships that might create bias perception

- Other instructions that might create time pressure affecting quality

Resource availability: Expert witness work often requires significant time investment for investigation, report preparation, and potential court attendance. Accepting instructions without adequate resources compromises quality and professional obligations.

Terms of engagement: Clear written terms should establish scope of work, fee arrangements, timetable, and mutual obligations. For expert witness work, fees should never be contingent on outcome or valuation conclusion.

Investigation and Evidence Gathering Methodology

Thorough investigation forms the foundation of credible expert witness valuations. The depth of investigation should be proportionate to the dispute's significance but must always meet minimum professional standards.

Property inspection: A comprehensive physical inspection is typically essential, similar in scope to a RICS building survey. The inspection should document:

- Overall condition and construction quality

- Any defects, repairs, or alterations

- Compliance with building regulations

- Environmental factors affecting value

- Unique features or limitations

- Photographic evidence of key aspects

Comparable evidence: Market evidence must be robust and relevant. In 2026's stabilizing market, particular attention should be paid to:

- Transaction timing: Recent comparables (within 3-6 months) are most relevant in transitional markets

- Adjustment transparency: All adjustments for differences between subject property and comparables must be clearly justified

- Market segment: Comparables should reflect the same market segment and buyer profile

- Verification: Evidence should be verified from reliable sources, not just online portals

Regulatory context: Understanding the specific regulatory requirements applicable to the dispute is crucial. Was the original valuation conducted under Market Value or MLV? Were Basel 3.1 criteria applicable? Were they correctly applied?

Documentary evidence: Collect and review all relevant documentation:

- Original valuation reports

- Mortgage application materials

- Property marketing information

- Planning permissions and building control approvals

- Title documents and legal restrictions

- Previous survey reports or structural surveys

Report Structure and Content Requirements

An expert witness valuation report for mortgage disputes must meet both RICS professional standards and legal admissibility requirements. The structure should facilitate clear understanding by legal professionals and potentially lay tribunal members.

Essential report components:

1. Executive Summary

- Clear statement of valuation conclusion

- Brief summary of key factors affecting value

- Identification of critical issues in dispute

2. Instructions and Scope

- Who instructed the expert and when

- Specific questions to be addressed

- Scope and limitations of investigation

- Confirmation of independence and qualifications

3. Property Description

- Comprehensive description from inspection

- Location and market context

- Construction and condition assessment

- Any factors materially affecting value

4. Market Analysis

- Overview of relevant market conditions in 2026

- Analysis of market stabilization trends

- Identification of comparable evidence

- Discussion of market value range

5. Valuation Methodology

- Explanation of approach adopted (comparative, investment, etc.)

- Justification for methodology selection

- Discussion of alternative approaches considered

- Application of RICS standards and any regulatory requirements

6. Comparable Analysis

- Detailed schedule of comparable transactions

- Adjustments applied with clear justification

- Analysis of value indicators

- Reconciliation of evidence to valuation conclusion

7. Special Considerations

- Application of Basel 3.1 criteria if relevant

- Treatment of any special purchaser considerations

- Discussion of any unusual features or limitations

- Risk factors and assumptions

8. Valuation Conclusion

- Clear statement of Market Value or MLV

- Valuation date specification

- Any qualifications or caveats

- Confidence level in conclusion

9. Declaration and Qualifications

- Confirmation of independence

- Statement of qualifications and experience

- Acknowledgment of duty to court/tribunal

- Declaration of truthfulness

Common Valuation Disputes and Resolution Approaches

Understanding typical dispute scenarios helps expert witnesses anticipate issues and structure their analysis effectively.

Scenario 1: Downvaluation Below Purchase Price

Situation: Lender's valuation comes in 10% below agreed purchase price, threatening transaction completion.

Expert approach: Analyze whether the purchase price reflected special purchaser considerations not captured in Market Value, whether comparable evidence was appropriately selected and adjusted, and whether any Basel 3.1 conservatism was appropriately or excessively applied. Consider whether choosing the right property survey initially might have identified value concerns earlier.

Scenario 2: Divergent Expert Opinions

Situation: Borrower's expert values property at £500,000; lender's expert at £450,000.

Expert approach: Conduct independent analysis focusing on comparable selection criteria, adjustment methodology, and any differences in property condition assessment. Identify whether differences stem from methodological choices, market interpretation, or factual disagreements about property characteristics.

Scenario 3: Market Value vs. MLV Confusion

Situation: Borrower disputes valuation without understanding it was conducted under MLV rather than Market Value.

Expert approach: Clearly articulate the distinction between valuation bases, explain why MLV produces lower figures in current market conditions, and assess whether the MLV was correctly calculated according to Basel 3.1 criteria and RICS standards.

Scenario 4: Defect Impact Disputes

Situation: Disagreement over how structural issues or defects should affect value.

Expert approach: Coordinate with structural engineers if necessary, obtain repair cost estimates, analyze market perception of similar defects, and apply appropriate deductions based on market evidence rather than just repair costs. Reference specialist defect surveys where appropriate.

Building Expertise and Capitalizing on Growing Demand

Professional Development for Expert Witness Work

The growing demand for Expert Witness Valuations in Mortgage Disputes: Leveraging RICS Standards as Property Values Stabilize in 2026 creates significant opportunities for qualified surveyors. However, effective expert witness work requires skills beyond technical valuation competence.

Essential competencies include:

Technical mastery: Deep understanding of RICS valuation standards, Basel 3.1 requirements, and market analysis methodologies. This requires ongoing professional development as standards evolve. The January 2026 updates to bank lending valuation standards demonstrate the need for continuous learning[1].

Communication skills: Ability to explain complex valuation concepts clearly to legal professionals and lay tribunal members. Expert witnesses must translate technical jargon into accessible language without oversimplifying.

Report writing: Skill in producing comprehensive, well-structured reports that withstand scrutiny. Reports must be thorough yet concise, technically rigorous yet readable.

Cross-examination preparation: Comfort with having opinions challenged and ability to defend methodology under questioning. This requires confidence in the underlying analysis and honest acknowledgment of limitations.

Professional judgment: Capacity to maintain independence and objectivity despite pressure from instructing parties. The expert's duty to the court supersedes client relationships.

Recommended development pathway:

- Achieve RICS Registered Valuer status – demonstrates competence and commitment to professional standards

- Specialize in specific property sectors – develop deep expertise in residential, commercial, or specialized properties

- Pursue expert witness training – formal courses on expert witness duties and court procedures

- Shadow experienced experts – learn practical aspects of dispute resolution

- Start with lower-value disputes – build experience before tackling complex, high-value cases

- Join professional networks – engage with other expert witnesses to share knowledge and best practices

Marketing Expert Witness Services in 2026

As demand for expert valuations increases with market stabilization, positioning services effectively becomes crucial for building a sustainable expert witness practice.

Target audiences include:

- Legal firms specializing in property litigation

- Mortgage lenders requiring independent dispute resolution

- Borrowers and buyers challenging lender valuations

- Arbitration and mediation services

- Professional indemnity insurers managing valuation claims

Effective positioning strategies:

Demonstrate RICS credentials prominently: Research shows that 78% of cross-border real estate investment firms in North America required RICS-aligned valuations in their acquisition due diligence[2]. This demonstrates the global recognition of RICS standards and the value of highlighting RICS qualifications.

Develop case studies: (While maintaining confidentiality) showcase expertise through anonymized examples of dispute resolution, demonstrating methodology and outcomes.

Publish thought leadership: Write articles analyzing current valuation challenges, regulatory changes like Basel 3.1, and market trends. This establishes expertise and visibility.

Build legal network relationships: Attend property law conferences, join relevant professional associations, and develop relationships with legal professionals who instruct expert witnesses.

Maintain online presence: Ensure professional website clearly articulates expert witness services, qualifications, and areas of specialization. Include testimonials from legal professionals (with permission).

Emphasize risk mitigation: RICS valuations mitigate professional risk by significantly reducing the risk of overvaluation, undervaluation, tax exposure, and professional challenge through disciplined methodologies[3]. Position expert witness services as risk management tools for all parties.

Fee Structures and Business Considerations

Expert witness work typically commands premium fees reflecting the specialized nature of the service, professional risk, and time commitment required.

Common fee approaches:

Hourly rates: Most appropriate for expert witness work, ensuring fees aren't contingent on outcome. Typical rates for experienced RICS-qualified expert witnesses range from £150-£400+ per hour depending on expertise, complexity, and location.

Fixed fees for specific deliverables: May be appropriate for discrete tasks like initial assessment or report preparation, with hourly rates for additional work like court attendance.

Retainer arrangements: For clients with ongoing dispute resolution needs, retainer arrangements provide predictable income and client loyalty.

Important considerations:

- ⚖️ Never make fees contingent on valuation outcome – this compromises independence

- 📝 Document time meticulously – detailed time records support fee justification

- 💼 Carry adequate professional indemnity insurance – expert witness work carries liability exposure

- 🔍 Be transparent about fees upfront – avoid disputes about costs by clear initial agreements

- ⏰ Factor in court attendance time – include preparation, travel, and waiting time in fee estimates

Risk Management and Professional Standards Compliance

Providing expert witness services carries professional and legal risks that must be carefully managed.

Key risk areas:

Professional negligence: Errors in valuation methodology, inadequate investigation, or failure to comply with RICS standards can lead to negligence claims. Mitigation strategies include thorough documentation, peer review for complex cases, and maintaining current technical knowledge.

Bias allegations: Even perception of bias can damage credibility. Maintain strict independence, document objective reasoning, and decline instructions where conflicts exist.

Regulatory compliance: Ensure all work complies with current RICS standards, including the January 2026 updates to bank lending valuation guidance[4]. Non-compliance can result in disciplinary action.

Reputational risk: Expert witness work is high-profile. Poor performance in court or flawed analysis can damage professional reputation. Only accept instructions within competence areas and maintain quality standards.

Best practices for risk management:

- ✅ Maintain comprehensive professional indemnity insurance

- ✅ Document all methodological decisions and assumptions

- ✅ Seek second opinions on complex or unusual cases

- ✅ Stay current with RICS standards updates and market developments

- ✅ Decline instructions where independence might be questioned

- ✅ Maintain detailed records of all communications and instructions

- ✅ Use standardized report templates ensuring all required elements are included

- ✅ Participate in continuing professional development focused on expert witness skills

Conclusion: Seizing Opportunities in a Stabilizing Market

As property values stabilize in 2026, the landscape for Expert Witness Valuations in Mortgage Disputes: Leveraging RICS Standards as Property Values Stabilize in 2026 presents unprecedented opportunities for qualified professionals. The convergence of market stabilization, Basel 3.1 implementation, and increased lender conservatism has created a perfect environment for valuation disputes—and therefore for expert witness services.

The improvement in market sentiment, with the net balance on price growth improving from -19% to -10%[9], signals a transitional period where valuation precision becomes critical. Neither in freefall nor rapid growth, the 2026 market requires nuanced analysis that distinguishes between genuine market value and overly conservative or optimistic assessments.

For RICS-qualified surveyors and valuers, this environment offers a clear pathway to professional growth and service diversification. By mastering both the technical requirements of RICS standards and the practical skills of expert witness work, professionals can position themselves as essential resources for dispute resolution.

Actionable Next Steps

For surveyors looking to develop expert witness capabilities:

- Review the latest RICS guidance on bank lending valuations and Basel 3.1 implementation released in January 2026

- Pursue RICS Registered Valuer status if not already achieved

- Invest in expert witness training focusing on court procedures and cross-examination preparation

- Develop relationships with property litigation solicitors in your practice area

- Create standardized report templates that meet both RICS and legal admissibility requirements

- Build a comparable evidence database for your specialist property sectors and locations

- Review and enhance professional indemnity insurance to cover expert witness activities

For lenders and borrowers facing valuation disputes:

- Understand the distinction between Market Value and Mortgage Lending Value frameworks

- Review whether Basel 3.1 criteria should apply to your specific situation

- Seek early expert opinion when significant valuation discrepancies emerge

- Ensure any expert witness you instruct is RICS-qualified and demonstrably independent

- Provide comprehensive documentation to support efficient expert analysis

- Consider alternative dispute resolution like mediation before litigation

For legal professionals instructing expert witnesses:

- Verify RICS qualifications and relevant sector expertise before instruction

- Conduct thorough conflict checks to ensure expert independence

- Provide clear, comprehensive instructions defining scope and specific questions

- Allow adequate time for thorough investigation and report preparation

- Understand current market conditions and regulatory frameworks affecting valuations

- Coordinate early between opposing experts to narrow areas of disagreement

The stabilizing property market of 2026, combined with evolving regulatory requirements and increased dispute frequency, creates a sustained demand for expert witness valuation services. Those who invest in developing the necessary technical expertise, professional skills, and market positioning will find themselves well-placed to capitalize on this growing opportunity while providing essential services that facilitate fair dispute resolution.

By leveraging RICS standards as the foundation for credible, defensible valuations, expert witnesses can help resolve conflicts efficiently, support market transparency, and maintain confidence in property transactions during this critical stabilization period. The professional surveyor who masters Expert Witness Valuations in Mortgage Disputes: Leveraging RICS Standards as Property Values Stabilize in 2026 will be positioned not just for current opportunities, but for long-term success as regulatory frameworks continue to evolve and market dynamics shift.

References

[1] Rics Updates Global Guidance On Bank Lending Valuations With Two Key Publications – https://www.rics.org/news-insights/rics-updates-global-guidance-on-bank-lending-valuations-with-two-key-publications

[2] Breaking Down The Rics Valuation What Every Valuer Should Know – https://globalvaluation.com/breaking-down-the-rics-valuation-what-every-valuer-should-know/

[3] Why A Rics Registered Valuer Is Essential For Client Valuation Needs – https://www.res-prop.com/why-a-rics-registered-valuer-is-essential-for-client-valuation-needs/

[4] Bank Lending Valuations – https://www.rics.org/profession-standards/rics-standards-and-guidance/sector-standards/valuation-standards/bank-lending-valuations

[5] Rics Update On The Pra Boe Final Rules On The Implementation Of Basel 3 Point 1 In The Uk – https://www.rics.org/profession-standards/rics-standards-and-guidance/sector-standards/valuation-standards/rics-update-on-the-pra-boe-final-rules-on-the-implementation-of-basel-3-point-1-in-the-uk

[9] Uk Resi Survey Jan 2026 Report Shows Early Signs Market Recovery Despite Caution – https://www.rics.org/news-insights/uk-resi-survey-jan-2026-report-shows-early-signs-market-recovery-despite-caution