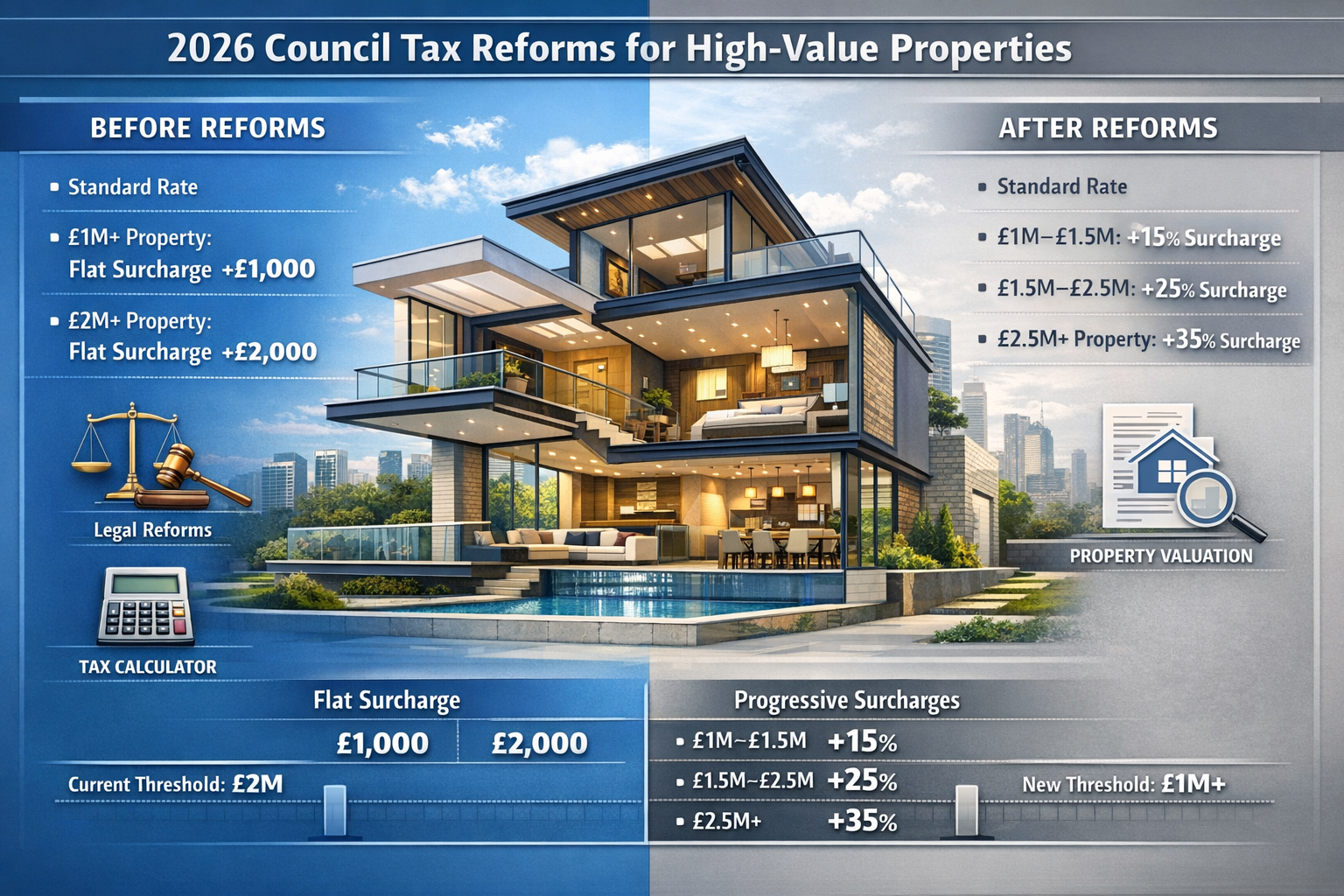

The landscape of property taxation in England is undergoing its most significant transformation in decades. As the government prepares to implement a new High Value Council Tax Surcharge affecting properties worth over £2 million from April 2028, property owners and expert witness surveyors face unprecedented challenges in valuation accuracy and dispute resolution. With over 100,000 households potentially affected and annual charges ranging from £2,500 to £7,500, understanding Expert Witness Valuations for High-Value Properties: Mitigating Council Tax Surcharge Disputes in 2026 Reforms has never been more critical for protecting property owners' interests.

The stakes are particularly high given that property values will be fixed as at 2026 and reviewed every five years[3], creating a narrow window for accurate assessment and potential challenges. This comprehensive guide examines how RICS-accredited surveyors serve as expert witnesses in valuation disputes, providing evidence-based strategies for appeals and navigating the complex terrain of high-value property taxation.

Key Takeaways

- 🏛️ New surcharge framework: Properties over £2 million face annual charges of £2,500-£7,500 starting April 2028, with valuations fixed at 2026 levels

- 📊 Geographic concentration: Approximately 85% of affected properties are in the South East, with 50% in London alone, creating regional valuation challenges

- ⚖️ Expert witness role: RICS-accredited surveyors provide critical evidence-based valuations for tribunal appeals and Valuation Office Agency challenges

- 💰 Financial impact: Successful challenges can result in substantial backdated refunds, with documented cases recovering over £15,400

- 📈 Price bunching trends: Market distortions near the £2 million threshold require sophisticated comparable evidence analysis for accurate valuations

Understanding the 2026 Council Tax Reforms and High-Value Property Surcharge

The Legislative Framework

The introduction of the High Value Council Tax Surcharge represents the most substantial reform to property taxation since the current council tax system was established in 1993. The existing council tax valuations are based on 1991 property assessments—over 30 years old as of 2026[1]—creating significant disparities between actual market values and tax assessments.

The new surcharge structure operates on a tiered system:

| Property Value | Annual Surcharge | Estimated Affected Households |

|---|---|---|

| £2-3 million | £2,500 | ~60,000 |

| £3-5 million | £5,000 | ~30,000 |

| £5 million+ | £7,500 | ~10,000 |

Total affected households: Over 100,000 across England[2]

Geographic Distribution and Market Implications

The concentration of high-value properties creates unique challenges for valuation professionals. With 50% of all properties over £2 million located in London and 85% in the South East[2], regional market expertise becomes essential for accurate assessments.

This geographic clustering also influences:

- Comparable evidence availability in specific postcodes

- Market volatility in luxury property segments

- Local authority resources for assessment and appeals

- Valuation methodology variations across regions

The 2026 Valuation Snapshot

The government's decision to fix property values as at 2026 with five-year review cycles[3] creates a critical juncture for property owners. This snapshot approach means:

✅ Properties valued at £1.95 million in 2026 avoid surcharges until the next review

❌ Properties valued at £2.05 million in 2026 face immediate surcharges from April 2028

🔄 Market fluctuations between 2026-2028 do not affect initial assessments

This mechanism incentivizes strategic timing for property valuations and creates opportunities for evidence-based challenges where assessments appear inflated.

The Role of Expert Witness Valuations for High-Value Properties in Dispute Resolution

RICS Standards and Professional Requirements

Expert witness surveyors operate under strict RICS (Royal Institution of Chartered Surveyors) guidelines that prioritize independence, objectivity, and evidence-based methodology. Unlike standard valuation reports, expert witness valuations must withstand scrutiny in tribunal proceedings and formal appeals.

Key RICS requirements for expert witnesses include:

- 🎓 Professional qualifications: RICS accreditation with specialist valuation expertise

- 📋 Duty to the tribunal: Primary obligation to the court/tribunal, not the instructing party

- 🔍 Transparent methodology: Fully documented valuation approach with clear assumptions

- 📊 Comparable evidence: Robust market data supporting conclusions

- ⚖️ Impartiality: Willingness to acknowledge weaknesses in one's own position

Evidence-Based Valuation Methodology

Expert witness valuations for council tax surcharge disputes employ sophisticated analytical frameworks that go beyond standard market valuations. The methodology typically includes:

1. Comparable Market Analysis

Identifying genuinely comparable properties requires meticulous research:

- Geographic proximity: Properties within the same postcode district or neighborhood

- Physical characteristics: Square footage, number of bedrooms, architectural features

- Condition and specification: Quality of fixtures, recent renovations, maintenance standards

- Transaction timing: Sales occurring within appropriate timeframes relative to the 2026 snapshot

2. Adjustment Calculations

Expert witnesses must quantify differences between the subject property and comparables:

Adjusted Comparable Value = Sale Price ± Location Adjustment

± Size Adjustment

± Condition Adjustment

± Time Adjustment

Example adjustment scenario:

A comparable property sold for £2.1 million but features:

- Additional 200 sq ft (+£50,000)

- Superior garden (+£75,000)

- Recent full renovation (+£100,000)

Adjusted value: £2.1M – £225,000 = £1.875 million

This adjusted value provides stronger evidence that the subject property sits below the £2 million threshold.

3. Market Conditions Analysis

Expert witnesses must account for broader market trends affecting valuations:

- Price bunching near the £2 million threshold (discussed in detail below)

- Regional market velocity and transaction volumes

- Economic indicators affecting luxury property demand

- Seasonal variations in property values

Documentation and Report Standards

A professional expert witness valuation report for council tax surcharge disputes typically contains:

Executive Summary

- Clear statement of opinion on property value as at 2026

- Summary of key evidence supporting the valuation

- Conclusion regarding surcharge applicability

Property Description

- Detailed physical characteristics

- Location analysis and neighborhood context

- Condition assessment

- Unique features affecting value

Valuation Methodology

- Explanation of approach (comparative method, residual method, etc.)

- Market data sources and research methodology

- Assumptions and limitations

Comparable Evidence

- Minimum 5-8 comparable transactions

- Detailed adjustment schedules

- Supporting documentation (sale particulars, land registry data)

Market Analysis

- Local market trends

- Price bunching analysis near thresholds

- Economic factors affecting values

Conclusion and Opinion

- Final valuation figure with confidence range

- Reasoning for conclusions

- Alternative scenarios if applicable

Price Bunching Trends and Strategic Valuation Challenges

Understanding Price Bunching Phenomena

Price bunching refers to the clustering of property transactions just below tax thresholds, creating artificial market distortions. This phenomenon becomes particularly pronounced when significant tax consequences attach to specific value points.

Evidence of price bunching near £2 million:

Research indicates that properties naturally valued between £1.95-2.05 million often transact at prices just below the threshold due to:

- Negotiation leverage: Buyers using tax implications to reduce offers

- Seller motivation: Accepting slightly lower prices to facilitate sales

- Marketing strategies: Properties listed strategically below threshold values

- Valuation bias: Unconscious tendency toward "safe" valuations

Implications for Expert Witness Valuations

Price bunching creates both challenges and opportunities for expert witnesses:

Challenges:

- 📉 Fewer genuine comparable transactions above £2 million

- 🎯 Difficulty establishing "true" market value absent tax considerations

- ⚠️ Risk of circular reasoning using bunched comparables

- 📊 Statistical anomalies in market data analysis

Opportunities:

- 💡 Demonstrating artificial market distortion strengthens appeals

- 🔍 Identifying pre-reform comparables provides cleaner evidence

- 📈 Analyzing asking prices versus achieved prices reveals bunching patterns

- ⚖️ Expert testimony explaining bunching phenomena adds credibility

Case Study: Navigating Bunching in Valuation Evidence

Scenario: A Chelsea townhouse requires valuation for 2026 surcharge assessment.

Initial market data:

- 8 comparable sales in 2025-2026: 7 sold between £1.85-1.95M, 1 sold at £2.25M

- Property characteristics suggest value around £2.0-2.1M

- Clear evidence of price bunching below £2M threshold

Expert witness approach:

- Acknowledge bunching: Report explicitly identifies market distortion

- Expand comparable search: Include pre-announcement sales (2023-2024) before bunching began

- Analyze asking prices: Compare listing prices to achieved prices, revealing £50,000-100,000 reductions near threshold

- Apply hedonic modeling: Statistical analysis controlling for property characteristics independent of tax considerations

- Provide range: Expert opinion states value between £1.95-2.05M with explanation of uncertainty

Outcome: Tribunal accepts evidence of market distortion and values property at £1.98M, avoiding surcharge.

Challenging Council Tax Assessments: Procedures and Strategies

The Valuation Office Agency Appeal Process

Homeowners can formally challenge their council tax band through the Valuation Office Agency (VOA) at no cost[1]. The process for high-value property surcharge challenges follows similar procedures with specific considerations:

Step 1: Initial Challenge Submission

- Submit challenge within specified timeframe after receiving assessment

- Provide preliminary evidence suggesting incorrect valuation

- No fee required for submission

Step 2: VOA Review

- VOA reassesses property using internal methodology

- May request additional information or property inspection

- Timeline: Typically 3-6 months for initial response

Step 3: Negotiation Phase

- Opportunity to provide additional evidence, including expert witness reports

- VOA may revise assessment based on new evidence

- Many disputes resolve at this stage without tribunal

Step 4: Valuation Tribunal

- Formal hearing if agreement cannot be reached

- Both parties present evidence and expert testimony

- Independent tribunal panel makes binding decision

Strategic Timing Considerations

The 2026 valuation snapshot creates unique timing dynamics:

Optimal challenge periods:

🗓️ Q3-Q4 2026: Challenge preliminary assessments before finalization

🗓️ Q1 2028: Final opportunity before surcharges commence

🗓️ Post-implementation: Ongoing challenges if new evidence emerges

Benefits of early engagement:

- Greater flexibility in evidence gathering

- Opportunity to influence VOA methodology

- Time to commission comprehensive expert valuations

- Reduced urgency and associated costs

Section 13A Discretionary Reductions

Beyond formal challenges, Section 13A discretionary reductions allow councils to reduce bills in cases of exceptional hardship[1]. While designed for financial hardship rather than valuation disputes, this mechanism provides an additional avenue for relief in specific circumstances:

Qualifying scenarios:

- Temporary financial difficulties preventing payment

- Significant property value decline due to local factors

- Exceptional circumstances affecting ability to pay

Application process:

- Submit application to local council (not VOA)

- Provide financial evidence and circumstances

- Council exercises discretion based on local policy

Negotiation Tactics and Evidence Presentation

Building a Compelling Evidence Package

Successful challenges require more than accurate valuations—they demand persuasive presentation of evidence that addresses potential counterarguments:

Essential components:

- Professional valuation report from RICS-accredited expert witness

- Comparable evidence package with detailed property particulars

- Market analysis demonstrating price trends and bunching

- Photographic evidence documenting property condition

- Historical valuations for tax purposes showing consistency

- Independent corroboration such as mortgage valuations or recent sale prices

Effective Negotiation Strategies

Strategy 1: The Threshold Argument

When properties genuinely sit near the £2 million threshold, emphasize valuation uncertainty and the margin of error inherent in any valuation:

"Professional valuations carry an inherent margin of error of ±5-10%. Given the subject property's estimated value of £2.0M, the true market value could reasonably range from £1.90-2.10M. Where such uncertainty exists, the principle of fairness suggests avoiding surcharge application."

Strategy 2: The Comparable Evidence Challenge

Question the VOA's comparable selection:

- Identify superior comparables supporting lower values

- Highlight inappropriate comparables used by VOA

- Demonstrate inadequate adjustment calculations

- Present alternative valuation scenarios

Strategy 3: The Market Distortion Defense

Leverage price bunching evidence:

- Show systematic undervaluation of properties near threshold

- Demonstrate that comparable transactions reflect tax avoidance rather than true value

- Argue for pre-reform comparables as more reliable evidence

- Request adjustment for artificial market conditions

Strategy 4: The Technical Specification Argument

For properties with unique characteristics:

- Emphasize features that reduce value (lease terms, building defects, planning restrictions)

- Provide specialist reports on value-reducing factors

- Commission specific defect assessments where relevant

- Highlight differences from apparently comparable properties

Tribunal Presentation Best Practices

When cases proceed to tribunal, effective presentation becomes critical:

Expert witness testimony guidelines:

✅ Speak clearly and avoid jargon: Tribunals include non-specialist members

✅ Acknowledge limitations: Credibility increases when experts recognize uncertainties

✅ Respond directly to questions: Avoid evasiveness or over-elaboration

✅ Maintain composure under cross-examination: Professional demeanor reinforces expertise

✅ Use visual aids: Charts, photographs, and maps enhance comprehension

✅ Reference authoritative sources: RICS guidance, market reports, academic research

Common pitfalls to avoid:

❌ Advocacy: Expert witnesses must remain impartial, not argue the client's case

❌ Overconfidence: Excessive certainty undermines credibility

❌ Inadequate preparation: Failure to anticipate counterarguments weakens position

❌ Inconsistency: Contradictions between written reports and oral testimony

❌ Dismissiveness: Disrespecting opposing experts or tribunal members

Financial Impact and Backdated Refunds

Calculating Potential Savings

The financial implications of successful challenges extend beyond avoiding future surcharges. Homeowners can potentially recover backdated refunds for past overpayments, with documented cases recovering £15,400[1].

Example calculation:

Scenario: Property incorrectly assessed at £2.2M (£2,500 annual surcharge)

Correct valuation: £1.95M (no surcharge)

Challenge timeline: Submitted 2029, covering 2028-2029 period

Immediate savings:

- Year 1 (2028-29): £2,500

- Year 2 (2029-30): £2,500

- Total two-year savings: £5,000

Projected five-year savings (until next revaluation):

- Years 1-5: £2,500 × 5 = £12,500

Additional considerations:

- Interest on backdated refunds (where applicable)

- Avoided future increases if surcharge rates rise

- Reduced likelihood of higher band in next revaluation

Cost-Benefit Analysis of Expert Witness Engagement

Commissioning professional expert witness valuations involves costs, but the potential returns often justify the investment:

Typical expert witness costs:

| Service Level | Cost Range | Appropriate For |

|---|---|---|

| Basic valuation report | £1,500-3,000 | Clear-cut cases with strong comparable evidence |

| Comprehensive expert report | £3,000-6,000 | Properties near threshold requiring detailed analysis |

| Full tribunal representation | £6,000-12,000+ | Complex disputes with substantial financial stakes |

Break-even analysis:

For a property facing £5,000 annual surcharge over five years (£25,000 total):

- Expert witness cost: £4,000

- Probability of success: 60%

- Expected value: (£25,000 × 0.60) – £4,000 = £11,000 net benefit

This simplified calculation demonstrates that even with moderate success probabilities, professional representation often delivers positive returns.

Regional Variations and Specialized Considerations

London and South East Concentration

The 85% concentration of affected properties in the South East[2] creates specific challenges and opportunities:

London-specific factors:

- Extreme price volatility: Rapid market fluctuations complicate 2026 snapshot valuations

- Diverse property types: From Georgian townhouses to modern penthouses requiring specialized expertise

- Leasehold complexities: Many high-value London properties are leasehold, requiring lease extension valuation considerations

- Conservation areas: Planning restrictions affecting values require specialist knowledge

South East considerations:

- Commuter premium: Proximity to London transport links significantly affects values

- School catchment areas: Educational facilities create localized value variations

- Green belt restrictions: Planning constraints influencing development potential

- Historic properties: Listed building status and associated maintenance costs

Scotland's Parallel Reforms

Scotland's plans to revalue properties worth over £1 million and introduce two new high-value property bands from 1 April 2028[4] create additional complexity for property owners with assets in multiple jurisdictions.

Key differences:

- Lower threshold (£1M vs £2M in England)

- Band-based system rather than surcharge approach

- Different valuation date and review cycles

- Separate appeal procedures

Property owners with Scottish and English holdings require coordinated valuation strategies addressing both regimes.

Commercial and Mixed-Use Properties

High-value properties serving dual residential and commercial purposes present unique valuation challenges:

Considerations for mixed-use valuations:

- Apportionment between residential and commercial elements

- Different valuation methodologies for commercial components

- Business rates implications alongside council tax

- Potential for multiple challenges across different tax regimes

Expert witnesses must possess cross-disciplinary expertise in both residential and commercial property valuation for these complex cases.

Preparing for the 2026 Valuation Snapshot

Proactive Steps for Property Owners

With the 2026 valuation snapshot approaching, high-value property owners should take immediate action:

Q1-Q2 2026:

- 📋 Commission preliminary valuation from RICS-accredited surveyor

- 🔍 Research comparable sales in local area

- 📸 Document current property condition with photographs

- 📊 Gather historical valuation evidence (mortgage valuations, prior assessments)

- 🏗️ Complete any value-reducing works before snapshot date

Q3-Q4 2026:

- 🎯 Obtain formal expert witness valuation if near threshold

- 📝 Prepare challenge documentation in advance

- 💼 Engage legal/tax advisors for coordinated strategy

- 🔄 Monitor market conditions and comparable transactions

- ⚖️ Consider strategic timing of any property transactions

Value-Reducing Strategies

For properties genuinely near the £2 million threshold, legitimate strategies may reduce assessed values:

Structural and maintenance factors:

- Document deferred maintenance requiring substantial investment

- Obtain specialist reports on building defects

- Highlight obsolete building systems requiring replacement

- Commission building surveys identifying value-affecting issues

Legal and planning considerations:

- Review restrictive covenants limiting property use

- Document planning constraints affecting development potential

- Identify adverse easements or rights of way

- Assess impact of conservation area or listed building restrictions

Market positioning:

- Avoid unnecessary improvements immediately before valuation

- Consider timing of major renovations

- Document local market conditions affecting values

- Gather evidence of comparable sales trends

⚠️ Important: All strategies must reflect genuine property characteristics and market conditions. Artificial manipulation or misrepresentation undermines credibility and may constitute fraud.

Future Outlook and Long-Term Planning

Five-Year Review Cycles

The five-year review cycle[3] creates both certainty and strategic opportunities:

Benefits:

- Predictable reassessment timeline

- Opportunity to plan for future challenges

- Stability in tax planning

Challenges:

- Properties appreciating rapidly may face significant increases at revaluation

- Market downturns may not provide immediate relief

- Accumulated market changes create larger adjustments

Strategic implications:

Property owners should:

- Maintain ongoing valuation records

- Document market conditions throughout each cycle

- Prepare evidence packages in advance of revaluation dates

- Consider impact on long-term property planning

Potential Policy Evolution

The council tax reform landscape continues evolving, with potential future developments:

Likely scenarios:

- 📈 Threshold adjustments: Inflation-linked increases to £2M threshold

- 🏛️ Band restructuring: Comprehensive council tax reform addressing 1991 valuations

- 💰 Rate changes: Modification of surcharge amounts based on revenue targets

- 🌍 Regional variations: Different approaches in devolved administrations

Implications for property owners:

- Maintain flexibility in tax planning strategies

- Monitor policy developments and consultation processes

- Engage with professional advisors for ongoing guidance

- Participate in industry consultations affecting high-value properties

Building Relationships with Expert Witnesses

Given the recurring nature of valuations and potential disputes, establishing ongoing relationships with qualified expert witness surveyors provides long-term benefits:

Advantages of continuity:

- Expert develops deep understanding of specific property

- Historical knowledge strengthens future valuations

- Established credibility with local tribunals

- Efficient response to emerging challenges

- Coordinated approach across multiple properties or transactions

Selecting the right expert witness:

✅ RICS accreditation with relevant specializations

✅ Proven tribunal experience and success record

✅ Local market expertise in relevant geographic areas

✅ Clear communication and report-writing capabilities

✅ Professional indemnity insurance coverage

✅ Availability for ongoing engagement

Conclusion

The introduction of Expert Witness Valuations for High-Value Properties: Mitigating Council Tax Surcharge Disputes in 2026 Reforms represents a watershed moment for owners of properties valued above £2 million. With over 100,000 households facing potential annual surcharges of £2,500-£7,500 and the critical 2026 valuation snapshot rapidly approaching, the role of RICS-accredited expert witnesses has never been more crucial.

Key success factors for navigating the reforms:

🎯 Early engagement: Commissioning professional valuations well before the 2026 snapshot provides maximum flexibility and strategic advantage

📊 Evidence-based approach: Robust comparable analysis, market data, and transparent methodology form the foundation of successful challenges

⚖️ Professional representation: Qualified expert witnesses provide credibility and technical expertise essential for tribunal proceedings

💰 Financial justification: With potential savings of £12,500-£37,500 over five-year cycles, professional fees often deliver substantial returns

🔄 Long-term planning: Ongoing relationships with valuation experts and proactive monitoring of policy developments ensure continued optimization

Actionable Next Steps

For property owners approaching the £2 million threshold:

- Immediate (2026): Commission preliminary valuation assessment from qualified surveyor

- Short-term (Q3-Q4 2026): Obtain formal expert witness valuation if within £100,000 of threshold

- Medium-term (2027-2028): Prepare and submit challenges if assessments appear excessive

- Long-term (2028+): Maintain ongoing valuation records and prepare for five-year review cycles

For properties significantly above thresholds:

- Understand surcharge obligations and budget accordingly

- Document property characteristics for future revaluations

- Monitor market conditions affecting values

- Consider Section 13A discretionary reductions if circumstances warrant

The council tax surcharge reforms create both challenges and opportunities. Property owners who engage proactively with qualified expert witness surveyors, develop evidence-based valuation strategies, and understand the appeal procedures position themselves to minimize tax burdens while ensuring fair and accurate assessments.

As the 2026 valuation snapshot approaches, the window for strategic action narrows. Professional guidance from experienced valuation experts provides the technical expertise, procedural knowledge, and evidentiary rigor necessary to navigate these complex reforms successfully. The investment in expert witness valuations today can deliver substantial financial benefits extending across decades of property ownership.

References

[1] Watch – https://www.youtube.com/watch?v=7RWiUy-BlhM

[2] New Property Tax – https://hoa.org.uk/news/new-property-tax/

[3] High Value Council Tax Surcharge Reform Significant Implications – https://www.taxadvisermagazine.com/article/high-value-council-tax-surcharge-reform-significant-implications

[4] Council Tax Reform In Scotland – https://www.jrf.org.uk/neighbourhoods-and-communities/council-tax-reform-in-scotland

[5] Your Council Tax 2025 26 – https://www.bathnes.gov.uk/your-council-tax-2025-26