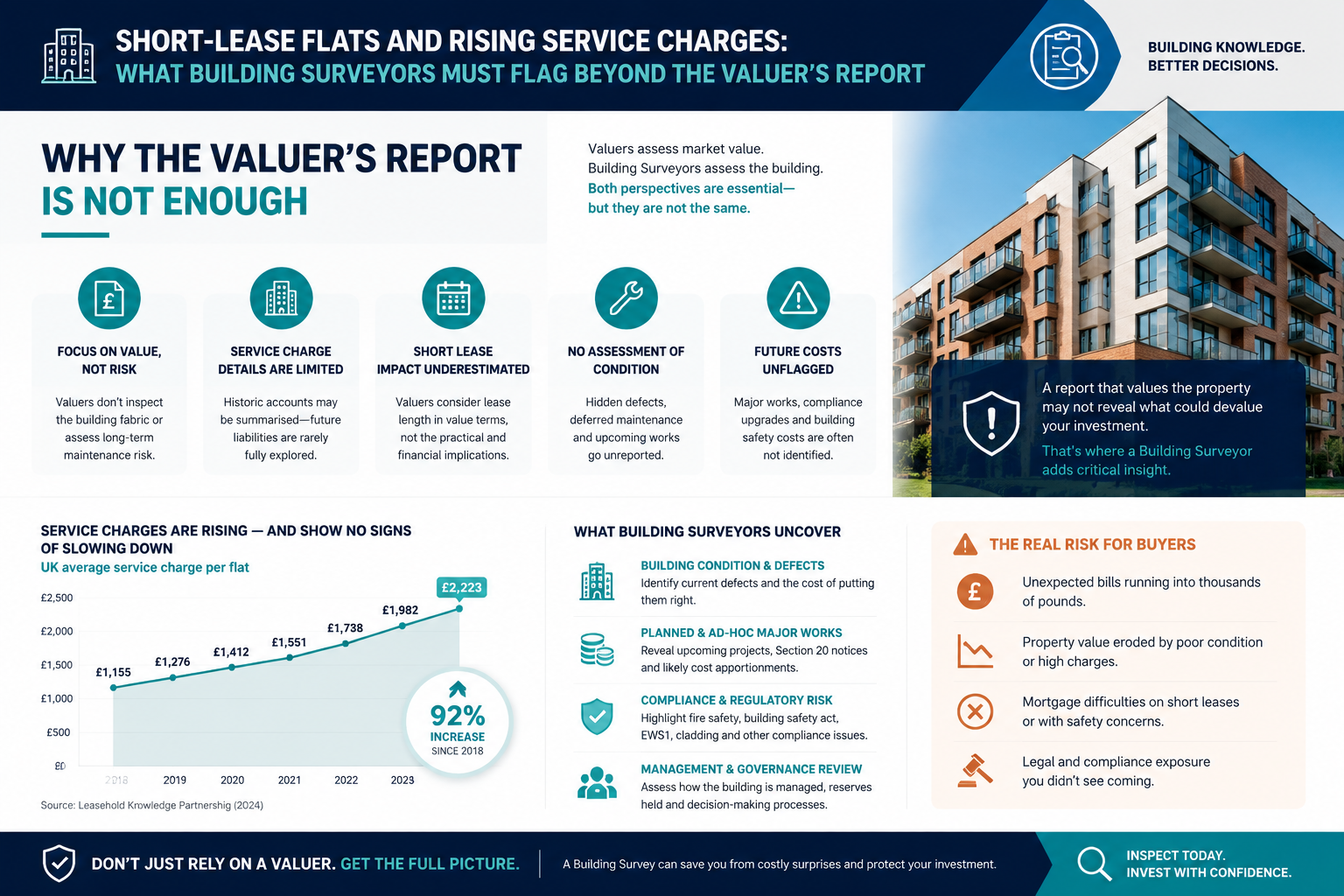

Nearly 40% of leasehold flats in England and Wales now carry service charges that exceed 1% of the property's value — a threshold that triggers lending restrictions at several major mortgage providers [3]. For buyers of short-lease flats, that single statistic reframes the entire risk picture. A valuer's report addresses price. A building surveyor's report must go further, examining the physical, financial, and legal conditions that determine whether a flat will remain mortgageable, sellable, and affordable to own over time.

The topic of Short-Lease Flats and Rising Service Charges: What Building Surveyors Must Flag Beyond the Valuer's Report sits at the intersection of structural assessment, leasehold law, and financial due diligence. Buyers and their advisers often assume the valuer has covered everything. In practice, the valuer's remit is narrower than most buyers realise, and the gaps can be costly.

Key Takeaways

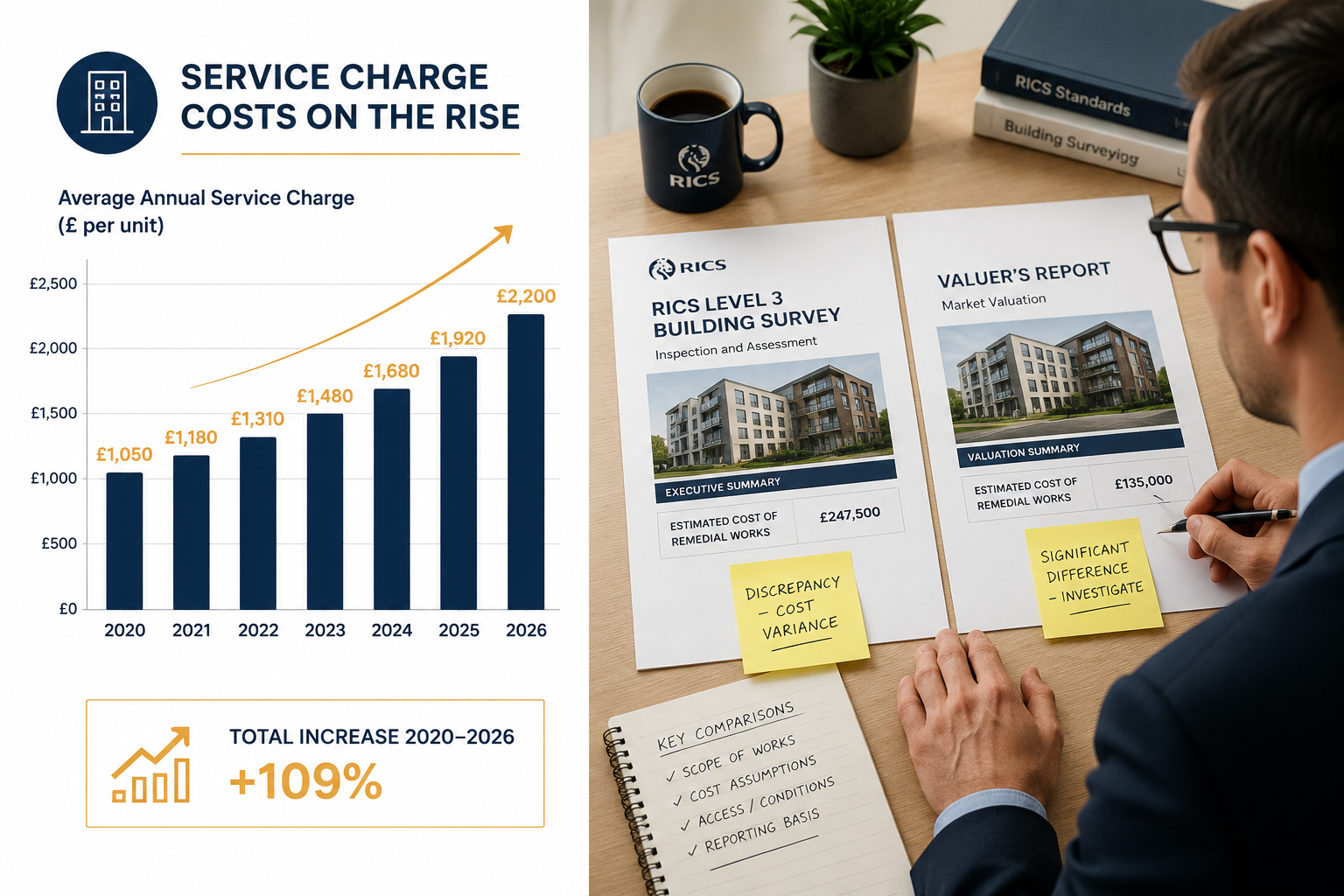

- Average service charges for leasehold flats reached £2,405 per year in 2025, a 32.6% rise over five years — surveyors must treat escalating charges as a material risk, not background noise [1].

- A short lease (typically under 80 years) compounds service charge risk because lease extension costs rise sharply below that threshold, adding financial pressure on top of rising annual charges.

- Building surveyors should request at least three years of service charge accounts, the current reserve fund balance, and any outstanding Section 20 notices before completing their report [6].

- The valuer assesses market value; the building surveyor assesses physical condition and flags financial red flags that affect long-term ownership costs — the two roles are complementary, not interchangeable.

- The Leasehold and Freehold Reform Act 2024 now requires itemised, standardised service charge accounts, giving surveyors a clearer framework for scrutiny [4].

Why the Valuer's Report Is Not Enough

A registered RICS valuer produces a report focused on one question: what is this property worth on the open market today? That assessment will factor in lease length in broad terms and may note unusually high service charges if they are obvious. However, the valuer is not typically instructed to inspect communal areas in detail, interrogate three years of management accounts, or assess the condition of the roof relative to the reserve fund balance.

This is not a criticism of valuers. It reflects the scope of their instruction. The RICS Level 3 Building Survey — often called a full structural survey — is the instrument designed to fill those gaps. For leasehold flats, particularly those with short leases or rising service charges, that survey must be approached with a specific checklist that goes well beyond damp, timber, and roof coverings.

The distinction matters because buyers routinely conflate the two reports. A flat may be valued accurately at £350,000 while simultaneously carrying a near-empty reserve fund, a Section 20 notice for £18,000 of cladding remediation, and a ground rent clause that doubles every ten years. None of those facts necessarily change the valuation figure materially on the day of purchase. All of them can devastate the buyer's finances within three years of completion.

The Short Lease Multiplier Effect

A lease with fewer than 80 years remaining is not simply a legal inconvenience. It is a financial accelerant that magnifies every other risk in the building. Below 80 years, the statutory formula for lease extension includes a "marriage value" element, which significantly increases the premium payable to the freeholder. The shorter the lease, the higher that premium — and the more urgent the extension becomes.

When rising service charges are layered on top of a short lease, the buyer faces a compounding liability. They must fund the lease extension (potentially tens of thousands of pounds), continue paying escalating annual service charges, and potentially contribute to major works through special levies — all while the property's saleability narrows because fewer lenders will offer mortgages.

A lease extension valuation should be commissioned alongside the building survey wherever the lease falls below 85 years. The building surveyor's report should explicitly note the lease length and cross-reference it with the financial documents reviewed, so the buyer understands the combined exposure.

What Building Surveyors Must Flag Beyond the Valuer's Report

Reserve Fund Health

The reserve (or sinking) fund is the building's financial safety net. A healthy fund accumulates contributions from leaseholders over time to cover major cyclical works — roof replacement, lift overhaul, external decoration, structural repairs. A low or zero balance means that when those works arise, the freeholder will issue a special levy, sometimes at very short notice [6].

Surveyors should request the most recent reserve fund statement and compare it against the building's apparent maintenance cycle. A Victorian mansion block with a £4,000 reserve fund and a roof that has not been replaced in 30 years is a warning sign that numbers alone cannot convey without physical inspection context.

Key questions to answer in the report:

- What is the current reserve fund balance per flat?

- When was the last major cyclical works programme completed?

- Is there a long-term maintenance plan (LTMP) in place?

- Does the fund balance align with the building's age and condition?

Section 20 Notices and Scheduled Major Works

Under the Landlord and Tenant Act 1985, freeholders must serve a Section 20 consultation notice before carrying out qualifying works that will cost any individual leaseholder more than £250. The notice is a legal formality, but its existence signals an imminent financial demand.

Surveyors should request confirmation of any outstanding or recently completed Section 20 notices. If a notice has been served but works have not yet started, the buyer could be liable for costs that were not factored into the purchase price. If works are recently completed but the accounts have not been reconciled, there may be a balancing charge waiting to be issued.

This is a document that neither the valuer nor the conveyancer will routinely inspect in physical detail. The building surveyor is best placed to cross-reference the notice with the observed condition of the building — asking whether the works described are visible, appropriate, and proportionate.

Service Charge Account Analysis

Average service charges reached £2,405 per year in 2025, a 4.6% increase on the previous year and a 32.6% rise over five years [1]. In London, the average climbs to £2,801 annually [2]. These are averages. Individual buildings — particularly those with cladding remediation programmes, ageing plant, or poor management — can run significantly higher.

Surveyors should request at least three years of service charge accounts and look for:

| Red Flag | What It Signals |

|---|---|

| Year-on-year increases above 10% | Poor cost control or deferred maintenance catching up |

| Large one-off charges | Emergency repairs or unplanned major works |

| Management fees above 15% of total | Potential overcharging or inefficient management |

| Incomplete or unaudited accounts | Poor governance, potential disputes |

| No breakdown of insurance costs | Possible conflicts of interest in policy placement |

The Leasehold and Freehold Reform Act 2024 now requires freeholders and managing agents to provide itemised service charge accounts in a standardised format [4]. This gives surveyors a clearer basis for comparison and challenge. Where accounts are not provided in this format, the report should note the non-compliance explicitly.

"A building surveyor who reviews three years of service charge accounts before completing a report on a leasehold flat is not doing extra work — they are doing the minimum necessary to give an honest assessment of ownership costs."

Ground Rent Escalation Clauses

Ground rent is legally separate from service charges, but its escalation terms can render a flat unmortgageable. Leases that double ground rent every ten or fifteen years can produce figures that breach lender thresholds within a single ownership period [6].

The Leasehold Reform (Ground Rent) Act 2022 capped ground rent at a peppercorn for new leases, but millions of existing leases pre-date this reform. The building surveyor should flag the ground rent terms explicitly, calculate the projected rent at five, ten, and fifteen years, and note whether those figures are likely to affect mortgage eligibility.

This is not a valuation exercise. It is a factual reporting obligation that sits clearly within the building surveyor's scope.

Management Quality Assessment

Poor management is one of the most underreported risks in leasehold flat purchases. A management company that produces incomplete accounts, responds slowly to maintenance requests, or fails to maintain adequate insurance creates a building that deteriorates faster and costs more to run [6].

Surveyors should assess management quality through observable indicators during the inspection:

- Communal area condition: Peeling paint, broken lighting, dirty carpets, and unrepaired damage all suggest reactive rather than planned maintenance.

- Plant room access and records: Lift maintenance logs, boiler service records, and fire safety certificates should be current.

- External fabric: Blocked gutters, failed pointing, and unchecked roof flashings indicate that routine maintenance cycles are not being followed.

A RICS specialist defect survey can be particularly valuable where specific elements — cladding, flat roofs, or drainage systems — require deeper investigation than a standard Level 3 survey provides.

Cladding and Fire Safety Certification

Post-Grenfell legislation has created a category of leasehold flat that is effectively unsellable without a valid EWS1 (External Wall System) certificate or equivalent fire safety assessment. Buildings over 11 metres in height with certain cladding types require this documentation before most lenders will proceed.

The building surveyor should identify the external wall construction type during inspection and flag whether an EWS1 assessment is likely to be required. Where cladding remediation is ongoing or planned, the surveyor should note the implications for service charges, as remediation costs — even where government funding is available — frequently generate additional management and legal costs that fall on leaseholders.

The 1% Lending Threshold

Approximately 37% of flats in England and Wales now have service charges exceeding 1% of their property value, up from 29% in 2020 [3]. Several lenders have introduced criteria that restrict or decline mortgage applications where charges cross this threshold. In London, where property values are higher relative to service charges, the proportion is lower — but the trajectory is upward.

The building surveyor's report should calculate the current service charge as a percentage of the agreed purchase price and note whether it approaches or exceeds 1%. Where it does, the report should recommend that the buyer's mortgage broker checks lender criteria before proceeding. This is not a valuation opinion — it is a practical flag that protects the buyer from a failed mortgage application at a late stage.

Complementing, Not Duplicating, the Valuer's Work

The relationship between the building surveyor and the valuer should be collaborative, not competitive. The valuer determines what the market will pay for the property today. The building surveyor determines what the buyer will pay to own it over the next five to ten years.

In practice, this means:

- The building surveyor reviews physical condition and flags financial documents that affect ownership costs.

- The valuer uses market comparables and lease adjustments to arrive at a figure.

- Neither report duplicates the other's core function.

Where both reports are commissioned — which is strongly advisable for any short-lease flat — the buyer should read them together. A registered RICS valuer and a building surveyor working from the same set of documents will produce complementary outputs that give a far more complete picture than either report alone.

The Greater London Authority launched a formal review in May 2026 into the impact of rising service charges on housing affordability across the capital [5]. That investigation reflects a growing recognition that service charge escalation is not a marginal issue — it is a structural feature of the leasehold market that requires systematic scrutiny at the point of purchase.

Practical Document Checklist for Surveyors

Before completing a report on a short-lease leasehold flat, the building surveyor should have reviewed or formally requested the following:

- Three years of service charge accounts (audited where possible)

- Current reserve fund statement

- Long-term maintenance plan (if available)

- Any outstanding or recently served Section 20 notices

- Ground rent schedule for the full lease term

- EWS1 certificate or fire risk assessment (for buildings over 11 metres)

- Building insurance schedule and reinstatement value

- Most recent managing agent's report or AGM minutes

Where any of these documents are unavailable, the report should state this prominently and note that the uncertainty represents a material risk that the buyer should resolve before exchange of contracts [6].

For buyers in specific regions, working with local chartered surveyors who understand the management landscape in their area — including the reputations of specific freeholders and managing agents — adds an additional layer of practical intelligence that no document review can fully replicate.

Legislative Context in 2026

The Leasehold and Freehold Reform Act 2024 introduced several provisions that directly affect how surveyors and buyers should approach service charge scrutiny. Standardised, itemised accounts are now a legal requirement [4]. Ground rent reform has been extended. Leaseholders have enhanced rights to challenge unreasonable charges through the First-tier Tribunal.

These reforms improve transparency but do not eliminate risk. A standardised account format makes comparison easier; it does not guarantee that the figures within it are reasonable or that the reserve fund is adequate. The building surveyor's role remains essential precisely because legislation sets a floor, not a ceiling, for due diligence.

Buyers seeking detailed guidance on the factors that affect property valuation in the context of leasehold tenure will find that service charges, lease length, and reserve fund health are increasingly weighted variables — not footnotes.

Conclusion

Short-lease flats and rising service charges represent one of the most complex risk environments in the residential property market in 2026. The building surveyor's report is the instrument best suited to navigating that complexity — but only if it is scoped and executed to go beyond the physical fabric of the flat itself.

Actionable next steps for buyers and their advisers:

- Commission a RICS Level 3 Building Survey for any leasehold flat, particularly where the lease is below 85 years.

- Instruct the surveyor explicitly to review service charge accounts, reserve fund statements, and Section 20 notices as part of the scope.

- Commission a separate lease extension valuation where the lease is below 85 years, so the full financial exposure is understood before exchange.

- Ask the mortgage broker to check lender criteria against the current service charge level before proceeding.

- Treat missing or incomplete financial documents as a material red flag — not an administrative inconvenience.

- Read the building survey and the valuer's report together, treating them as complementary inputs rather than alternatives.

The valuer tells a buyer what a flat is worth. The building surveyor tells them what it will cost to own. Both answers are essential. Neither is sufficient without the other.

References

[1] 2025 Service Charge Index – https://www.hamptons.co.uk/articles/2025-service-charge-index?utm_source=openai

[2] Soaring Service Charges On Leasehold Flats Hit Capital Values – https://www.newsontheblock.com/news-opinion-service-charges/soaring-service-charges-on-leasehold-flats-hit-capital-values?utm_source=openai

[3] Nearly 40 Of Flats Face Lending Curbs As Service Charges Rise Hamptons Finds – https://www.mortgagesolutions.co.uk/news/2026/03/02/nearly-40-of-flats-face-lending-curbs-as-service-charges-rise-hamptons-finds/?utm_source=openai

[4] Ground Rent Service Charge Changes 2026 – https://sell-short-lease-flat.co.uk/news/ground-rent-service-charge-changes-2026/?utm_source=openai

[5] City Hall London Service Charges Probe May 2026 – https://sell-short-lease-flat.co.uk/news/city-hall-london-service-charges-probe-may-2026/?utm_source=openai

[6] Valuing Properties With Short Leases And Service Charge Uncertainty A Practical Guide For Surveyors And Flat Owners – https://manchestersurveyors.com/valuing-properties-with-short-leases-and-service-charge-uncertainty-a-practical-guide-for-surveyors-and-flat-owners/?utm_source=openai

[7] Building Surveying For Pre Purchase Flats Leasehold Risks Service Charge Clues And Hidden Defects Buyers Miss – https://www.canterburysurveyors.com/blog/building-surveying-for-pre-purchase-flats-leasehold-risks-service-charge-clues-and-hidden-defects-buyers-miss/?utm_source=openai