As of May 1, 2026, Section 21 "no-fault evictions" are legally abolished — a seismic shift that makes the Renters' Rights Act 2026 impact on buy-to-let valuations one of the most pressing challenges facing chartered surveyors today. [1][2]

The private rented sector has operated under the shadow of this legislation for years, but now that implementation is live, surveyors must rapidly adapt their valuation methodologies. Rental yields, capital values, and lender risk models are all in flux. For any professional involved in property valuation, understanding how these regulatory changes translate into hard numbers is no longer optional — it is essential.

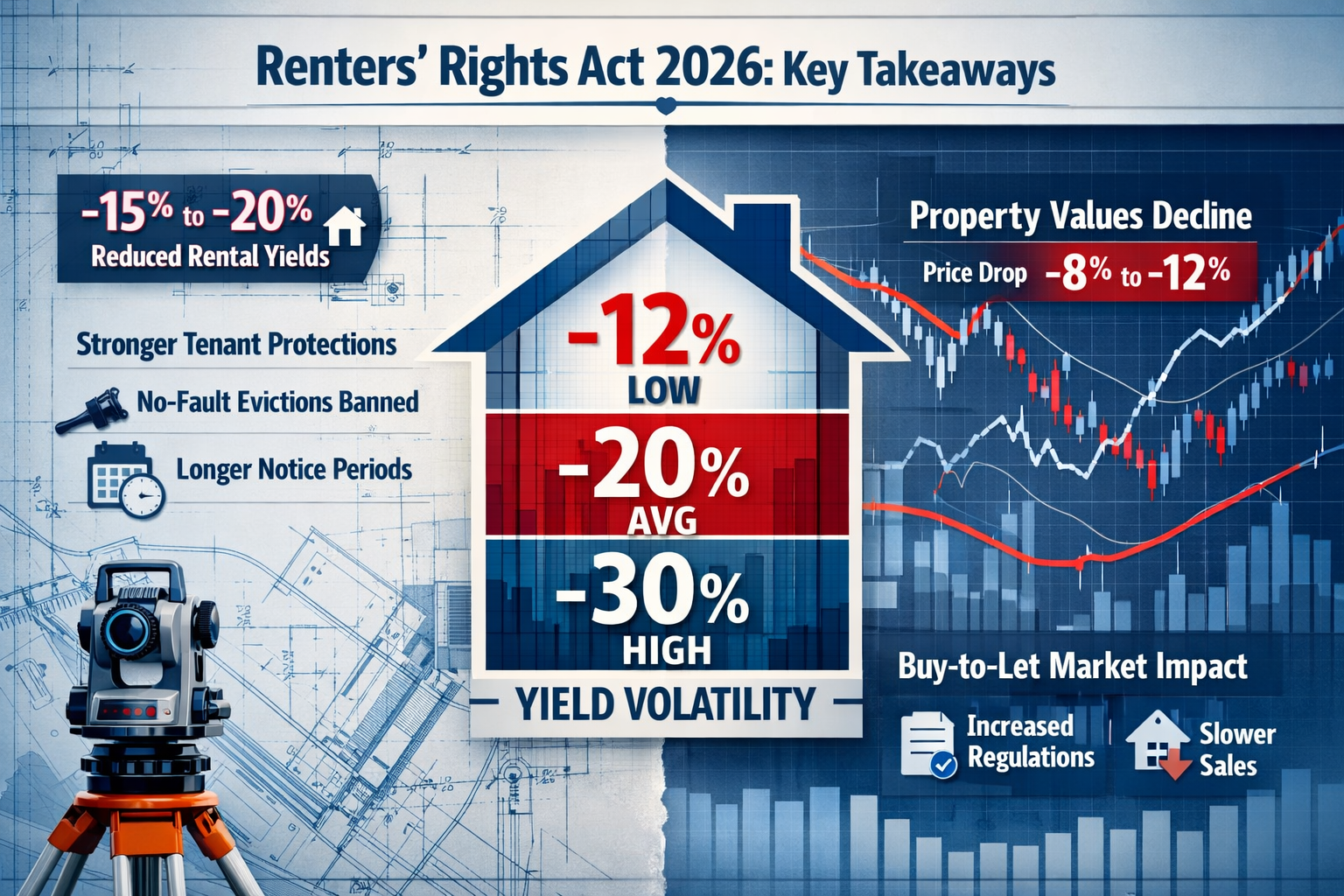

Key Takeaways 📌

- Section 21 is abolished from May 2026, replacing no-fault evictions with a more complex Section 8 grounds-based process.

- Yield volatility is increasing as lenders reassess cashflow visibility and void period assumptions across buy-to-let portfolios.

- Surveyors must update their valuation models to account for longer possession timelines, restricted rent review mechanisms, and mandatory landlord registration.

- Lenders are adjusting risk pricing, with many reviewing cost and void assumptions that were previously updated only annually. [1]

- Expert witness surveyors face new challenges in landlord-tenant disputes where Section 8 grounds are contested.

What the Renters' Rights Act 2026 Actually Changes

The End of Section 21: A Legal Landmark

Before May 2026, a landlord could serve a Section 21 notice to recover possession of a property without providing any reason. This gave buy-to-let investors a powerful tool for managing their portfolios — whether to sell, refurbish, or simply change tenants.

That flexibility is now gone. [2]

Under the Renters' Rights Act 2026, all tenancies in England become periodic (open-ended) by default. Fixed-term assured shorthold tenancies no longer exist for new lets. Landlords who wish to regain possession must now rely exclusively on Section 8 grounds, which require specific, evidenced reasons. [2]

💬 "The abolition of Section 21 is not merely a procedural change — it fundamentally alters the risk profile of every buy-to-let property in England."

Section 8: The New Possession Framework

The Section 8 replacement framework includes several key grounds relevant to landlords:

| Ground | Reason | Notice Period |

|---|---|---|

| Ground 1A | Landlord intends to sell | 4 months |

| Ground 6A | Redevelopment | 4 months |

| Ground 8 | Serious rent arrears (2+ months) | 4 weeks |

| Ground 14 | Anti-social behaviour | Immediate |

| Ground 1 | Landlord/family to move in | 4 months |

Each ground requires documentary evidence, and courts are expected to scrutinise applications more closely than under the old regime. [2] This increases both the time and cost of achieving vacant possession — a critical factor in any investment valuation.

Landlord Registration and Compliance Costs

The Act also introduces a mandatory landlord registration scheme in England. This creates additional compliance obligations and cost layers that surveyors must factor into net yield calculations. Non-compliance carries financial penalties that further erode returns.

Renters' Rights Act 2026 Impact on Buy-to-Let Valuations: Understanding Yield Volatility

Why Yields Are Under Pressure

The Renters' Rights Act 2026 impact on buy-to-let valuations flows primarily through three yield compression channels:

- Extended void periods — longer possession timelines mean properties may sit empty for months longer than previously modelled.

- Restricted rent review mechanisms — the Act limits how and when landlords can increase rents, reducing income growth assumptions.

- Increased management costs — legal fees, compliance costs, and potential tribunal proceedings all reduce net operating income.

Lenders are already responding. Many buy-to-let mortgage providers are facing increased uncertainty around landlord cashflows due to the shift to open-ended tenancies. [1] Where rental income visibility was once relatively predictable, it is now subject to far greater regulatory risk.

The Lender Risk Recalibration Problem

A significant operational challenge has emerged: many lenders currently review their cost and void assumptions only once a year. [1] In a rapidly changing regulatory environment, this creates dangerous gaps between actual risk and modelled risk.

The consequences are material:

- Longer possession timelines increase loss expectations for lenders. [1]

- Provisioning requirements are likely to rise across buy-to-let mortgage books.

- Collections strategies must be redesigned to account for slower and more complex eviction processes. [1]

For surveyors preparing Red Book valuations for lender clients, this means that comparable evidence alone is insufficient. The valuation must now explicitly address regulatory risk as a distinct value-affecting factor.

Quantifying Yield Volatility: A Surveyor's Framework

Surveyors assessing buy-to-let properties in 2026 should consider the following yield adjustment framework:

Gross-to-Net Yield Deductions (Post-Act Estimates):

| Cost Category | Pre-Act Estimate | Post-Act Estimate |

|---|---|---|

| Void periods | 4–6 weeks/year | 8–14 weeks/year |

| Legal/possession costs | £500–£1,500 | £3,000–£8,000+ |

| Management uplift | 10–12% gross | 12–15% gross |

| Compliance costs | Minimal | £300–£800/year |

⚠️ These estimates are indicative. Actual figures will vary by property type, location, and tenant profile. Surveyors should build location-specific evidence bases.

For properties in high-demand urban areas — such as those assessed by chartered surveyors in Islington or chartered surveyors in Fulham — yield compression may be partially offset by stronger rental demand. In lower-demand markets, the impact on capital values could be more pronounced.

Capital Value Implications

Yield compression directly affects capital values through the investment method of valuation:

Capital Value = Net Annual Rent ÷ Capitalisation Rate

If net annual rent falls (due to higher voids and costs) and the capitalisation rate rises (due to increased risk), capital values face double compression. A property yielding £15,000 net at a 5% cap rate = £300,000. If net income falls to £13,000 and the cap rate rises to 5.5%, capital value drops to approximately £236,000 — a 21% reduction.

This is not hypothetical. Surveyors preparing property valuations must stress-test their assumptions against these scenarios.

Surveyor Strategies for Navigating the Post-Section 21 Landscape

Adapting Valuation Methodology

The Renters' Rights Act 2026 impact on buy-to-let valuations demands a fundamental rethink of standard surveyor methodology. The following strategies are recommended for RICS-registered professionals:

1. Adopt a Regulatory Risk Premium

Add an explicit regulatory risk premium to the capitalisation rate used in investment valuations. This should reflect:

- Jurisdiction-specific possession timeline data

- Local court backlog statistics

- Property-specific tenant risk profile

2. Rebuild Void Period Assumptions

Historical void period data (typically 3–5%) is no longer reliable. Surveyors should:

- Source post-Act possession timeline data from court statistics

- Apply location-weighted void multipliers

- Model best-case, base-case, and worst-case scenarios

3. Reassess Comparable Evidence

Pre-2026 investment sales may not provide reliable comparables for post-Act valuations. Surveyors should:

- Flag the legislative change date in valuation reports

- Seek post-May 2026 transaction evidence where available

- Apply temporal adjustments to pre-Act comparables

4. Engage with Lender Requirements Proactively

Lenders are redesigning their buy-to-let risk models. [1] Surveyors who understand these changes can provide more lender-relevant reports. This is particularly important for commercial valuation instructions involving larger portfolios.

Expert Witness Considerations

The abolition of Section 21 will generate a significant increase in contested possession proceedings. Surveyors acting as expert witnesses in landlord-tenant disputes must be prepared to:

- Provide evidence on market rent levels to assess whether a landlord's rent increase notice is reasonable

- Assess property condition as it relates to habitability grounds

- Opine on comparable rental evidence in rent tribunal hearings

A thorough RICS building survey or specialist defect survey can provide critical documentary evidence in disputes where property condition is contested.

The Rent Review Challenge

The Act's restrictions on rent increases — limiting landlords to one increase per year and requiring market-evidence justification — make professional rent review expertise more valuable than ever. Surveyors who can robustly evidence market rent levels will be in high demand from both landlords seeking to justify increases and tenants challenging them.

Portfolio-Level Assessment

For investors holding multiple buy-to-let properties, surveyors should offer portfolio-level stress testing that considers:

- 🏠 Geographic concentration risk — high exposure to one local market increases regulatory risk

- 📋 Tenancy profile analysis — proportion of high-risk tenancies (arrears history, ASB flags)

- 💰 Financing structure — interest coverage ratios under stressed net income scenarios

- 🔄 Exit strategy viability — Ground 1A (sale) timeline implications for portfolio liquidity

Practical Steps for Surveyors in 2026

Here is a concise action checklist for surveyors updating their buy-to-let valuation practice:

- ✅ Update valuation report templates to include a Regulatory Risk section

- ✅ Build a local database of post-Act void period data as it becomes available

- ✅ Review all standing instructions with lender clients to confirm new risk model requirements [1]

- ✅ Develop a standard Section 8 grounds impact note for investment valuations

- ✅ Ensure CPD includes training on the Renters' Rights Act 2026 provisions

- ✅ Consider specialist training in rent tribunal expert witness work

- ✅ Collaborate with legal professionals to understand evolving case law on Section 8 grounds

Regional Market Dynamics: Where the Impact Hits Hardest

The Renters' Rights Act 2026 impact on buy-to-let valuations will not be uniform across England. Regional dynamics matter enormously.

High-pressure rental markets (London, South East, major university cities) may see limited capital value decline because strong tenant demand partially offsets yield compression. However, legal costs and possession timelines will still increase regardless of location.

Lower-demand markets (parts of the North East, coastal towns, rural areas) face a more challenging outlook. Where yields were already thin and tenant demand more variable, the additional cost burden may push marginal landlords to exit — potentially flooding local markets with former rental stock.

Surveyors operating across diverse geographies — from chartered surveyors in Surrey to chartered surveyors in Essex — will need to develop location-specific adjustment matrices rather than applying blanket national assumptions.

The Accidental Landlord Problem

A significant subset of the buy-to-let market consists of accidental landlords — those who inherited property, relocated, or retained a former home. These landlords typically have lower risk tolerance and less professional management infrastructure.

For this group, the Act's complexity may accelerate market exit decisions. Surveyors advising on property valuations for sale purposes should be prepared to model both vacant possession value and investment value with sitting tenant — and explain the growing gap between the two.

Conclusion: Actionable Next Steps for Surveyors

The Renters' Rights Act 2026 impact on buy-to-let valuations is not a future risk to monitor — it is a present reality to manage. From the abolition of Section 21 to the introduction of mandatory landlord registration, every element of the Act reshapes how rental property should be assessed, valued, and reported.

Surveyors who adapt quickly will become indispensable advisors to landlords, lenders, and investors navigating this new landscape. Those who continue applying pre-2026 methodologies risk producing valuations that materially misrepresent risk.

Immediate Action Steps 🎯

- Audit your valuation templates — ensure they capture regulatory risk as a distinct factor.

- Engage your lender clients now — understand how their risk models are evolving and align your reporting accordingly. [1]

- Build your Section 8 knowledge — the grounds, timelines, and evidence requirements are now central to investment valuation. [2]

- Develop post-Act comparable databases — pre-May 2026 evidence needs careful temporal adjustment.

- Consider expert witness training — contested possession proceedings will increase, creating demand for qualified surveyor experts.

- Communicate proactively with landlord clients — many are unaware of the full valuation implications of the Act's provisions.

The private rented sector is entering a period of sustained regulatory transformation. Chartered surveyors who combine technical valuation expertise with deep legislative understanding will be best placed to serve their clients — and to protect the integrity of the valuations they produce.

References

[1] Renters Rights Act To Reshape Buy To Let Risk Models – https://mortgagesoup.co.uk/renters-rights-act-to-reshape-buy-to-let-risk-models/

[2] Selling A Rental Property In 2026 How The New Renters Rights Bill Affects You – https://www.gorvinsresidential.com/selling-a-rental-property-in-2026-how-the-new-renters-rights-bill-affects-you/

[3] Watch – https://www.youtube.com/watch?v=N4zC65cu8GU