{"cover":"Professional landscape format (1536×1024) hero image with bold text overlay: 'Valuation Methodology Shifts: Buyer Weakness vs Long-Term Optimism' in extra large 72pt white sans-serif font with dark shadow and semi-transparent navy overlay box, positioned in upper third center. Background shows split-screen composition: left side displays declining bar chart with red downward arrows representing -26% buyer enquiries, right side shows upward trending green line graph representing +33% 12-month expectations. RICS logo subtly integrated. Foreground includes professional surveyor reviewing property valuation documents on tablet with data visualization overlays. Color palette: navy blue, white, red, green accents. High contrast, editorial magazine cover quality, financial data visualization aesthetic","content":["Detailed landscape format (1536×1024) image showing professional chartered surveyor in modern office analyzing dual-screen computer setup displaying RICS February 2026 data dashboard. Left monitor shows heat map of UK regions with color-coded price sentiment (London in deep red -40%, Northern regions in amber showing positive trends). Right monitor displays comparative line graphs tracking buyer enquiry decline from -15% to -26% against stable 12-month sentiment at +33%. Desk includes Red Book valuation manual, property reports, calculator. Background shows large wall-mounted regional divergence map with data points. Professional lighting, business editorial style, data-driven composition","Detailed landscape format (1536×1024) image depicting comparative valuation methodology framework as infographic poster on conference room wall. Visual shows three-column comparison chart: 'Traditional Approach' (left column with single-metric focus), 'Hybrid Methodology' (center column highlighted with dual-weighting system showing short-term vs long-term factors), 'Forward-Looking Framework' (right column with predictive analytics icons). Each column contains percentage allocations, weighting scales, and decision tree flowcharts. Foreground shows professional valuation team reviewing commercial property assessment documents. Color-coded risk indicators, professional business aesthetic, strategic planning environment","Detailed landscape format (1536×1024) image showing close-up of professional property valuation report being completed on desk with RICS standards documentation visible. Report displays dual-scenario analysis sections: 'Current Market Conditions Assessment' with -12% agreed sales data and regional price variance tables, and 'Medium-Term Value Projection' section with +33% sentiment indicators and rental market resilience data at +20%. Hands holding red pen marking adjustments. Background includes laptop showing rental demand stability charts, calculator, property photographs, comparable sales data spreadsheets. Natural office lighting, professional documentation aesthetic, detailed analytical composition"]"}

The RICS February 2026 survey has exposed a striking market paradox: buyer enquiries plummeted to -26% net balance while 12-month price expectations held firm at +33%[3]. This disconnect between immediate market weakness and sustained medium-term optimism presents chartered surveyors with an unprecedented challenge—how to accurately value properties when current transaction data tells one story and forward-looking sentiment tells another entirely different narrative.

Understanding Valuation Methodology Shifts: Adjusting Assessments When Buyer Enquiries Weaken but Long-Term Sentiment Strengthens (RICS February 2026 Data) has become essential for property professionals navigating this complex environment. Traditional valuation approaches that rely heavily on recent comparable sales data may no longer provide the complete picture when market fundamentals diverge so dramatically from transactional activity.

Key Takeaways

- 🔻 Buyer enquiries fell sharply to -26% in February 2026, representing a significant decline from -15% in January, while 12-month price expectations remained positive at +33%

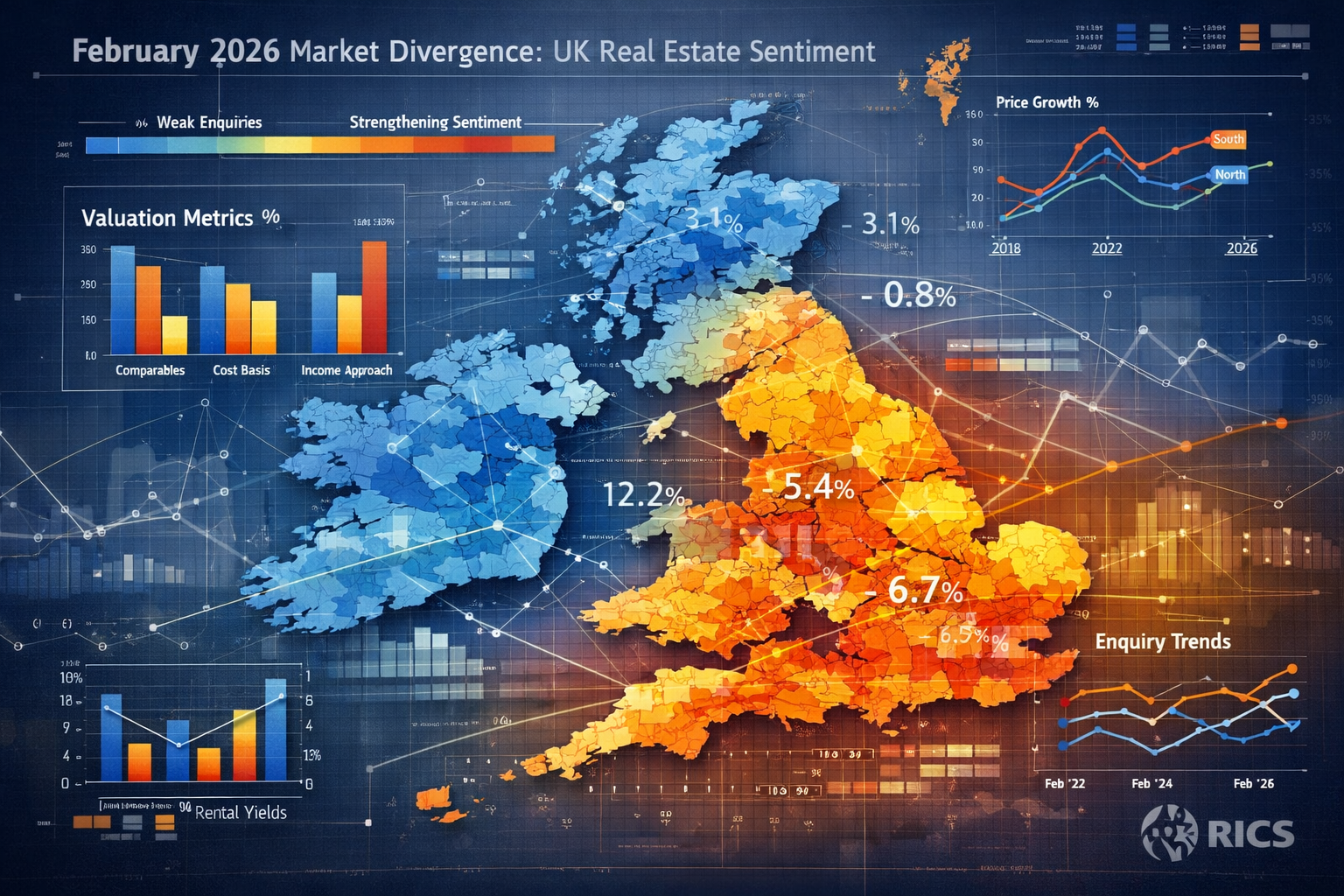

- 🗺️ Regional divergence has intensified, with London experiencing -40% net balance compared to firmer trends in Northern Ireland, Scotland, and North West England

- 📊 Near-term price expectations deteriorated to -18%, down from -6% in January, creating a valuation timing challenge for surveyors

- 🏠 Rental market resilience continues, with +20% of participants expecting rent increases despite buyer market weakness

- ⚖️ Hybrid valuation methodologies that balance current transaction data with forward-looking sentiment indicators are becoming essential for accurate property assessments

Understanding the February 2026 Market Divergence

The February 2026 RICS data reveals a market caught between conflicting forces. Buyer demand declined sharply to -26% net balance, down from -15% in January, representing fresh weakness after tentative early-year improvement[3]. This decline was driven by renewed geopolitical uncertainty and macroeconomic concerns that dampened immediate purchasing confidence.

Yet despite this transactional weakness, surveyors maintained relatively positive 12-month price expectations at +33% nationally[3]. This suggests that property professionals view current buyer hesitancy as temporary rather than structural—a critical distinction when determining property values.

The Transaction Reality

Agreed sales remained subdued at -12% net balance in February, confirming that the buyer enquiry weakness is translating into reduced transaction volumes[3]. Near-term sales expectations softened to -2%, reflecting surveyor caution about immediate market momentum[3].

House prices remained broadly flat nationally at -12% net balance in February 2026, only slightly weaker than January's -10%[3]. This price stability despite buyer weakness indicates that sellers are holding firm on valuations, supported by limited stock availability and the belief that market conditions will improve.

For professionals conducting Red Book valuations, this creates a methodological challenge: should valuations reflect the current weak transaction environment or incorporate the more optimistic medium-term outlook that underpins seller pricing expectations?

Regional Variation Complicates National Trends

The national figures mask significant regional divergence. London experienced the most severe buyer weakness at -40% net balance, with the South East at -24% and East Anglia at -26%[3]. Meanwhile, Northern Ireland, Scotland, and North West England reported firmer price trends[3].

This regional variation is particularly pronounced in longer-term expectations. London's 12-month price expectations cooled dramatically to +7% from +56%[4], representing one of the most significant sentiment shifts in the capital in recent years. This suggests that even forward-looking optimism is geographically uneven.

When conducting commercial valuations or residential assessments, understanding these valuation factors at a granular regional level has become essential for accuracy.

Valuation Methodology Shifts: Adjusting Assessments When Buyer Enquiries Weaken but Long-Term Sentiment Strengthens

Traditional valuation approaches typically weight recent comparable sales heavily, using transaction evidence as the primary basis for determining market value. However, when transaction volumes decline and buyer enquiries weaken while professional sentiment about future values remains positive, this approach may undervalue properties relative to their likely medium-term worth.

The Case for Dual-Weighting Systems

Forward-thinking surveyors are adopting dual-weighting valuation frameworks that explicitly account for both current market conditions and medium-term expectations. This approach recognizes that market value represents not just today's transaction environment but also the informed expectations of market participants about future conditions.

Key components of this adjusted methodology include:

- Transaction evidence weighting: Maintaining comparable sales analysis but acknowledging the limited volume and potentially distressed nature of current transactions

- Sentiment adjustment factors: Incorporating surveyor expectations data from RICS surveys as a forward-looking indicator

- Regional differentiation: Applying different weighting ratios based on local market dynamics rather than national averages

- Time-horizon specification: Clearly stating whether the valuation reflects current exchange value or anticipated value over a specified period

This approach aligns with evolving RICS guidance that emphasizes the importance of context and assumption transparency in valuation reporting[2].

Incorporating Rental Market Strength

One of the most significant supporting factors for medium-term optimism is rental market resilience. Tenant demand remained stable at +2% net balance over the three months to February, while landlord instructions sat firmly at -27% net balance[3]. This supply-demand imbalance continues to support rental values, with +20% of survey participants expecting rents to rise over the coming three months[3].

For valuation purposes, this rental strength provides important context. Properties with strong rental potential may warrant less downward adjustment for weak buyer enquiries, as their income-generating capacity remains robust. This is particularly relevant for Help to Buy valuations and investment property assessments.

Near-Term vs Medium-Term Expectations

The divergence between near-term and medium-term expectations creates a valuation timing challenge. Near-term price expectations deteriorated significantly to -18% in February, down from -6% in January[3]. Yet 12-month expectations remained at +33% nationally[3].

This suggests a J-curve trajectory—further near-term weakness followed by medium-term recovery. For surveyors, this raises the question: which timeframe should dominate valuation conclusions?

The answer depends on the valuation purpose:

| Valuation Purpose | Appropriate Time Horizon | Weighting Approach |

|---|---|---|

| Immediate sale/purchase | Near-term (3 months) | Heavy weight on current transactions |

| Mortgage lending | Medium-term (6-12 months) | Balanced approach with sentiment factors |

| Portfolio/accounting | Longer-term | Greater weight on fundamental value drivers |

| Probate/tax | Statutory date-specific | Current market only, with commentary |

Understanding these distinctions ensures that valuation factors are appropriately applied based on the assessment's intended use.

Regional Strategies for Valuation Methodology Shifts

The pronounced regional divergence in the February 2026 data demands location-specific valuation approaches. A one-size-fits-all methodology will produce inaccurate results when London shows -40% buyer sentiment while northern regions demonstrate resilience[1].

London and South East: Conservative Adjustments

In London, where buyer enquiries reached -40% and 12-month expectations cooled to just +7%[4], surveyors should adopt more conservative valuation adjustments. The dramatic sentiment shift suggests that even medium-term optimism has weakened significantly in the capital.

Recommended approaches for London valuations include:

- Increased weighting on recent transaction evidence (70-75% vs typical 60-65%)

- Conservative comparable selection, favoring recent sales over older data

- Explicit downward adjustments for properties in submarkets showing particular weakness

- Enhanced market conditions commentary explaining the sentiment shift

The South East, with -24% buyer sentiment, requires similar but slightly less conservative treatment[3]. Properties with strong commuter links or lifestyle appeal may warrant less aggressive downward adjustment than purely London-focused assets.

Northern Regions: Maintaining Value Confidence

Northern Ireland, Scotland, and North West England showed firmer price trends in February[3], suggesting that national weakness is not uniform. In these regions, surveyors can maintain greater confidence in medium-term expectations when determining current values.

Appropriate adjustments include:

- Standard transaction weighting (60-65%) with normal sentiment incorporation

- Positive adjustment factors for properties in high-demand submarkets

- Recognition of supply constraints that support pricing power

- Commentary highlighting regional outperformance relative to national trends

For professionals conducting homebuyer surveys in these regions, the valuation component can reflect greater stability than might be assumed from national headlines.

East Anglia and Regional Centers: Balanced Approach

Regions showing moderate weakness (East Anglia at -26%)[3] require balanced valuation methodologies that acknowledge current softness while recognizing that medium-term fundamentals remain reasonably supportive.

This middle-ground approach involves:

- Equal weighting between current transactions and forward indicators (50-50 split)

- Property-specific adjustments based on individual characteristics and appeal

- Submarket analysis to identify pockets of strength within broader regional weakness

- Transparent assumption documentation explaining the balanced methodology

Practical Implementation for Surveyors

Implementing Valuation Methodology Shifts: Adjusting Assessments When Buyer Enquiries Weaken but Long-Term Sentiment Strengthens (RICS February 2026 Data) requires systematic changes to valuation processes and reporting.

Enhanced Comparable Analysis

Traditional comparable analysis focuses primarily on recent sales prices. Enhanced methodology requires additional layers:

- Transaction context assessment: Understanding whether comparables sold under distressed conditions, with incentives, or represented motivated transactions

- Time-on-market analysis: Longer marketing periods indicate weaker demand and may require downward adjustment

- Vendor motivation evaluation: Sales by motivated vendors may not reflect true market value in a weak transaction environment

- Withdrawn listings review: Properties that failed to sell provide important ceiling price information

This deeper analysis ensures that comparable evidence is properly contextualized within the current market weakness.

Sentiment Integration Framework

Incorporating RICS survey data and broader market sentiment requires a structured approach:

- Quarterly sentiment review: Systematically reviewing RICS regional data to inform adjustment factors

- Peer consultation: Discussing market conditions with fellow surveyors to validate sentiment assessments

- Client expectation management: Explaining to clients how sentiment factors influence valuations

- Documentation standards: Recording sentiment data sources and weighting decisions in valuation files

For commercial property surveyors, this framework is particularly important given the longer transaction cycles and greater impact of sentiment on commercial values.

Reporting Transparency

Clear communication of methodology is essential when valuations incorporate both weak current data and stronger forward expectations. Enhanced reporting should include:

- Explicit methodology statement: Describing the weighting approach between current transactions and forward indicators

- Assumption transparency: Clearly stating assumptions about market recovery timing and magnitude

- Sensitivity analysis: Showing how values would change under different scenarios

- Market conditions commentary: Providing context from RICS data and other market intelligence

This transparency protects surveyors professionally while ensuring clients understand the basis for valuation conclusions.

Risk Management Considerations

Adopting adjusted methodologies introduces additional professional risk that must be managed:

✅ Documentation excellence: Maintain comprehensive files justifying methodology choices

✅ Professional indemnity awareness: Ensure PI insurance covers evolving valuation approaches

✅ Peer review processes: Implement internal quality control for complex valuations

✅ Client instruction clarity: Obtain clear written instructions about valuation basis and purpose

✅ Regular methodology review: Update approaches as market conditions evolve

For surveyors providing RICS building surveys at Level 3, the valuation component requires particular care given the comprehensive nature of these assessments.

The Rental Market Factor in Valuation Adjustments

The resilience of the rental market provides crucial support for property valuations even as buyer enquiries weaken. With +20% of participants expecting rent increases[3] and landlord instructions remaining severely constrained at -27%[3], rental values continue to strengthen.

Income Capitalization Adjustments

For investment properties, rental strength justifies maintaining firmer valuations despite buyer market weakness. The income capitalization approach becomes relatively more important when transaction evidence is limited or potentially distressed.

Key adjustments include:

- Yield compression recognition: Strong rental demand may justify tighter yields despite buyer weakness

- Rental growth incorporation: Forward rental expectations should inform capitalization rates

- Void period adjustments: Reduced void expectations in tight rental markets increase income certainty

- Tenant quality premium: High-quality tenant demand supports premium valuations

This approach is particularly relevant for rent review professionals who must balance current rental evidence with market trajectory.

Owner-Occupier Implications

Even for owner-occupier properties, rental market strength provides valuation support through:

- Alternative use value: Strong rental potential establishes a value floor

- Investor buyer potential: Properties attractive to investors maintain demand even when owner-occupier enquiries weaken

- Opportunity cost consideration: Buyers comparing purchase to rental costs may find purchase relatively attractive despite market weakness

Surveyors should explicitly consider rental market dynamics when valuing all residential properties, not just obvious investment assets.

Looking Forward: Methodology Evolution

The divergence between current weakness and medium-term optimism revealed in the Valuation Methodology Shifts: Adjusting Assessments When Buyer Enquiries Weaken but Long-Term Sentiment Strengthens (RICS February 2026 Data) is unlikely to be a temporary phenomenon. Market volatility, geopolitical uncertainty, and economic transitions suggest that such divergences may become more common.

Developing Adaptive Frameworks

Surveyors should develop adaptive valuation frameworks that can respond to varying market conditions without requiring complete methodology overhauls. This includes:

- Scenario-based valuation models that can quickly adjust weighting factors

- Real-time market data integration using technology to track sentiment shifts

- Automated comparable analysis tools that can rapidly assess transaction context

- Client communication templates that efficiently explain methodology variations

Technology will play an increasingly important role in enabling these adaptive approaches while maintaining professional standards.

Professional Development Priorities

The profession must prioritize training in:

- Statistical analysis of market sentiment data

- Forecasting methodologies that incorporate multiple data sources

- Risk assessment frameworks for valuation uncertainty

- Client communication skills for explaining complex methodologies

RICS and other professional bodies should develop specific guidance on incorporating sentiment data and forward expectations into valuation methodologies while maintaining compliance with international valuation standards[2].

Regulatory and Standards Evolution

Valuation standards may need to evolve to provide clearer guidance on:

- Acceptable weighting approaches for current vs forward-looking data

- Documentation requirements for sentiment-adjusted valuations

- Disclosure standards for methodology variations

- Peer review protocols for complex valuation scenarios

This evolution will help protect both surveyors and clients while ensuring valuation quality remains high during periods of market divergence.

Conclusion

The Valuation Methodology Shifts: Adjusting Assessments When Buyer Enquiries Weaken but Long-Term Sentiment Strengthens (RICS February 2026 Data) represents more than a temporary market anomaly—it signals a fundamental challenge for property valuation in an era of increased market volatility and uncertainty.

The sharp decline in buyer enquiries to -26% alongside sustained 12-month expectations at +33% creates a valuation paradox that traditional comparable-sales-focused methodologies struggle to address adequately. Surveyors must evolve their approaches to incorporate both current transaction reality and informed forward expectations, while maintaining professional standards and managing risk.

Key Action Steps for Property Professionals

🎯 Adopt dual-weighting frameworks that explicitly balance current transaction evidence with medium-term sentiment indicators

🎯 Implement regional differentiation in valuation approaches, recognizing that London's -40% buyer sentiment requires different treatment than northern regions' relative resilience

🎯 Enhance documentation and transparency in valuation reporting, clearly explaining methodology choices and assumptions

🎯 Integrate rental market analysis into all residential valuations, recognizing that rental strength provides important value support

🎯 Invest in professional development focused on forecasting, sentiment analysis, and adaptive valuation methodologies

The property professionals who successfully navigate this challenging environment will be those who embrace methodological evolution while maintaining rigorous professional standards. By thoughtfully incorporating both current market weakness and forward-looking optimism, surveyors can provide valuations that accurately reflect true market value rather than simply documenting temporary transactional weakness.

For those seeking expert guidance on property valuations during this complex market period, consulting with experienced local chartered surveyors who understand both current conditions and medium-term dynamics is essential for making informed property decisions in 2026.

References

[1] Valuation Impacts Of February 2026 Rics Survey Strategies For Regional Price Divergence In Uk Markets – https://nottinghillsurveyors.com/blog/valuation-impacts-of-february-2026-rics-survey-strategies-for-regional-price-divergence-in-uk-markets

[2] Time For A Better Approach To Valuation In The Uk And Europe – https://www.altusgroup.com/insights/time-for-a-better-approach-to-valuation-in-the-uk-and-europe/

[3] Uk Residential Survey February 2026 – https://www.rics.org/news-insights/uk-residential-survey-february-2026

[4] Uk Residential Market Survey February 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_February-2026.pdf