The RICS price expectations balance plummeted to -18 in February 2026, marking the sharpest monthly decline since September and signaling a dramatic shift in market sentiment [2]. This collapse from -6 in the previous month has sent shockwaves through the property valuation sector, forcing surveyors and homeowners alike to recalibrate their pricing strategies. Understanding Valuation Adjustments Amid February 2026 RICS Market Slowdown: Strategies for Cautious Price Expectations has become essential for anyone navigating today's uncertain property landscape.

The February 2026 data reveals more than just numbers—it exposes fundamental weaknesses in buyer confidence, regional disparities that have widened to unprecedented levels, and external pressures from geopolitical events that have dampened what began as a strengthening trend at the start of 2026 [2]. For property professionals, these shifts demand immediate tactical responses in how valuations are conducted, documented, and communicated.

Key Takeaways

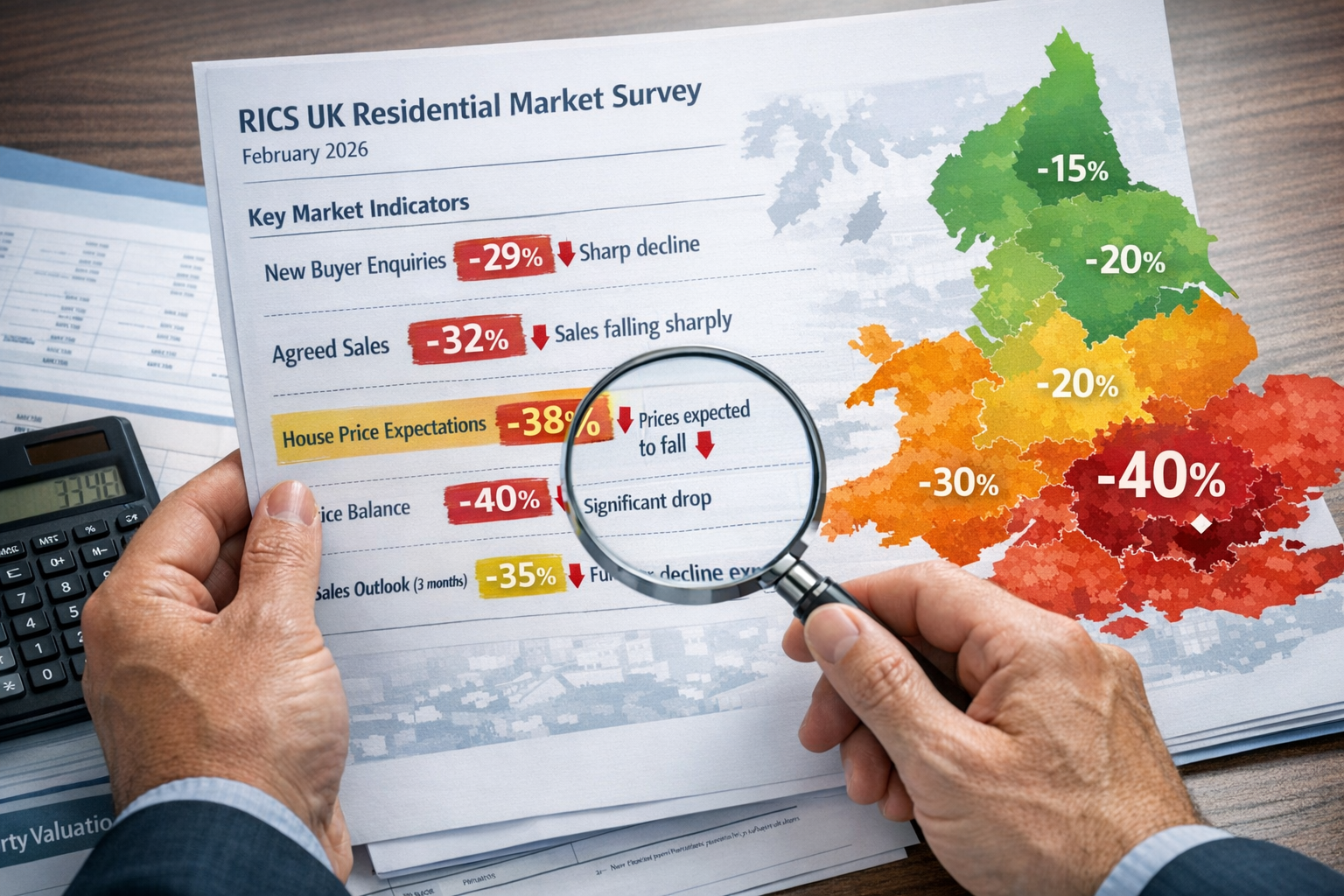

- 📉 RICS price expectations collapsed to -18 in February 2026, down from -6 the prior month, marking the lowest level since September and indicating widespread pessimism

- 🏙️ London experienced severe localized pressure with a -40% net balance in valuation adjustments, requiring specific RICS techniques for mid-market properties

- 🌍 Regional disparities widened significantly across England and Wales, with London's weakness contrasting sharply against relative stability in other markets

- 📊 Near-term sales expectations fell to +4% from +22%, reflecting heightened caution despite 12-month outlook remaining optimistic at +35%

- 🛡️ Strategic valuation adjustments now require enhanced comparable analysis, risk-weighted pricing models, and transparent documentation aligned with RICS Red Book standards

Understanding the February 2026 RICS Market Slowdown

The Sharp Decline in Price Expectations

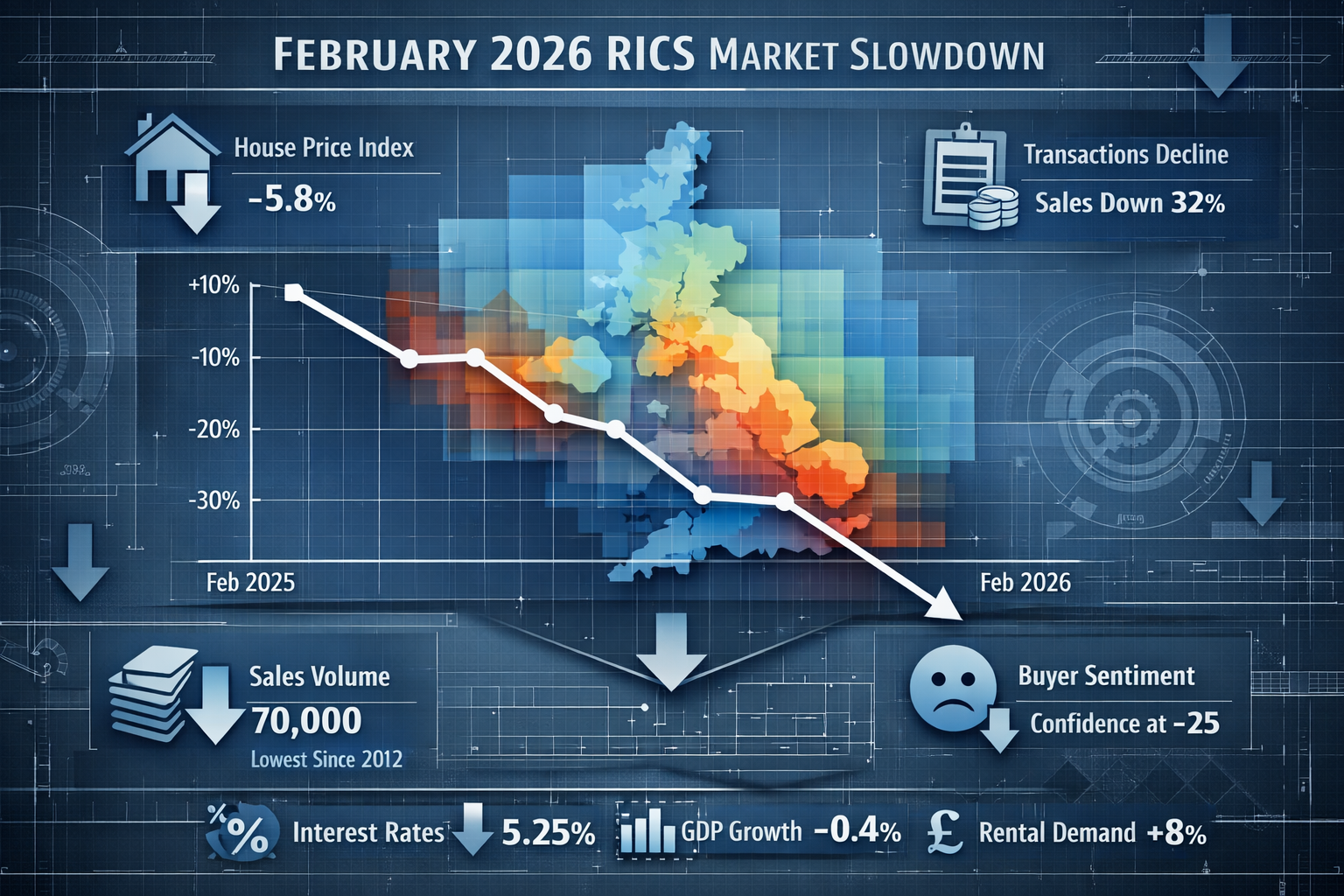

February 2026 marked a turning point for the UK residential property market. The RICS residential market survey revealed that the price expectations balance—a key indicator measuring surveyors' outlook on property values—dropped precipitously to -18, representing the weakest reading since September [2]. This dramatic shift occurred despite initial optimism at the beginning of 2026, when market conditions appeared to be strengthening.

The deterioration was not isolated to a single metric. Near-term sales expectations tumbled from +22% to just +4%, indicating that surveyors anticipated significantly fewer transactions in the immediate future [5]. This represented one of the most substantial monthly declines in sales confidence recorded in recent years, suggesting that the market slowdown was both sudden and severe.

Several factors contributed to this downturn:

- Geopolitical uncertainty stemming from Middle East events dampened buyer sentiment throughout February [2]

- Employment data weakness from the U.S., where payrolls fell by 92,000 jobs against expectations of a 50,000 gain, created ripple effects across global markets [4]

- Rising unemployment in major economies, with U.S. unemployment reaching 4.4% and labor force participation slipping to approximately 62% [4]

- Valuation pressures across asset classes as investors reassessed risk profiles amid economic uncertainty

For property valuers, these macroeconomic headwinds translated into immediate practical challenges. Traditional valuation methodologies that relied on stable market conditions and predictable price trajectories suddenly required significant recalibration.

London's Localized Crisis: The -40% Adjustment

While national figures painted a concerning picture, London's property market faced particularly acute pressure. The capital recorded a staggering -40% net balance in valuation adjustments for February 2026 [3], representing the most severe localized downturn in the UK market.

This dramatic figure meant that 40% more surveyors reported downward price adjustments than upward revisions in London properties. The implications were profound:

| Metric | London | National Average | Difference |

|---|---|---|---|

| Price Expectations Balance | -40% | -18% | -22 percentage points |

| Valuation Adjustment Severity | Severe | Moderate | Significant gap |

| Market Sentiment | Highly pessimistic | Cautious | Regional divergence |

The London-specific crisis necessitated particular attention to methods of valuation that could accurately capture the rapid market deterioration. Mid-market properties—those valued between £1 million and £3 million—faced especially complex valuation challenges as they sat at the intersection of high-value tax thresholds and shifting buyer demographics [3].

Professional surveyors working in London had to implement enhanced due diligence protocols, including:

✅ More frequent comparable sales reviews to capture rapidly changing market conditions

✅ Increased risk weighting for properties in segments experiencing acute pressure

✅ Enhanced documentation justifying valuation adjustments to lenders and clients

✅ Scenario analysis incorporating multiple price trajectory assumptions

Regional Disparities Across England and Wales

The February 2026 data exposed widening regional disparities that challenged the notion of a unified UK property market [5]. While London struggled with severe downward pressure, other regions demonstrated relative resilience or even stability.

Northern England and the Midlands maintained more balanced price expectations, with some areas recording neutral or slightly positive net balances. This divergence reflected fundamental differences in:

- Local economic conditions and employment prospects

- Affordability dynamics and first-time buyer activity

- Investment patterns and buy-to-let market health

- Supply constraints and new construction activity

For surveyors conducting Canterbury property valuations and assessments across different regions, these disparities required location-specific approaches. A valuation methodology appropriate for a London property might significantly overstate or understate value when applied to a comparable property in Manchester or Birmingham.

The regional divergence also affected rental markets differently. While landlord rental instructions showed constraint at -24% nationally in January, this masked significant variation [5]. Some regions experienced landlord exits and rental supply shortages, while others saw stable or growing rental stock.

Valuation Adjustments Amid February 2026 RICS Market Slowdown: Practical Strategies

Enhanced Comparable Sales Analysis

In a rapidly shifting market, comparable sales analysis became the cornerstone of accurate valuation adjustments. The traditional approach of selecting three to five comparable properties sold within the past six months proved insufficient during the February 2026 slowdown.

Professional surveyors adapted by implementing more rigorous comparable selection criteria:

Temporal Weighting: Properties sold within the most recent 30-60 days received significantly higher weighting than those sold 90+ days ago, reflecting the rapid pace of market change. A property sold in December 2025 might have transacted under fundamentally different market conditions than one sold in February 2026.

Adjustment Factors: Each comparable required explicit adjustments for:

- Time of sale (with monthly adjustment factors of 1-3% in rapidly moving markets)

- Location micro-variations (street-by-street analysis in high-value areas)

- Property condition (with particular attention to deferred maintenance affecting value)

- Market motivation (distinguishing distressed sales from arm's-length transactions)

Volume and Diversity: Rather than relying on three comparables, best practice evolved to include 8-12 properties spanning a broader range, with outliers explicitly identified and explained. This approach provided more robust statistical validation of value conclusions.

For those seeking professional guidance, understanding the price of valuation services became important, as enhanced analysis required additional surveyor time and expertise.

Risk-Weighted Pricing Models

The February 2026 market conditions demanded that surveyors move beyond single-point value estimates toward risk-weighted pricing models that acknowledged uncertainty and provided value ranges rather than precise figures.

This approach involved:

Scenario Analysis: Developing three valuation scenarios:

- Optimistic scenario (+10-15% from base): Assuming market stabilization and return to positive sentiment within 6-12 months

- Base scenario (reference point): Reflecting current market conditions and modest continued softening

- Pessimistic scenario (-10-15% from base): Incorporating potential for further deterioration if macroeconomic conditions worsen

Probability Weighting: Assigning probabilities to each scenario based on leading indicators such as mortgage approval rates, employment data, and consumer confidence indices. In February 2026, many surveyors weighted the pessimistic scenario at 35-40%, significantly higher than the typical 20-25% in stable markets.

Value Range Reporting: Rather than stating "Market Value: £500,000," risk-weighted reports presented "Market Value Range: £475,000-£525,000, with base estimate of £500,000 subject to elevated market uncertainty." This transparency helped clients understand the limitations of valuation precision during volatile periods.

The risk-weighted approach proved particularly valuable for valuation factors that were themselves in flux, such as location premiums, property condition impacts, and buyer preference trends.

Documentation and RICS Red Book Compliance

Heightened market uncertainty elevated the importance of comprehensive documentation and strict adherence to RICS Red Book standards. Valuation reports prepared during the February 2026 slowdown required enhanced disclosure and justification.

Key documentation requirements included:

📋 Market Context Section: Every valuation report needed a dedicated section explaining current market conditions, including:

- Reference to RICS survey data and trends

- Discussion of regional market dynamics

- Acknowledgment of geopolitical and economic factors affecting sentiment

- Explicit statement of market uncertainty and its impact on valuation confidence

📋 Comparable Evidence Detail: Enhanced presentation of comparable sales with:

- Full address and transaction details (where permissible)

- Specific adjustment calculations with justification

- Time-series analysis showing price trends for each comparable

- Explanation of why each comparable was selected and how it informs the subject valuation

📋 Assumptions and Special Assumptions: Clear articulation of all assumptions underlying the valuation, with particular attention to:

- Market conditions assumptions (e.g., "assuming no further deterioration beyond February 2026 levels")

- Transaction timeline assumptions

- Property condition assumptions

- Regulatory and planning assumptions

📋 Limitations and Caveats: Explicit statement of valuation limitations, including:

- Reduced market transaction volume affecting comparable availability

- Increased uncertainty in price expectations

- Potential for rapid market changes affecting value validity period

For specialized valuations such as divorce valuations or probate valuations, these documentation requirements became even more critical, as the valuations often served as evidence in legal proceedings where scrutiny would be intense.

Communicating Cautious Price Expectations to Clients

Perhaps the most challenging aspect of Valuation Adjustments Amid February 2026 RICS Market Slowdown: Strategies for Cautious Price Expectations was effectively communicating market realities to clients who often had emotional attachments to properties or financial expectations based on pre-slowdown valuations.

Effective communication strategies included:

Setting Realistic Expectations Early: During initial client consultations, surveyors established that valuations would reflect current market conditions, which might differ significantly from client expectations formed during more buoyant periods.

Visual Data Presentation: Using charts and graphs to illustrate:

- RICS survey trend lines showing the February decline

- Regional price movement comparisons

- Transaction volume trends indicating market liquidity

- Days-on-market statistics demonstrating slower sales velocity

Contextual Framing: Explaining that a February 2026 valuation represented a snapshot in time during unusual market conditions, and that values could recover (or decline further) depending on subsequent economic developments.

Action-Oriented Recommendations: Rather than simply delivering disappointing news, professional surveyors provided strategic guidance:

- For sellers: Optimal timing considerations and pricing strategies to maximize achievable value

- For buyers: Negotiation leverage opportunities and due diligence priorities

- For lenders: Risk mitigation measures and loan-to-value ratio adjustments

- For investors: Hold-versus-sell analysis and portfolio rebalancing options

Regional Strategies: Navigating Divergent Markets Across England and Wales

London-Specific Valuation Tactics

The -40% net balance in London's February 2026 valuation adjustments demanded specialized approaches that acknowledged the capital's unique market dynamics [3]. Surveyors working in London implemented several tactical adjustments:

Micro-Location Analysis: London's property market operates at a granular level where value can vary dramatically between adjacent streets or even between properties on the same street. February 2026 valuations required even more detailed micro-location analysis, considering:

- Proximity to transport links (with increased premium for Crossrail-adjacent properties)

- School catchment areas (with particular attention to Outstanding-rated primaries)

- Neighborhood gentrification trajectories

- Local amenity availability and quality

Tax Threshold Sensitivity: Properties valued near key tax thresholds (£1 million, £1.5 million, £2 million) required careful consideration of how small valuation adjustments could trigger disproportionate tax consequences for buyers. This affected marketability and, consequently, value [3].

International Buyer Considerations: London's traditional reliance on international buyers meant that geopolitical events and currency fluctuations had outsized impacts. February 2026 valuations needed to account for reduced international demand resulting from Middle East tensions and global economic uncertainty [2].

Leasehold Complications: Many London properties are leasehold with varying remaining terms. The February slowdown affected lease extension valuations differently than freehold values, requiring specialized expertise in leasehold valuation methodologies.

Regional England and Wales Approaches

Outside London, surveyors adapted their approaches to reflect local market conditions that, while affected by the national slowdown, demonstrated different characteristics:

Northern England: Markets in Manchester, Liverpool, and Leeds showed greater resilience, with some areas recording neutral price expectations. Valuation strategies emphasized:

- Strong rental yields supporting investment value

- Regeneration projects and infrastructure improvements

- Affordability advantages attracting first-time buyers and relocating families

- Growing tech and professional services sectors supporting employment

Midlands: Birmingham and surrounding areas experienced moderate softening but avoided London's severe decline. Surveyors focused on:

- HS2 infrastructure impacts (both positive for connectivity and negative for construction disruption)

- Manufacturing sector health and employment prospects

- Regional affordability dynamics

- Buy-to-let market stability

South East (excluding London): Areas such as Canterbury, Brighton, and Oxford demonstrated mixed performance. Valuation considerations included:

- Commuter premium adjustments reflecting hybrid working trends

- University town dynamics and student accommodation demand

- Coastal property resilience and lifestyle migration patterns

- Historic property valuations requiring specialized expertise

Wales: Welsh markets showed relative stability with localized pockets of growth. Surveyors considered:

- Cardiff's economic diversification and government sector employment

- Rural property demand from lifestyle buyers

- Second home market dynamics and regulatory changes

- Affordable housing initiatives and first-time buyer support schemes

For surveyors working across multiple regions, maintaining current knowledge of local market conditions became essential. Commercial valuations also required regional customization, as business property markets responded differently to the residential slowdown.

Rental Market Implications

The February 2026 slowdown had complex effects on rental markets that influenced both residential valuations and investment property assessments. While landlord rental instructions remained constrained at -24% nationally, rental price expectations showed surprising strength, with +28% of respondents anticipating near-term increases [5].

This dynamic created several valuation considerations:

Yield Compression: As capital values softened while rents remained stable or increased, gross and net yields improved for investment properties. This partially offset capital value declines for buy-to-let portfolios.

Tenure Flexibility: Properties suitable for both owner-occupation and rental achieved premium valuations due to optionality, particularly in uncertain markets where buyers valued flexibility.

Rental Demand Drivers: Factors supporting rental demand included:

- Mortgage affordability challenges keeping potential buyers in rental market longer

- Economic uncertainty making renting more attractive than ownership commitment

- Lifestyle flexibility preferences among younger demographics

- Corporate relocation and temporary accommodation needs

For commercial rent reviews, the residential market slowdown had indirect effects through reduced retail spending and office space demand, requiring integrated analysis of residential and commercial market trends.

Medium-Term Outlook and Strategic Planning

The 12-Month Optimism Paradox

Despite the severe near-term pessimism reflected in February 2026 data, RICS survey participants maintained surprising optimism for the 12-month outlook, with +35% net balance anticipating increased sales activity [5]. This apparent contradiction—short-term gloom paired with medium-term optimism—created strategic planning challenges for property professionals.

Several factors explained this paradox:

Interest Rate Expectations: Market participants anticipated that central bank rate cuts would materialize in the second half of 2026, improving mortgage affordability and stimulating demand. The 10-year Treasury yield had already eased to approximately 4.02% by late February, down from January levels [1].

Pent-Up Demand: The slowdown had suppressed transaction activity, creating a reservoir of potential buyers and sellers who were postponing decisions until market conditions clarified. This pent-up demand could drive a rebound once confidence returned.

Economic Stabilization: While February employment data disappointed, many economists expected labor markets to stabilize and potentially strengthen in the latter half of 2026 as geopolitical tensions eased and monetary policy became more accommodative.

Seasonal Patterns: The February slowdown occurred during traditionally slower winter months. Spring and summer typically bring increased market activity, and participants expected this seasonal pattern to reassert itself.

For surveyors, this outlook paradox suggested several strategic approaches:

✅ Maintain conservative near-term valuations while acknowledging potential for recovery

✅ Provide clients with scenario analysis showing value trajectories under different market conditions

✅ Advise on optimal transaction timing based on individual circumstances and market forecasts

✅ Monitor leading indicators such as mortgage approvals, viewing activity, and consumer confidence for early signs of recovery

Preparing for Market Recovery

While February 2026 demanded cautious valuation adjustments, forward-thinking property professionals simultaneously prepared for eventual market recovery. This preparation involved:

Building Comparable Databases: Systematically documenting transactions during the slowdown period to create robust datasets for future analysis. Properties transacting in February-April 2026 would provide valuable evidence of market bottoms and early recovery signals.

Client Relationship Management: Maintaining regular communication with clients to provide market updates and position for future opportunities. Clients who felt well-informed and supported during difficult periods would be more likely to engage for purchase, sale, or refinancing opportunities when markets recovered.

Professional Development: Using the slower transaction period to enhance skills and knowledge through:

- RICS continuing professional development courses

- Specialized valuation methodology training

- Technology and software proficiency improvements

- Market research and analysis capabilities

Service Diversification: Expanding service offerings to include valuations less affected by market cycles, such as:

- Probate valuations (driven by demographic factors rather than market timing)

- Reinstatement cost valuations for insurance purposes

- Commercial building surveys for business properties

- Specialized assessments such as shared ownership property valuations

Technology and Data-Driven Valuation

The February 2026 market slowdown accelerated adoption of technology-enabled valuation approaches that enhanced accuracy and efficiency. Progressive surveying firms invested in:

Automated Valuation Models (AVMs): While not replacing professional judgment, AVMs provided rapid initial value estimates and helped identify potential comparable properties. During volatile markets, AVMs required frequent recalibration to reflect changing conditions.

Property Data Platforms: Subscription services providing comprehensive transaction data, planning information, and market analytics enabled more thorough comparable analysis and market research.

Desktop Valuations: For certain purposes and property types, technology-enabled desktop valuations offered cost-effective alternatives to full physical inspections, though with appropriate caveats and limitations.

Geographic Information Systems (GIS): Mapping and spatial analysis tools helped visualize regional market trends, identify micro-location value drivers, and present complex data to clients in accessible formats.

Communication Platforms: Video conferencing and digital document sharing enabled efficient client communication and reduced transaction friction, particularly valuable when market uncertainty made in-person meetings more challenging to schedule.

Conclusion

The Valuation Adjustments Amid February 2026 RICS Market Slowdown: Strategies for Cautious Price Expectations represent a critical inflection point for UK property professionals. The dramatic collapse in price expectations to -18 nationally and -40 in London has fundamentally altered the valuation landscape, demanding enhanced methodologies, rigorous documentation, and transparent client communication [2][3].

Surveyors navigating this challenging environment must balance multiple imperatives: maintaining professional standards and RICS Red Book compliance, providing accurate valuations that reflect current market realities, communicating difficult messages to clients with empathy and clarity, and positioning for eventual market recovery while managing near-term risks.

The regional divergence across England and Wales adds complexity, requiring location-specific approaches that acknowledge the vast differences between London's severe downturn and the relative stability of many regional markets [5]. What works for a mid-market London property facing tax threshold sensitivities may be entirely inappropriate for a northern England property benefiting from strong rental yields and affordability advantages.

Actionable Next Steps

For property professionals and stakeholders navigating the February 2026 market slowdown, consider these concrete actions:

🎯 Review and update valuation methodologies to incorporate enhanced comparable analysis, risk-weighted pricing, and comprehensive documentation

🎯 Invest in professional development focusing on specialized valuation techniques and market analysis capabilities

🎯 Enhance client communication protocols to set realistic expectations and provide strategic guidance beyond simple value figures

🎯 Monitor leading indicators including mortgage approvals, employment data, and consumer confidence for early recovery signals

🎯 Diversify service offerings to include valuation types less affected by market cycles

🎯 Build regional market expertise to capitalize on opportunities in areas showing resilience

🎯 Leverage technology to improve efficiency and analysis quality while maintaining professional judgment

For property owners, buyers, and investors, the February 2026 slowdown creates both challenges and opportunities. Those requiring valuations should engage qualified RICS professionals who understand current market dynamics and can provide comprehensive valuation reports that go beyond simple numbers to offer strategic insights.

The path forward requires patience, professionalism, and adaptability. While near-term conditions remain challenging, the medium-term outlook suggests potential for recovery as interest rates moderate and economic conditions stabilize. By implementing the strategies outlined in this analysis, property professionals can navigate the current slowdown while positioning for success when market confidence returns.

References

[1] Three Forces Point To A Second Half 2026 Market Recovery Earnings Consolidation Upward Revisions And Falling Rate Expectations – https://www.svcp.com/three-forces-point-to-a-second-half-2026-market-recovery-earnings-consolidation-upward-revisions-and-falling-rate-expectations/

[2] Uk Rics Residential Market Survey Feb 2026 – https://www.capitaleconomics.com/publications/uk-housing-market-update/uk-rics-residential-market-survey-feb-2026

[3] Building Survey Protocols For Mid Market Properties Under New High Value Tax Thresholds Rics Strategies Post 2026 Budget – https://nottinghillsurveyors.com/blog/building-survey-protocols-for-mid-market-properties-under-new-high-value-tax-thresholds-rics-strategies-post-2026-budget

[4] Reviewing The February 2026 Markets – https://manercpa.com/reviewing-the-february-2026-markets/

[5] Uk Residential Market Survey January 2026 – https://www.rics.org/content/dam/ricsglobal/documents/market-surveys/uk-residential-market-survey/UK-Residential-Market-Survey_January-2026.pdf

[6] Market Surveys – https://www.rics.org/news-insights/market-surveys